Marina Lyubimova

Marina Lyubimova

EDF’s decision to delay the sale of a stake in Edison until 2027 says less about the asset itself and more about how Europe’s infrastructure economy is changing under higher financing costs. Large utility assets benefited from an environment built around ultra-cheap capital, stable yield demand and aggressive infrastructure valuations. That framework is starting to break down.

The muted reaction to EDF’s postponement masks a larger shift now spreading across Europe’s energy sector: strategic infrastructure is becoming harder to finance, harder to value and increasingly difficult to sell at politically acceptable prices.

Cheap Infrastructure Capital Is Gone

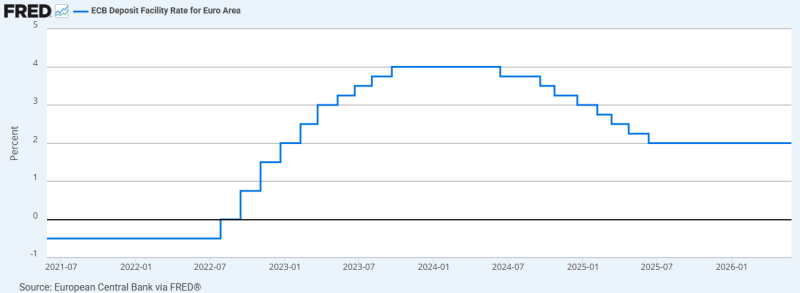

The ECB’s aggressive tightening cycle fundamentally changed how infrastructure-heavy businesses are priced across Europe. Utilities once traded like bond substitutes. Investors were willing to pay premium valuations for regulated cash flows because financing costs remained exceptionally low for years.

The ECB’s deposit facility rate moved from negative territory to nearly 4%, sharply increasing financing pressure across capital-intensive sectors.

The company is simultaneously managing:

- nuclear maintenance,

- grid modernization,

- electrification spending,

- and long-cycle energy transition investments.

Those obligations require massive amounts of long-duration capital precisely as financing conditions across Europe become structurally tighter. In that context, delaying the Edison stake sale looks less like indecision and more like a refusal to lock in weaker infrastructure valuations during a higher-rate cycle.

Strategic Energy Assets Are Becoming Harder to Value

EDF also operates under a uniquely political framework. The company is expected to maintain financial discipline while simultaneously supporting France’s broader energy-security strategy and industrial policy objectives.

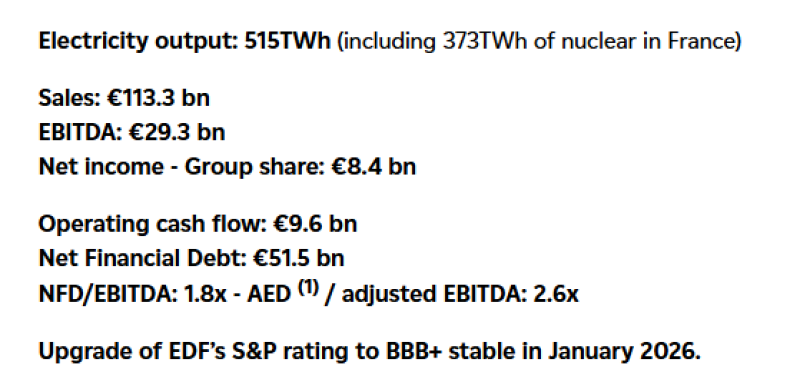

EDF reported €51.5 billion in net financial debt alongside major infrastructure investment commitments tied to Europe’s long-term energy transition. The issue extends well beyond EDF itself.

Across Europe, infrastructure-heavy companies are becoming more selective about asset disposals as higher financing costs reduce buyer appetite and compress transaction multiples. Fewer large transactions also create another problem: valuation discovery starts breaking down.

When fewer strategic infrastructure assets trade hands, it becomes harder for markets to establish reliable pricing benchmarks for future deals. That uncertainty alone can delay additional transactions.

Europe’s Energy Transition Is Entering a More Difficult Phase

Europe still wants:

- energy independence,

- accelerated electrification,

- grid expansion,

- and large-scale decarbonization investment.

Governments increasingly rely on utilities and infrastructure operators to carry strategic investment burdens while political scrutiny over energy prices continues to intensify. That creates a growing contradiction at the center of Europe’s energy transition: the continent needs more infrastructure spending precisely as infrastructure capital becomes more expensive.

For EDF, Edison is no longer just a balance-sheet asset. It represents part of a broader European energy footprint at a time when energy security has once again become strategically and politically sensitive.

The Bigger Shift Behind EDF’s Decision

The postponement of the Edison sale may ultimately prove less important than what it signals about Europe’s infrastructure economy more broadly. The era of abundant cheap money allowed governments, utilities and investors to assume that strategic energy assets would always command premium valuations. Higher rates are forcing markets to reconsider that assumption.

Europe’s energy transition still requires enormous amounts of capital. The question now is whether private markets remain willing to finance strategic infrastructure at the valuations utilities and governments became accustomed to during the zero-rate era.

Marina Lyubimova

Marina Lyubimova