Marina Lyubimova

Marina Lyubimova

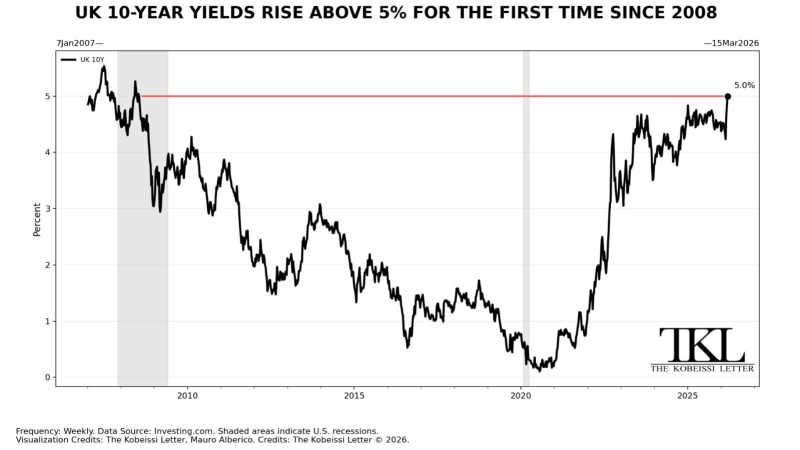

⬤ The UK 10-year government bond yield (UK10Y) has officially crossed the 5.00% mark, its highest level since 2008 and a clear signal of a major shift in the macroeconomic backdrop. The chart shows yields reaching approximately 5.0% in March 2026, capping a multi-year climb from near-zero levels in 2020. Growing inflation concerns across Europe, worsened by a deepening energy crisis, are driving the move.

⬤ The long-term trajectory shows just how dramatic this turnaround has been. After the 2008 financial crisis, UK10Y yields spent years in steady decline, eventually collapsing below 1% during the pandemic. Since 2021, the reversal has been sharp and relentless, with yields breaking higher through 2022 and pressing further into 2026. Crossing 5% means returning to levels not seen in nearly two decades, confirming a structural reset in bond markets.

The break above 5% confirms we are in a new regime, one defined by persistent inflation and tighter financial conditions across developed economies.

⬤ The UK10Y surge fits within a wider global pattern. Energy-related pressures and rising inflation expectations have pushed sovereign yields higher across the board. This mirrors what happened in Japan, where the Japan bond yield surge pushed long-term rates to record highs on similar inflation concerns. Meanwhile, shifting expectations tied to energy shocks continue to reshape yield dynamics, as explored in inflation expectations and yield signals for retail traders navigating this environment.

⬤ A 5% UK10Y yield signals not just a number, but a new era of elevated borrowing costs, persistent price pressures, and tighter conditions that could weigh on households, businesses, and government finances alike. The broader context of shifting European yield dynamics is explored further in the analysis of the European yield inversion shift. With this threshold now crossed, the scale of the ongoing adjustment in global bond markets is hard to ignore.

Marina Lyubimova

Marina Lyubimova