Eseandre Mordi

Eseandre Mordi

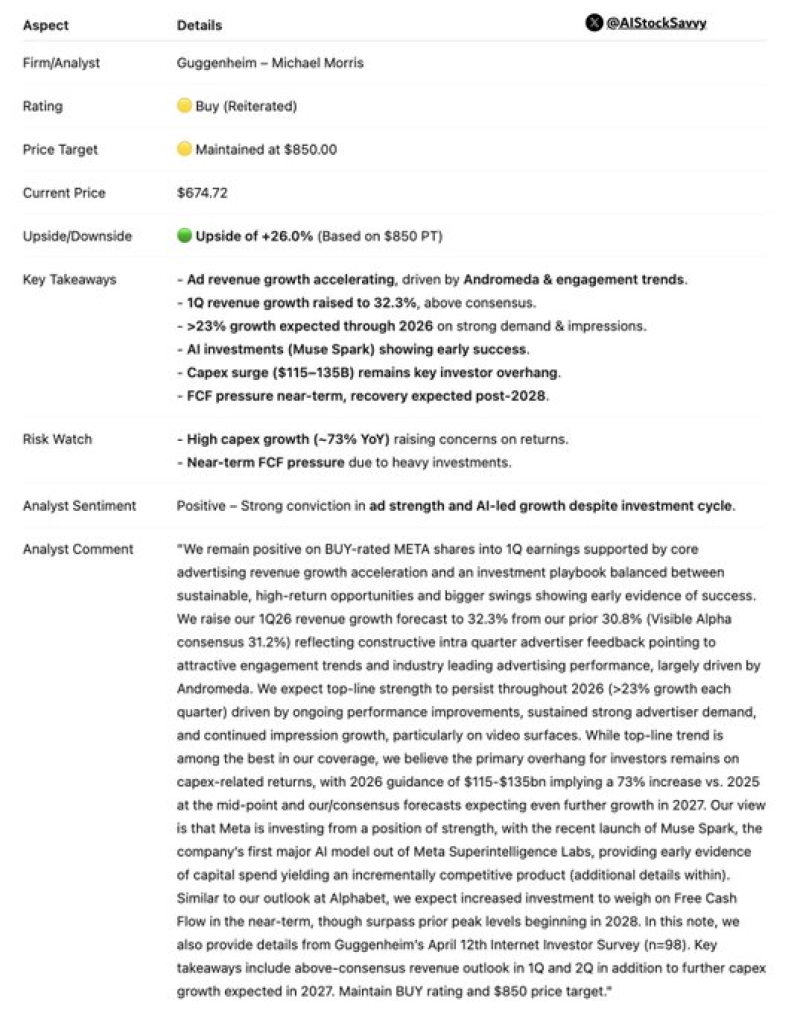

Guggenheim states again that investors should buy Meta Platforms shares and keeps the price goal at $850. By looking at how advertising results improve and how artificial intelligence advances, the firm justifies this position.

At the price of $674, the goal is 26 % higher than the current value. It shows that the firm believes the company will grow.

Growth Outlook

In the first quarter of 2026, Guggenheim predicts that revenue will grow by 32.3% instead of the previous 30.8%. With advertisers providing positive reports and users interacting more with the platform, this estimate is higher than the average market prediction of 31.2%.

For every quarter in 2026, the firm expects that revenue will increase by more than 23 %. By improving how ads perform, meeting higher demand from advertisers and showing more videos to users, the company supports this growth.

As an essential part of the investment, artificial intelligence remains the focus. To improve performance, Meta uses an advertising system called Andromeda. By launching Muse Spark, which is a new model from Meta Superintelligence Labs, the company develops more technology.

And those steps show that the money spent on new technology is becoming actual products that affect the business.

Capex and Cash Flow Dynamics

For the year 2026, the guidance for spending on equipment and infrastructure is between $115 billion and $135 billion. At the middle of this range, the amount is 73 % more than the previous year.

Because of this spending, the cash that remains after expenses will be lower for a short time - but Guggenheim expects this cash to increase later. If the investments in artificial intelligence grow, the cash flow might be higher than previous levels starting in 2028.

What It Means for META Stock

On the stock market, the current price suggests that investors already expect some growth. With a price-to-earnings ratio near 30, the stock is at a price that matches its calculated value. To go higher the company must perform well instead of just meeting expectations.

If the improvements from artificial intelligence make advertising better, the stock might reach the $850 goal - but the increase is not certain. If the current positive view is correct depends on when and how much money the artificial intelligence investments return.

When looking at the risks, multiple factors exist:

- High spending might lower profit margins.

- Artificial intelligence might take a long time to make money.

- Rules from governments about data and ads continue to exist.

- Other companies are also building artificial intelligence platforms.

Market Sentiment

By observing different analysts, it is clear that opinions vary. While some targets are as high as $900, other firms are careful. To explain this they point to risks in how the company operates and the uncertainty of spending on artificial intelligence.

This difference shows that the market is not sure how fast the strategy for artificial intelligence will create financial results.

As a strategy Meta is changing from a company that sells ads into a platform that runs on artificial intelligence. If this change is successful, it will determine the value of the company and its place against competitors for a long time.

To conclude the report from Guggenheim shows that the main advertising business is getting stronger. And the spending on artificial intelligence is starting to show results. At the same time the high costs create risks for the business right now.

The price of the stock depends on if Meta can turn its spending into steady revenue and profit.

Eseandre Mordi

Eseandre Mordi