Saad Ullah

Saad Ullah

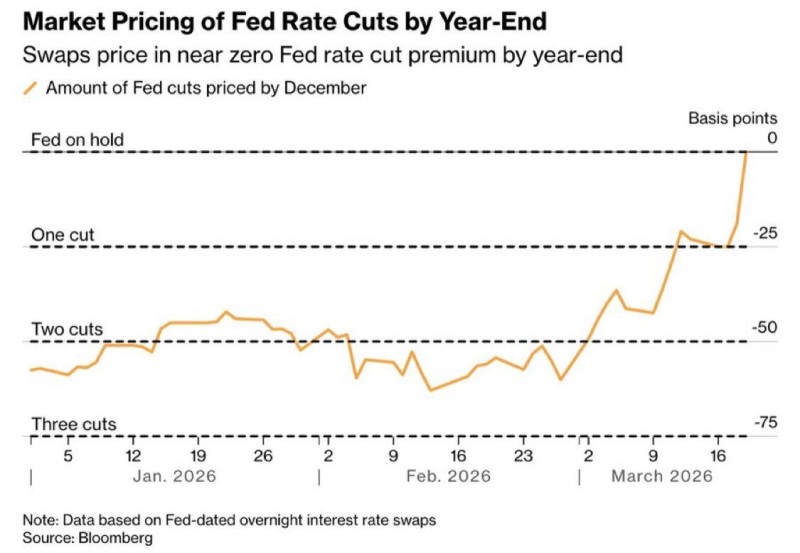

⬤ Swaps markets have moved to price in a 0% probability of Federal Reserve rate cuts through 2026. This marks a dramatic reversal from earlier in the year, when traders were betting on two to three cuts, with swap spreads sitting near -50 to -75 basis points in January and February. As Cointelegraph noted, the repricing followed the Fed's latest decision to hold rates steady amid persistent inflation and cooling easing expectations.

⬤ The chart tracking rate expectations tells a clear story: a steady upward move from deeply negative territory toward zero basis points, effectively wiping out any anticipated easing by year-end. The inflection began in late February and accelerated through mid-March, landing firmly in "Fed on hold" territory.

Markets have essentially given up on rate cuts this year - the data just isn't giving the Fed any room to move.

⬤ The broader macro backdrop is reinforcing the shift. The Fed has now held rates at 3.5%–3.75% for a second straight meeting, with its inflation forecast revised up to 2.7%. That steady-policy stance has aligned closely with what swaps markets are now implying: no cuts, no timeline, no relief for rate-sensitive assets.

⬤ Energy prices are adding another layer of complexity. A $10-per-barrel rise in oil could cut GDP by 0.1% and push inflation to 2.7%, according to recent analysis. That dynamic directly feeds into the Fed's calculus - elevated oil prices stoke inflation, making premature rate cuts riskier and extending the case for a prolonged hold. Together, these forces have reshaped the rate outlook in a matter of weeks.

Saad Ullah

Saad Ullah