Marina Lyubimova

Marina Lyubimova

The decline comes after one of the strongest advances ever recorded in bullion markets. Over the past year, gold surged from roughly $3,300/oz to more than $5,300/oz as investors piled into safe-haven assets amid geopolitical tensions, aggressive sovereign borrowing, and expectations that major central banks would eventually move toward lower interest rates.

Gold Price Performance (1 Year)

Gold remains dramatically above last year's levels but has struggled to revisit its record highs.

While a 2% drop would normally attract little attention in such a volatile market, the broader trend has become harder to ignore. Gold has now spent months struggling to reclaim its highs, producing a series of lower peaks after the explosive rally that dominated the first quarter. The metal remains historically elevated, but momentum no longer appears as one-sided as it did earlier this year.

Part of the pressure is coming from the currency market. The U.S. Dollar Index (DXY) moved back above the 99 level during Tuesday's session, making dollar-denominated commodities more expensive for overseas buyers and reducing the urgency of defensive positioning.

U.S. Dollar Index (DXY)

The dollar's rebound has increased pressure on precious metals and other dollar-priced commodities.

Normally, renewed dollar strength would be accompanied by expectations of tighter monetary policy. This time, however, that explanation is largely absent.

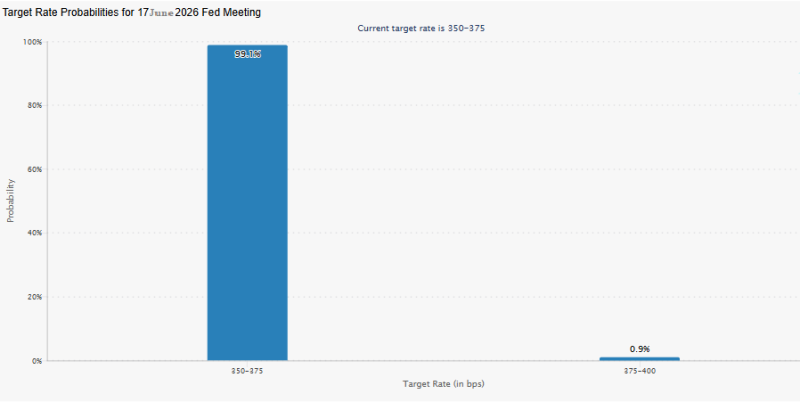

According to CME FedWatch data, traders continue to overwhelmingly expect the Federal Reserve to keep rates unchanged at its June meeting. The market assigns only a negligible probability to another rate increase, suggesting that gold's weakness cannot be easily explained by a sudden shift in interest-rate expectations.

CME FedWatch Rate Probabilities

Markets continue to price in an unchanged Federal Reserve policy path despite gold's decline.

That disconnect is what makes the latest correction notable. The traditional pillars supporting the bullish gold narrative remain largely intact. Central banks continue diversifying reserves, geopolitical risks remain elevated across several regions, and investors still view bullion as a hedge against long-term fiscal deterioration and currency debasement.

Yet prices are no longer responding to those themes with the same intensity as they did during the rally's peak.

One explanation is simple exhaustion. Momentum-driven trades often require a constant flow of new buyers to sustain increasingly ambitious valuations. Once that flow slows, even slightly, markets can spend extended periods consolidating or correcting despite an unchanged macro backdrop. In that sense, gold may be confronting a challenge faced by nearly every parabolic asset: finding enough fresh demand after an extraordinary run higher.

The recent price action does not necessarily signal the end of the broader bull market. Gold remains far above levels seen a year ago, and many long-term investors continue to view the metal as a strategic portfolio allocation rather than a short-term trade.

But the character of the market appears to be changing. Earlier this year, investors were asking how high gold could go. Today, a growing number are asking whether the rally's strongest phase is already behind it.

Marina Lyubimova

Marina Lyubimova