Artem Voloskovets

Artem Voloskovets

Combined with Anthropic’s previously reported $100 billion infrastructure agreement with Amazon, the AI startup has now committed roughly $300 billion in cloud spending despite not being publicly listed. The scale of those agreements alone exceeds the market capitalization of most public technology companies.

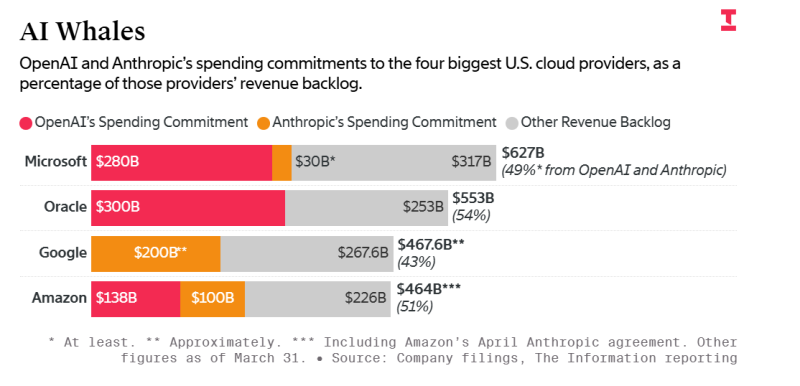

The chart highlights a remarkable shift inside the AI economy. OpenAI and Anthropic together now account for roughly half of the combined revenue backlog across the four largest U.S. cloud providers: Microsoft, Oracle, Google, and Amazon.

According to the data, OpenAI alone has committed approximately:

- $280 billion to Microsoft;

- $300 billion to Oracle;

- $138 billion to Amazon.

Anthropic, meanwhile, has reportedly committed:

- $200 billion to Google Cloud;

- $100 billion to Amazon.

Together, the two companies now represent one of the largest concentrated infrastructure demand pools in the history of the technology sector.

The Entire AI Infrastructure Trade Is Becoming Highly Concentrated

The implications for Wall Street are enormous.

Much of the current valuation expansion across mega-cap technology companies has been driven by expectations of accelerating AI infrastructure demand. Investors have rewarded Microsoft, Amazon, Alphabet, Oracle, and Nvidia based on the assumption that cloud growth, compute demand, and AI-related capital expenditures will continue compounding for years.

However, the latest data suggests that a substantial portion of that growth narrative may effectively depend on just two highly unprofitable startups: OpenAI and Anthropic.

That concentration risk is becoming increasingly difficult to ignore.

The broader AI infrastructure story that markets are currently pricing into big tech earnings increasingly resembles a massive long-duration bet that OpenAI and Anthropic can sustain extraordinary growth rates - potentially expanding revenues 20x to 30x by the end of the decade.

If that growth materializes, current cloud infrastructure spending may eventually appear justified. If it slows, however, the economics behind today’s AI capital expenditure boom could face much greater scrutiny.

Anthropic and OpenAI Are Taking Very Different Approaches

The two companies are also pursuing sharply different infrastructure strategies.

OpenAI has increasingly moved toward owning parts of its compute stack directly through the Stargate project and other data center initiatives. That approach may provide greater long-term control over hardware infrastructure, capacity allocation, and operating efficiency.

Anthropic, by contrast, appears to be pursuing a distributed infrastructure model.

Rather than relying on a single hyperscaler, the company is simultaneously locking in compute capacity across Google, Amazon, and Microsoft. The strategy reduces dependence on any single cloud provider while allowing Anthropic to scale rapidly without assuming the massive financial and operational risks associated with building proprietary data center infrastructure.

But the tradeoff is growing dependency on platform providers themselves.

Google’s role is especially notable because Anthropic is reportedly running large portions of its workloads on Google’s TPU chips rather than relying exclusively on Nvidia GPUs. That could significantly improve margins for Google Cloud while deepening Anthropic’s integration into Google’s proprietary hardware ecosystem.

Big Tech’s AI Revenue Boom Is Becoming More Interconnected

The chart also reveals how interconnected the modern AI ecosystem has become.

Cloud providers are no longer simply selling generic compute services. Instead, they are increasingly functioning as strategic infrastructure partners whose future growth depends heavily on a small number of AI model developers.

At the same time, AI startups themselves are becoming deeply reliant on hyperscalers for compute access, financing structures, networking infrastructure, and custom silicon.

This creates a new kind of concentration risk across the industry:

- cloud providers depend on AI startups for growth;

- AI startups depend on cloud providers for survival;

- investors depend on both continuing to scale at unprecedented speed.

The Scale of the AI Bet Keeps Expanding

The most striking takeaway may simply be the size of the numbers involved.

Infrastructure commitments measured in hundreds of billions of dollars were once associated primarily with governments, telecom buildouts, or national energy systems. Now they are increasingly tied to private AI companies that are still years away from mature profitability.

As the AI race accelerates, the cloud infrastructure boom is beginning to look less like a traditional software cycle and more like a global industrial expansion project built around compute, power, semiconductors, and data centers.

Artem Voloskovets

Artem Voloskovets