Victoria Bazir

Victoria Bazir

The latest data from the U.S. Energy Information Administration (EIA) showed an unexpected increase in distillate inventories. Stocks rose by 0.951 million barrels, while economists expected a decline of 0.5 million barrels. A week earlier, inventories had fallen by 0.2 million barrels.

The difference between expectations and reality may seem small, but inventory reports are often used as a way to gauge how quickly fuel is moving through the economy.

Diesel Demand and Economic Activity

Unlike gasoline, which is largely consumed by households, diesel is used primarily by businesses. Every shipment delivered by truck, every construction project, and every large-scale agricultural operation requires fuel. As a result, diesel demand tends to reflect activity in sectors that produce, transport, and build.

When inventories rise unexpectedly, it can indicate that consumption is not keeping pace with supply.

The latest report does not prove that economic activity is slowing. It does, however, suggest that fuel demand was weaker than analysts anticipated.

The Latest Build in Historical Context

A weekly inventory increase of roughly one million barrels is not unusual on its own.

Historical EIA data show that distillate inventories regularly swing between substantial draws and builds. The significance of the latest report comes from the gap between forecasts and the actual result.

Instead of a projected draw, inventories increased. Relative to expectations, the surprise amounted to nearly 1.5 million barrels. That discrepancy is what attracted attention across energy markets.

Signals From API Data

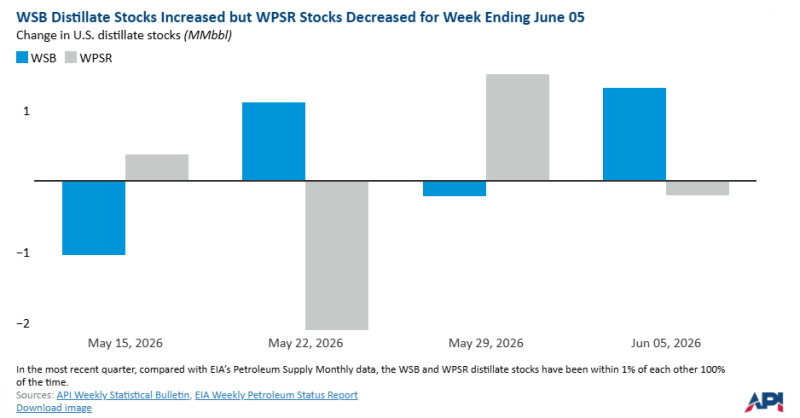

The EIA report was not the first indication that distillate supplies were becoming more abundant. Data published earlier by the American Petroleum Institute (API) showed a build of approximately 1.3 million barrels for the week ending June 5.

Although API and EIA estimates often differ from week to week, both datasets suggest that diesel inventories have recently faced less downward pressure than many analysts expected.

Possible explanations range from slower freight volumes to seasonal fluctuations in refinery operations and fuel consumption.

Crude Oil and Distillates Are Moving in Opposite Directions

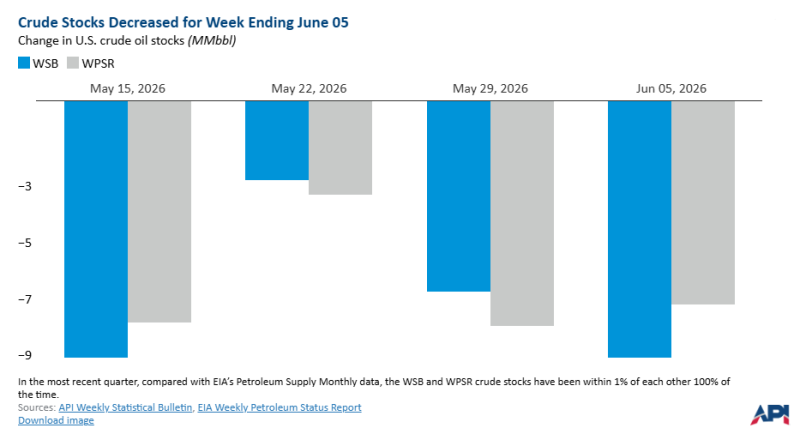

The increase in distillate inventories stands out even more when compared with developments in crude oil stocks.

Recent reports show a consistent pattern of crude inventory declines. During several consecutive weeks, U.S. crude stocks fell by between 3 million and 9 million barrels.

Normally, falling crude inventories are associated with strong refinery demand and active fuel production. The latest data suggest that refineries continue to process large volumes of crude oil, but a portion of the resulting diesel fuel is remaining in storage rather than being consumed immediately.

Gasoline Tells a Different Story

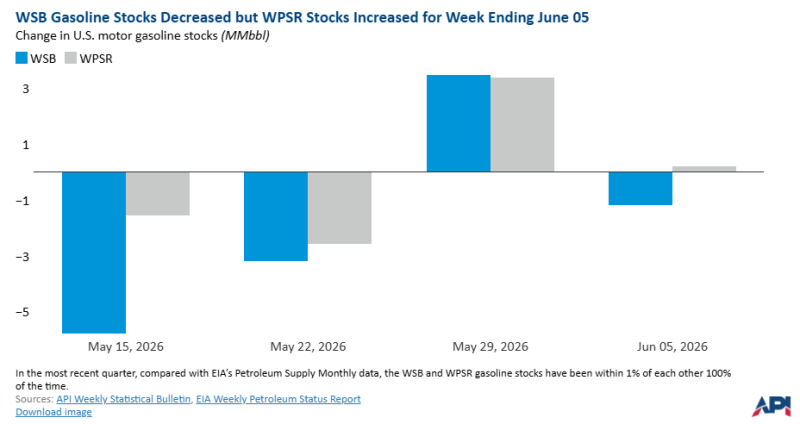

Gasoline inventories do not currently show the same pattern.

Recent reports contain a mix of inventory builds and draws, with no clear indication of sustained oversupply. For the week ending June 5, API reported a gasoline draw of roughly 1.2 million barrels, while EIA data showed a small inventory increase.

This divergence suggests that consumer fuel demand remains relatively stable, while the softness visible in distillate inventories is more closely tied to freight transportation and industrial activity.

What the Inventory Data Suggest

Inventory reports rarely provide definitive answers on their own. Weather conditions, refinery maintenance, imports, exports, and seasonal demand patterns can all influence weekly stock levels.

Even so, diesel remains one of the few fuel categories that offers insight into the movement of goods across the economy. The latest EIA report does not point to a major shift in economic conditions. It does, however, indicate that diesel consumption was weaker than expected during the reporting period.

Whether this turns into a broader trend will become clearer in the coming weeks as additional inventory data are released.

Victoria Bazir

Victoria Bazir