Saad Ullah

Saad Ullah

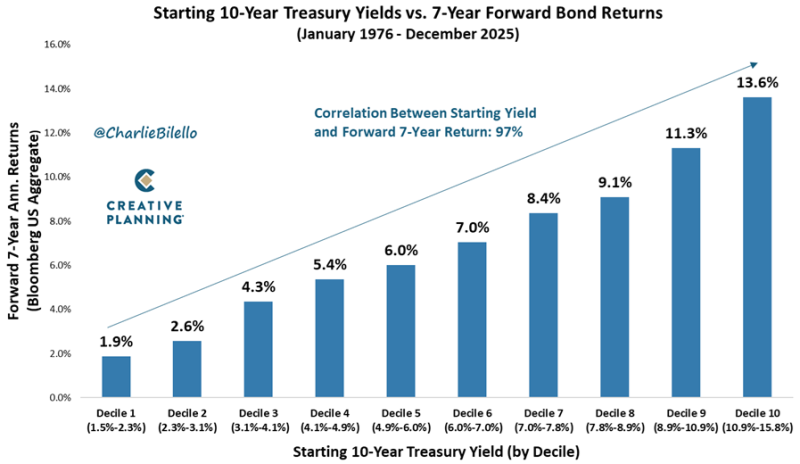

The level of US10Y Treasury yields may offer one of the clearest signals about where bond returns are headed. Historical data shows that the yield available when a bond investment starts is the single most powerful predictor of future performance. Over the past five decades, the relationship between starting yields and forward seven-year bond returns has stayed remarkably tight.

Data from January 1976 through December 2025 shows a 97% correlation between starting US10Y yields and forward seven-year returns. The dataset splits yield environments into ten deciles. When Treasury yields began in the lowest range of roughly 1.5% to 2.3%, the average forward annual return was just 1.9%. When starting yields topped 10.9%, forward annual returns historically reached around 13.6%.

The data shows a clear upward progression in expected performance as US10Y yields rise. Yield environments around 3.1% to 4.1% historically produced forward returns near 4.3%, while starting yields between 7.0% and 7.8% corresponded with roughly 8.4% annual returns over the following seven years. This pattern reflects a core mechanic of fixed-income markets: the yield at purchase largely sets the ceiling on long-term return potential. How Inflation and Interest Rates Affect Intrinsic Valuation explores the broader role of rate changes in asset pricing.

The strong link between US10Y yields and future returns reinforces yield as the central driver of bond performance. Because bond income and reinvestment rates are directly tied to starting yields, shifts in the rate environment can reshape long-term expectations across global fixed-income markets. Broader moves in sovereign debt were covered in Global Long-Dated Bond Yields Climb to 2009 Highs at 4%, while the currency impact of rising yields is tracked in USD/JPY Surges Past 150.00 on Yield Surge and Easing Tariff Concerns.

Saad Ullah

Saad Ullah