Artem Voloskovets

Artem Voloskovets

JPMorgan strategist Karen Ward argues that lower crude prices could become a major positive factor for the global economy. More supply entering the market would put pressure on oil prices, reduce inflationary risks and strengthen expectations for lower interest rates.

The argument is gaining attention because it is supported not only by geopolitics but also by market expectations.

Oil influences far more than fuel prices. Transportation, logistics, manufacturing, aviation and agriculture all depend on energy costs. When crude becomes cheaper, those costs gradually decline across supply chains.

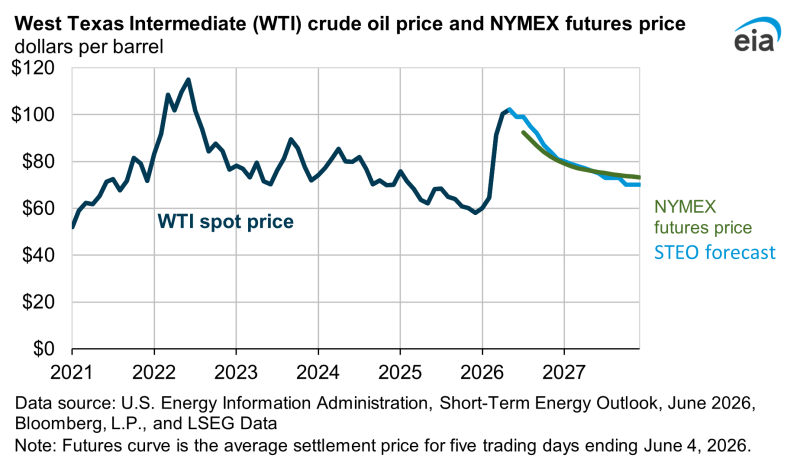

The effect becomes particularly important after several years in which inflation was driven partly by elevated energy prices. Recent forecasts from the U.S. Energy Information Administration suggest that oil may be entering a longer-term downtrend.

WTI traded above $110 per barrel during the 2022 energy shock. Prices later moved into a broad $60–90 range before another rally pushed them above $100 in 2026. The current futures curve points lower, while EIA projections show WTI gradually moving toward the $70–75 range by 2027.

That trajectory is remarkably close to the scenario outlined by Ward. Additional Iranian exports would increase global supply at a time when traders are already pricing weaker oil markets. The significance is not the price target itself. It is the mechanism behind it.

Oil falling because of collapsing demand usually signals economic weakness. Oil falling because of stronger supply tends to have the opposite effect. Lower energy costs improve margins, ease pressure on consumers and reduce inflation without necessarily slowing growth.

Market data already show signs of cooling.

| Date | WTI | Brent |

| June 2 | $97.47 | $98.49 |

| June 3 | $99.76 | $101.69 |

| June 4 | $96.83 | $98.98 |

| June 5 | $94.32 | $97.29 |

| June 8 | $95.00 | $97.46 |

Both benchmarks retreated from early-June highs within days. The move is small, but it illustrates how quickly energy markets react when traders start anticipating additional supply. Lower crude prices would also affect central-bank policy.

Energy remains one of the most visible components of inflation. Sustained declines in oil prices tend to filter into transportation costs, fuel prices and eventually headline inflation readings.

That matters because financial markets are increasingly focused on the timing of future rate cuts rather than the current level of rates. Europe could be one of the largest beneficiaries. European companies remain more exposed to energy costs than many of their U.S. counterparts. At the same time, European equities continue trading at a discount to American stocks despite recent gains.

Reuters recently reported that the STOXX 600 reached record levels as investors reacted positively to the prospect of increased oil supply and lower energy costs. The thesis is straightforward. If oil moves toward the levels implied by current futures markets and EIA forecasts, inflation pressure should ease. Lower inflation would give central banks more flexibility. Cheaper energy would support both consumers and businesses.

A single commodity rarely changes the direction of the global economy on its own. Oil, however, remains one of the few exceptions.

Its influence extends from household budgets and corporate earnings to inflation data and monetary policy decisions. That is why a move toward $70 oil is being discussed not as an energy story, but as a broader economic one.

Artem Voloskovets

Artem Voloskovets