Artem Voloskovets

Artem Voloskovets

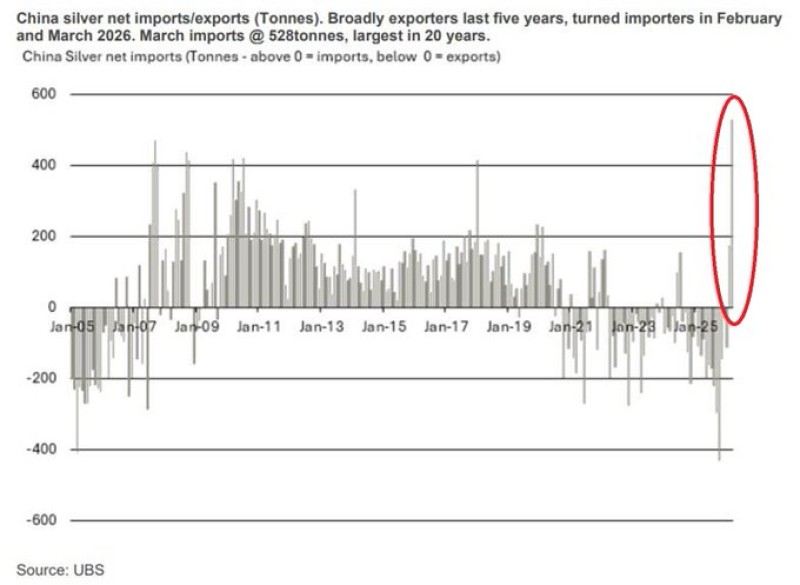

After spending much of the last five years as a net exporter of silver, the country abruptly flipped into aggressive imports in early 2026. According to UBS data, China imported roughly 528 tonnes of silver in March alone - the largest monthly inflow in nearly two decades. The move immediately caught the attention of commodity traders because physical silver flows often reveal deeper structural changes before prices fully react.

The chart above shows just how dramatic the reversal has been. After years of relatively weak imports and even periods of net exports, China suddenly became a major buyer of physical silver again. For the silver market, this matters far beyond one month of trade data.

The Market Was Already Facing a Supply Problem

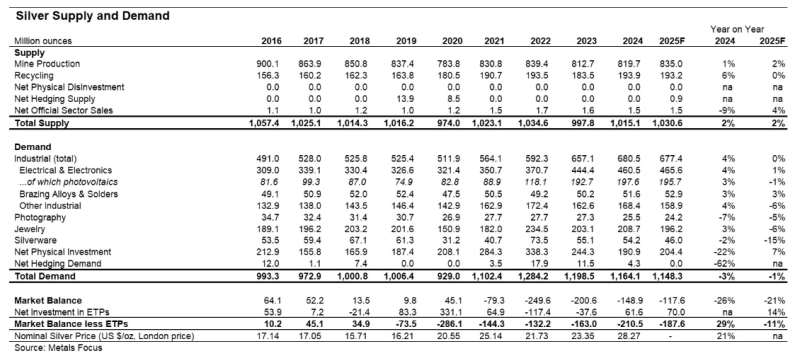

China’s buying surge is happening at a time when the global silver market has already been running persistent deficits for several consecutive years. According to Metals Focus data, silver demand has repeatedly exceeded available supply, creating one of the deepest structural shortages in decades. At the same time, physical investment demand through coins and silver bars has remained elevated.

That combination is important because it suggests the market was already tight before China sharply increased imports.

The deficit story becomes even more significant when looking at broader supply-and-demand trends.

Global silver demand surged from roughly 929 million ounces in 2020 to more than 1.16 billion ounces by 2024. Industrial demand alone climbed dramatically during that period, while the market balance remained deeply negative year after year.

Perhaps the most important figure in the data is solar demand. Silver consumption tied specifically to photovoltaics exploded from around 82.8 million ounces in 2020 to nearly 198 million ounces by 2024. In other words, the global green-energy transition is becoming one of the largest structural drivers of silver demand.

This helps explain why China’s sudden import surge may not be temporary. China remains the world’s dominant solar manufacturing hub, and the country’s demand for silver increasingly overlaps with strategic industries such as:

- solar panels;

- electronics;

- AI infrastructure;

- electric vehicles;

- advanced manufacturing.

That means silver is no longer viewed only as a precious metal or investment asset. It is increasingly behaving like a strategic industrial resource.

Physical Silver Inventories Are Falling Fast

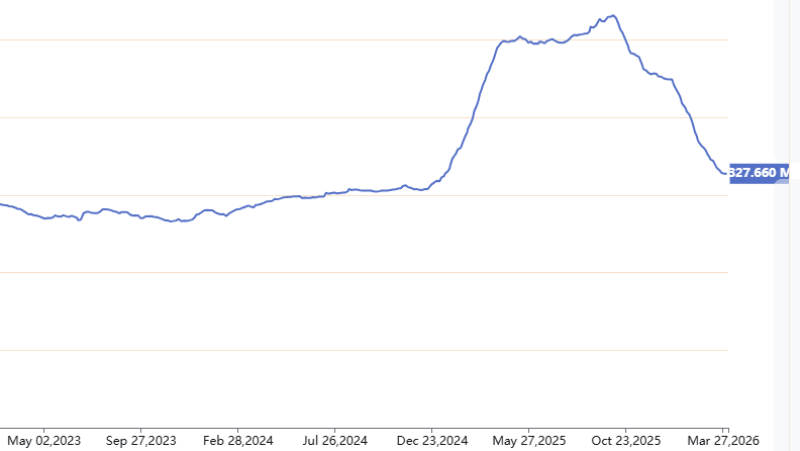

At the same time, another important signal has emerged in the physical market.

COMEX silver inventories surged during 2025 before sharply reversing lower in recent months. Available silver stocks have now fallen significantly from their peak levels, suggesting tightening physical supply conditions.

This creates a potentially powerful setup for the silver market:

- China is importing aggressively;

- global deficits remain persistent;

- solar demand continues rising;

- physical inventories are shrinking.

For commodity traders, this is the type of environment that can eventually produce supply squeezes and sharp price volatility.

Why Traders Are Watching Silver So Closely

The silver market is much smaller than the gold market, which means relatively modest shifts in physical demand can have an outsized impact on prices.

Unlike gold, silver also sits at the intersection of two powerful narratives:

- safe-haven and investment demand;

- industrial demand tied to energy and technology.

That combination makes silver uniquely sensitive to structural shortages. If China continues importing silver at elevated levels while inventories keep falling and industrial demand remains strong, the market could face one of its tightest supply environments in decades.

Artem Voloskovets

Artem Voloskovets