Usman Salis

Usman Salis

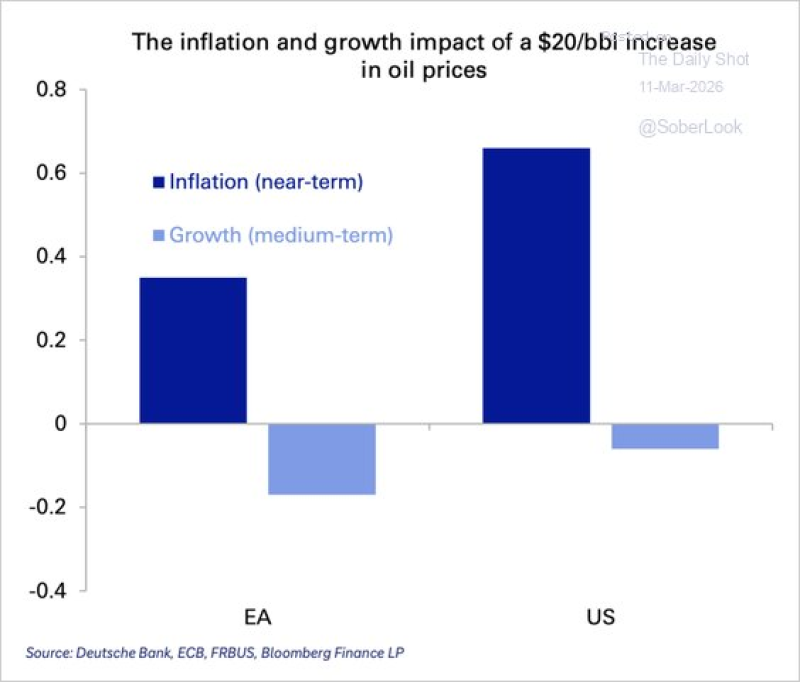

Oil markets rarely move in a straight line, but when they do spike, the ripple effects across developed economies are anything but uniform. New analysis comparing the United States and the euro area shows that a $20 per barrel increase in WTI crude prices would hit each region where it hurts most - and not in the same place.

U.S. Faces 0.65% Inflation Jump, Europe Absorbs Deeper Growth Hit

According to the chart data, a $20 oil price increase would push near-term inflation in the U.S. up by roughly 0.65 percentage points - nearly double the estimated 0.35 percentage point rise in the euro area. The inflation pass-through in America appears significantly stronger, likely reflecting how deeply energy costs are embedded in consumer prices, transportation, and industrial inputs across the U.S. economy.

WTI oil shocks do not impact all developed economies equally - the U.S. inflates, Europe stagnates.

The growth picture flips the script. Europe would absorb a medium-term GDP drag of around -0.18 percentage points, compared with just -0.07 percentage points for the United States. In other words, higher oil prices slow economic activity more severely in Europe, even as American consumers bear a heavier inflationary burden. This divergence matters for investors comparing regional equity exposure and earnings sensitivity across global markets.

WTI Oil Remains a Central Variable in Global Macro Forecasting

This asymmetry doesn't exist in isolation. Crude prices have been extremely volatile in recent months, with sharp rallies tied to geopolitical risk and supply disruptions. WTI Crude Oil Surges Above $84 for the First Time Since July 2025, Up 55% Since December, demonstrating just how fast energy markets can reprice. Further up the curve, WTI Oil Hits $114: Geopolitical Risks Trigger Biggest Surge Since 2022 illustrates the scale of moves possible under stress conditions. For context on the downstream effects, Oil-Powered Growth Risk: $10/Barrel Rise Could Cut GDP 0.1% and Push Inflation to 2.7% quantifies the broader macroeconomic stakes.

The key takeaway is straightforward: oil shocks are not one-size-fits-all. A stronger inflation response in the U.S. and a deeper growth slowdown in Europe could shape how markets read future oil rallies and how central banks on each side of the Atlantic respond. With energy prices still sensitive to supply disruptions and geopolitical flashpoints, the link between WTI crude, inflation, and economic growth will stay front and center in macro analysis.

Usman Salis

Usman Salis