Artem Voloskovets

Artem Voloskovets

The most important shift in global equities is no longer happening inside earnings reports or central bank meetings. It is happening inside market concentration itself.

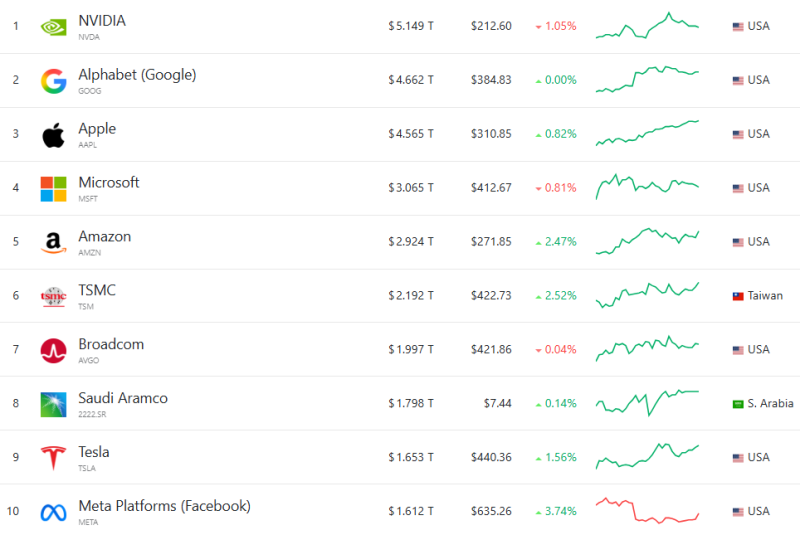

The latest global market-cap rankings increasingly resemble a map of AI infrastructure dominance rather than a diversified representation of the world economy. Nvidia now sits above $5 trillion in market value. Alphabet, Microsoft, Amazon, TSMC and Broadcom are clustered close behind.

The market is no longer assigning the highest premiums to consumer internet platforms or software distribution alone. It is rewarding ownership of computational infrastructure.

A growing share of global equity value is now concentrated inside companies tied directly to AI infrastructure through semiconductors, hyperscale cloud, networking, memory, or data-center demand.

Semiconductor manufacturers and networking suppliers were still treated as cyclical infrastructure sitting beneath the “real” technology sector. The rise of TSMC, Broadcom and SK Hynix inside global market-cap rankings suggests investors are increasingly pricing computational scarcity itself rather than simply software growth.

Wall Street Is Pricing AI Like Industrial Infrastructure

The deeper shift is less obvious, but potentially more important. AI is decentralizing software creation while simultaneously centralizing capital markets around a narrow infrastructure stack.

What appears on the surface to be diversification across:

- cloud computing,

- semiconductors,

- software,

- memory,

- and networking,

increasingly behaves like one synchronized macro trade expressed through different balance sheets. Microsoft depends on AI demand justifying hyperscale infrastructure spending. Nvidia depends on hyperscalers continuing to absorb accelerated compute at historic scale. TSMC depends on sustained AI chip demand. SK Hynix depends on memory intensity continuing to rise alongside AI workloads.

What looks like multiple independent growth stories may ultimately be a single capex flywheel moving through different layers of the same AI stack.

The AI Era Rewards Bottlenecks, Not Platforms

Previous technology cycles rewarded distribution advantages. The internet era rewarded network access. The mobile era rewarded platforms and ecosystems.

The AI cycle increasingly rewards bottlenecks:

- compute,

- memory,

- networking bandwidth,

- energy density,

- and hyperscale datacenter construction.

Software remains critical, but markets are assigning the largest premiums to firms controlling the physical infrastructure underneath AI itself. The closest historical comparison may not be software at all.

Cisco became indispensable during the internet buildout because online expansion required routers and networking equipment before digital businesses could scale globally. Nvidia now occupies a similar position inside AI compute infrastructure - except the dependency chain has become far more capital-intensive and globally interconnected.

Passive Capital Is Amplifying the Concentration

Higher index weights mechanically force more ETF and benchmark capital into the same cluster of AI-linked equities. Passive ownership amplifies concentration automatically. Underperforming Nvidia or major AI infrastructure names is increasingly becoming institutional career risk for active managers regardless of valuation concerns.

Once a trade becomes large enough inside passive and benchmark structures, flows themselves begin reinforcing leadership independently of fundamentals in the short term.

AI-linked infrastructure companies increasingly dominate global equity leadership across semiconductors, hyperscale cloud, memory, and networking.

The concentration is becoming geopolitical as well. The global AI investment chain now ties together:

- U.S. hyperscalers,

- Taiwanese semiconductor manufacturing,

- Korean memory production,

- Gulf energy capital,

- and Western datacenter expansion.

Technology, industrial policy, energy infrastructure and capital markets are becoming increasingly difficult to separate.

AI Did Not Diversify Markets - It Synchronized Them

Markets have experienced concentration cycles before:

- oil supermajors in the 1970s,

- Japan in the late 1980s,

- internet platforms in the 2010s.

But this cycle is structurally different because nearly every dominant company now depends on the same capex engine continuing to expand. If hyperscaler spending slows, financing costs rise further, or AI monetization disappoints, the pressure would not remain isolated inside one sector.

It would spread simultaneously across:

- semiconductors,

- cloud infrastructure,

- networking,

- industrial equipment,

- memory suppliers,

- and passive index flows.

The AI boom is no longer just a technology story. It is increasingly becoming the organizing structure of global equity markets themselves.

Artem Voloskovets

Artem Voloskovets