Victoria Bazir

Victoria Bazir

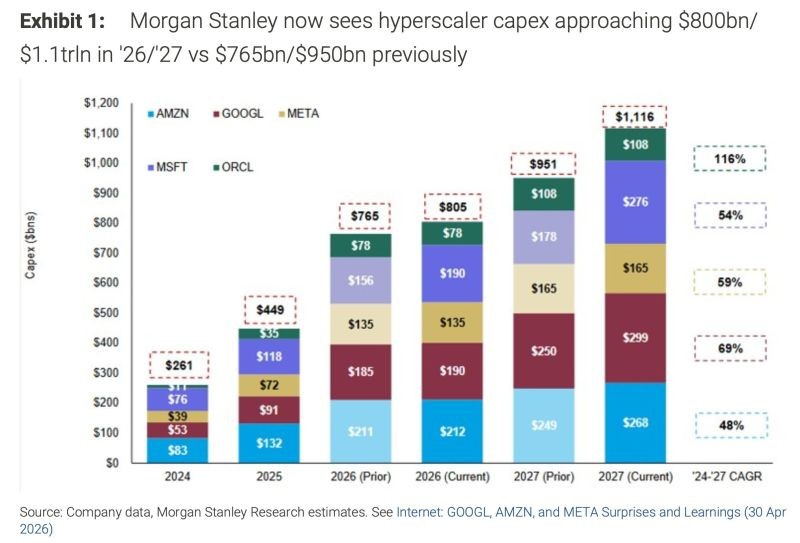

Morgan Stanley's latest update projects that Amazon, Microsoft, Google, Meta, and Oracle will spend a combined $805 billion on capital expenditures in 2026 and $1.116 trillion in 2027. Just months ago, those estimates stood at $765 billion and $951 billion.

The scale of spending is remarkable. The revisions are even more interesting. If AI infrastructure demand were starting to cool, forecasts would be moving lower. Instead, analysts continue raising them. Morgan Stanley added another $40 billion to its 2026 estimate and another $165 billion to its 2027 forecast. That is not what a maturing investment cycle usually looks like.

Morgan Stanley has raised its hyperscaler capex forecast again, now projecting spending to exceed $1.1 trillion by 2027 across Amazon, Microsoft, Google, Meta, and Oracle.

The Market Keeps Underestimating the Buildout

The AI narrative is often framed around model releases, benchmark scores, and product launches. Capital spending tells a different story. Combined hyperscaler capex reached roughly $261 billion in 2024. Morgan Stanley now expects that figure to more than quadruple by 2027.

The increase is not driven by a single company. Amazon's projected capex rises from roughly $83 billion in 2024 to $268 billion in 2027. Microsoft climbs from $76 billion to $276 billion. Google moves from $53 billion to $299 billion. Meta expands from $39 billion to $165 billion.

Even Oracle, the smallest player in the group, is expected to spend more than $100 billion by 2027. These numbers suggest that AI infrastructure is no longer being funded as a short-term opportunity. The spending plans assume demand remains elevated for years.

The key takeaway is not that hyperscalers are spending aggressively. Markets have known that for some time. The key takeaway is that analysts continue revising expectations upward after every earnings cycle.

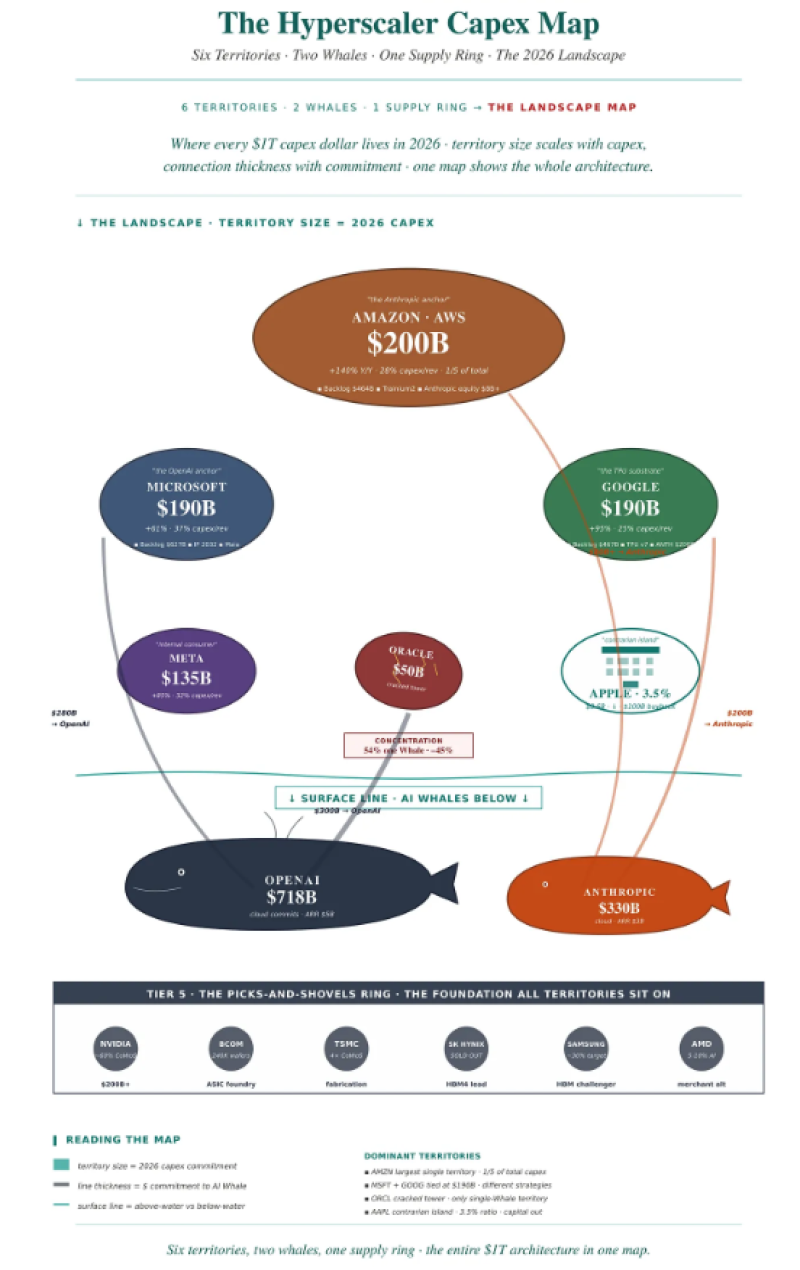

The AI ecosystem is increasingly organized around infrastructure ownership. Hyperscalers control the largest capital pools, while model developers such as OpenAI and Anthropic depend on access to compute and cloud capacity.

The Center of the AI Economy Is Not Where Most Investors Look

OpenAI and Anthropic dominate discussions about artificial intelligence. The capex map tells a different story. OpenAI is shown with approximately $17 billion in annualized revenue. Anthropic sits near $3 billion. Both companies are important, but neither controls the infrastructure that powers the ecosystem.

Above them sit Amazon, Microsoft, Google, Meta, Oracle, and Apple. AWS alone is associated with roughly $200 billion of capex in 2026. Microsoft and Google are each approaching $190 billion. Those figures are large enough to reshape entire supply chains.

The industry's balance of power remains concentrated among companies that own data centers, cloud platforms, networking infrastructure, and long-term power agreements. Model developers generate demand. Hyperscalers finance the capacity needed to satisfy it.

Follow the Money, Not the Models

The most useful way to read the capex forecasts is to follow where the dollars ultimately end up. Every new AI cluster requires GPUs, advanced memory, networking equipment, cooling systems, power infrastructure, and semiconductor manufacturing capacity.

That is why the same names appear repeatedly across the AI supply chain. Nvidia sits at the center of accelerated computing. Broadcom supplies networking and custom silicon. TSMC manufactures the most advanced chips used throughout the ecosystem.

SK Hynix and Samsung provide the high-bandwidth memory required by modern AI systems. AMD is steadily expanding its position as hyperscalers look for alternatives in AI accelerators. Nearly every dollar of hyperscaler spending flows through some combination of those companies.

That makes AI different from previous software booms. The largest beneficiaries are not necessarily the companies building applications. They are often the companies supplying the infrastructure those applications require.

A Trillion-Dollar Capex Cycle Changes the Equation

Once annual spending approaches $1 trillion, the impact extends far beyond Silicon Valley. Utilities are seeing data-center demand become a major growth driver. Power equipment suppliers are expanding production capacity. Construction firms are securing long-duration projects tied to new AI campuses.

Semiconductor manufacturers are investing to support future demand years before it arrives. The result is an AI economy that reaches well beyond model providers and cloud platforms.

That may explain why spending forecasts continue moving higher. The buildout is no longer limited to a handful of technology companies. It is creating demand across multiple industries simultaneously.

Wall Street still tends to discuss AI through the lens of applications and models. The spending data points somewhere else. A system requiring more than $1 trillion of annual investment starts to look less like a software market and more like infrastructure. At that scale, the defining question is no longer which model performs best. The defining question is who controls the assets required to keep the system expanding.

Victoria Bazir

Victoria Bazir