Marina Lyubimova

Marina Lyubimova

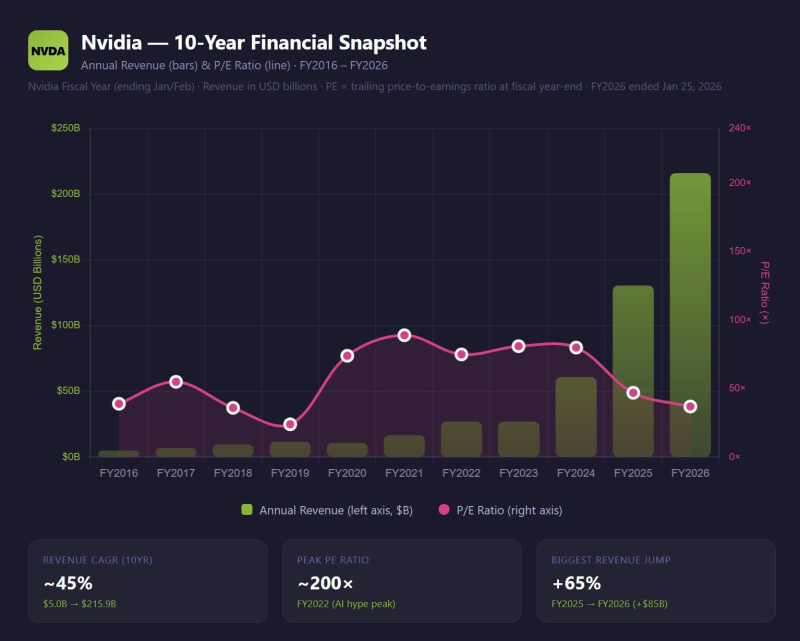

⬤ Nvidia is back in the spotlight. The company's decade-long financial acceleration - revenue up roughly 43x over 10 years at a ~45% CAGR, while the stock itself climbed around 236x over the same period. The bigger talking point, though, is valuation: the argument goes that NVDA now trades at a cheaper P/E than earlier in the cycle, raising the question of whether the market is still underpricing the stock's earnings power even as sentiment remains cautious. Also relevant: Nvidia Hits $215B in Revenue as NVDA Shares Test $197 Resistance.

⬤ The "Nvidia 10-Year Financial Snapshot" chart tells the story clearly. Revenue grew from roughly $5.0B in FY2016 to $215.9B in FY2026 - a ~45% CAGR across the decade. The sharpest single-year jump came most recently: +65% from FY2025 to FY2026, adding about $85B to the top line in one fiscal year alone. That kind of growth at this scale is genuinely rare. For more context on recent price action, see NVDA Price Climbs While P/E Drops to 48x.

NVDA should be around $320 if it were trading at the same P/E a year from now - this is a function of earnings growth, not multiple expansion.

⬤ On valuation, the P/E line in the chart peaked near ~200x around FY2022 - the labeled "AI hype peak" - before trending lower into FY2025 and FY2026. That compression supports the core thesis: Nvidia's multiple has cooled even as revenue scaled dramatically. The price target of $320 floated in the original commentary leans entirely on continued earnings growth rather than any re-rating of the multiple. Details on where the multiple stands today are covered in NVDA Valuation Drops to 40x as Shares Pull Back to 6-Month Low.

⬤ What makes this snapshot meaningful is the combination: massive revenue growth at enormous scale, paired with a valuation multiple sitting well below its own cycle highs. As the AI infrastructure buildout continues, the next chapter for NVDA will come down to one thing - whether earnings keep outrunning expectations, or whether a more normalized P/E finally starts to weigh on price.

Marina Lyubimova

Marina Lyubimova