Eseandre Mordi

Eseandre Mordi

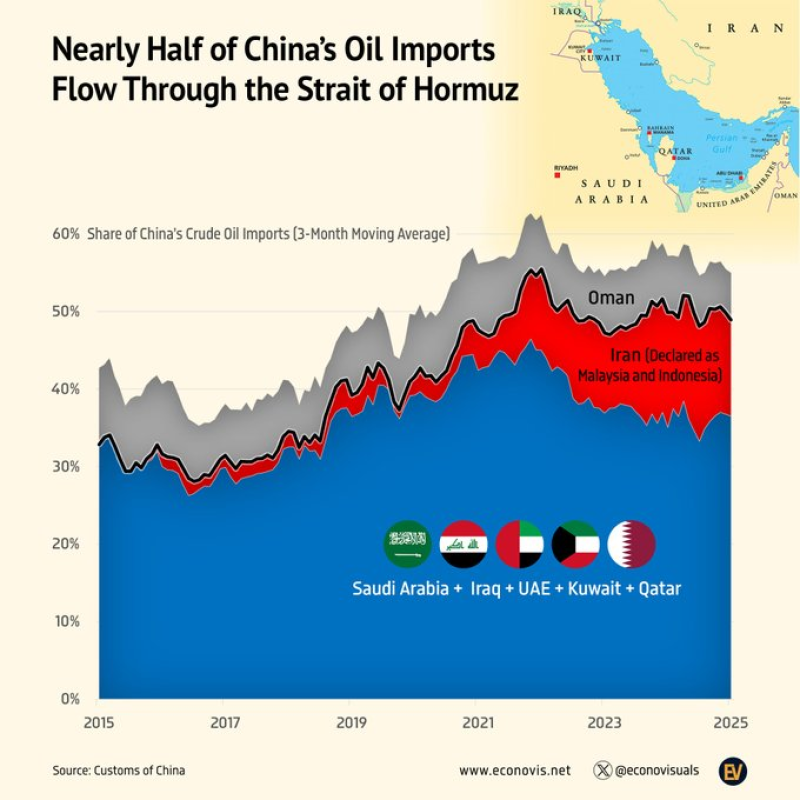

A critical vulnerability is back in focus. As Jack Prandelli noted, nearly half of China's crude oil imports flow through the Strait of Hormuz. The chart confirms this concentration, showing the share of imports routed through the region rising from roughly 30% in 2015 to near the 45-50% range in recent years.

A China Hormuz Dependency That Built Over a Decade

The chart shows a clear upward structure over time. From 2015 onward, China's reliance on Hormuz-linked flows steadily increases, forming higher highs into 2021-2022 before stabilizing near elevated levels.

Even during periods of decline, the structure does not break. The most recent data still sits close to the upper range - indicating that dependency remains structurally high rather than cyclical. The composition aligns with the source: core supply from Saudi Arabia, Iraq, UAE, Kuwait, and Qatar, additional volumes from Oman, and a visible share tied to Iranian flows. The dependency is tied to geography, not a single supplier.

Where Concentration Becomes Global Oil Market Risk

The chart does not show diversification reducing exposure - it shows persistence. Nearly half of China's crude imports continue to rely on a single maritime corridor, creating a highly asymmetric setup.

When dependency is concentrated at a single chokepoint, even partial disruption can impact a large portion of supply. Rather than gradual adjustment, the structure suggests that any sustained constraint would force rapid reallocation of flows across global markets.

Brent Oil Tops $100 as Hormuz Closure Puts 20% of Global Supply at Risk shows how quickly prices respond when Hormuz disruption risk rises - and China's 50% dependence means its demand signal amplifies that response well beyond what the global 20% figure alone would suggest.

Pressure Shifting Across Global Oil Supply Chains

The tweet outlines China's response: increasing non-Gulf sourcing, relying on reserves, and expanding overland flows. Yet the chart suggests these efforts have not materially reduced Hormuz exposure - leaving global oil markets sensitive to shifts in Chinese demand at precisely the moment when the strait is under pressure.

If China is forced to replace even part of these flows, competition for alternative barrels intensifies and supply tightens elsewhere. WTI Crude Oil Spikes to $110-$120 as Strait of Hormuz Closes, Brent Curve Signals Drop to $70 captured exactly that price dynamic playing out in real time - showing the scale of market reaction that China's import concentration helps explain.

Saudi Exports Surge to 4.19M bpd as Yanbu Rerouting Bypasses Hormuz shows how producers are attempting to adapt by rerouting flows through alternative corridors - but the scale of China's Hormuz dependence means that producer-side rerouting alone cannot fully offset the exposure on the demand side.

Eseandre Mordi

Eseandre Mordi