Saad Ullah

Saad Ullah

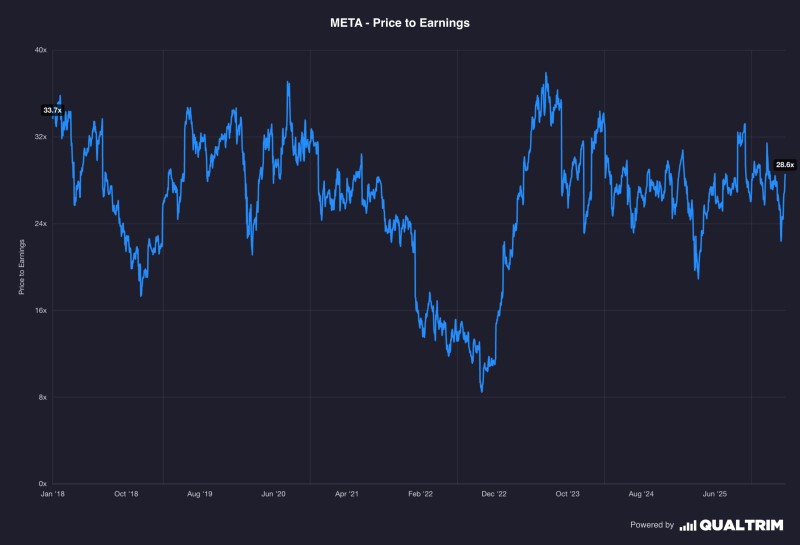

Meta Platforms is back in the valuation spotlight. Its price-to-earnings ratio sits around 28.6x - well below prior cycle highs but above the deepest compression levels seen in 2022. That leaves META in a kind of middle ground: not cheap relative to its trough, but still far from the most stretched points in its historical multiple range. According to Qualtrim, Bill Ackman's argument is that some of the best businesses in the market are available at unusually low valuations relative to their quality - and META is one of the names he highlights.

Some of the best businesses in the market are available at unusually low valuations relative to their quality - and META is one of the names highlighted.

A META Valuation Band the Market Keeps Returning To

The chart shows META's P/E ratio repeatedly oscillating within a broad multi-year band. Since 2018, the multiple has moved from the low teens at its weakest point to the mid-30s during stronger expansion phases. The current reading near 28.6x places the stock close to the middle of that long-term corridor rather than at either extreme.

That matters because it suggests the market is not aggressively repricing the company higher despite improved fundamentals. Instead, valuation has settled into a more stable range - consistent with earlier coverage noting that META's multiple has remained anchored in the mid-20s even as its AI narrative has strengthened. META P/E Ratio Holds Near 26x as AI Market Eyes $325B by 2033 captures that same pattern of a strong business trading inside a restrained valuation band.

META Revenue Up 30% but the Multiple Has Not Broken Out

The forward P/E sits at 22x against revenue growth of 30% year over year. That setup describes META as a company with strong earnings and revenue momentum while still trading at a relatively contained multiple. META Valuation Improves as EPS Surges from $10 to $25+ in Two Years highlights that earnings have expanded sharply while adjusted valuation has stayed comparatively moderate.

The stock's valuation is not behaving like a euphoric momentum name. The multiple appears capped within a known historical range, implying that fundamentals are improving faster than investor willingness to re-rate the stock dramatically.

That is the central feature of the current chart. Strong top-line growth does not automatically lead to major multiple expansion when the market is balancing growth optimism against scale, spending, and expectations. META Stock Holds $620 Level Despite 21% Revenue Growth makes a similar point - the market is treating earnings momentum and valuation expansion as two separate conversations.

A Market Repricing META Carefully, Not Aggressively

The chart does not show a breakout in valuation. It shows a normalization process. After the deep de-rating in 2022 and the sharp rebound that followed, META's P/E has spent much of the recent period moving sideways within a narrower band. That suggests investors are increasingly treating the company as a mature megacap with durable growth rather than a stock that deserves runaway multiple expansion.

Meta is enormous, still growing, and still central to AI and digital advertising conversations - but that scale can also keep valuation behavior more measured than in earlier phases of its lifecycle. Consider what that means in numbers:

- P/E ratio currently near 28.6x - mid-range within the 2018-present band

- Forward P/E of approximately 22x

- Revenue growth of 30% year over year

- EPS expansion from roughly $10 to $25+ over two years

- Market cap approaching the $1.6T range on a ~$190B revenue base

META's valuation setup looks less like a deep bargain and more like a high-quality company sitting in the middle of its long-term earnings multiple range - and that balance is exactly why the stock continues to attract attention.

If growth remains strong and the forward multiple stays restrained, that combination keeps META squarely in the conversation for investors looking for quality at a defensible price.

Saad Ullah

Saad Ullah