Editorial staff

Editorial staff

Every now and then, a company stops talking about what it could become and starts showing what it already is.

Datavault AI (NASDAQ: DVLT) may have just had that moment.

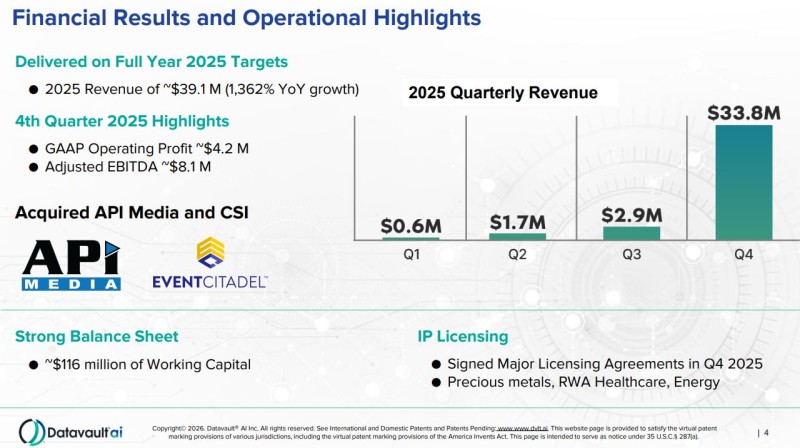

Fourth quarter revenue came in at $33.8 million. Not for the year. For the quarter. That single number did more than cap off a strong finish, it effectively rewrote the trajectory of the entire business. Full-year revenue landed at $39.1 million, meaning the engine didn’t just grow, it turned on.

And for the first time, it turned profitable.

By The Numbers...

Operating income of $4.2 million in Q4 marks a shift that investors have been waiting to see. Not theoretical leverage. Not future potential. Actual profitability, driven by real contracts, real counterparties, and real monetization of assets that until recently were still being positioned.

This is where the narrative changes.

Because Datavault isn’t presenting itself as another AI company chasing use cases. It’s positioning itself as the layer that monetizes them. Data, intellectual property, tokenization, licensing. These are not end products. They are infrastructure. And infrastructure, when it works, scales differently.

That distinction matters more now than it ever has.

A significant portion of the quarter was driven by large-scale licensing and data monetization agreements, including deals tied to tokenization frameworks. That’s not a one-off category. That’s a pipeline. And pipelines, once established, don’t reset every quarter. They build.

The market tends to underestimate that shift.

Development To Monetization...

When companies transition from development to monetization, the early quarters rarely look linear. They look like this. Quiet build, followed by step-function execution. The mistake is assuming that the spike defines the ceiling, when in many cases it’s simply the first visible layer of a much larger system coming online.

Datavault is now guiding toward approximately $200 million in revenue for 2026.

On the surface, that number looks aggressive. In context, it starts to look like math.

If Q4 represents the initial conversion of pipeline into revenue, then scaling that model across additional counterparties, verticals, and datasets becomes less about reinvention and more about replication. Licensing deals expand. Tokenization frameworks extend. Data becomes an asset class, not just an input.

That’s the bet.

And it’s not being made in a vacuum.

Institutions Are Buying The Story...

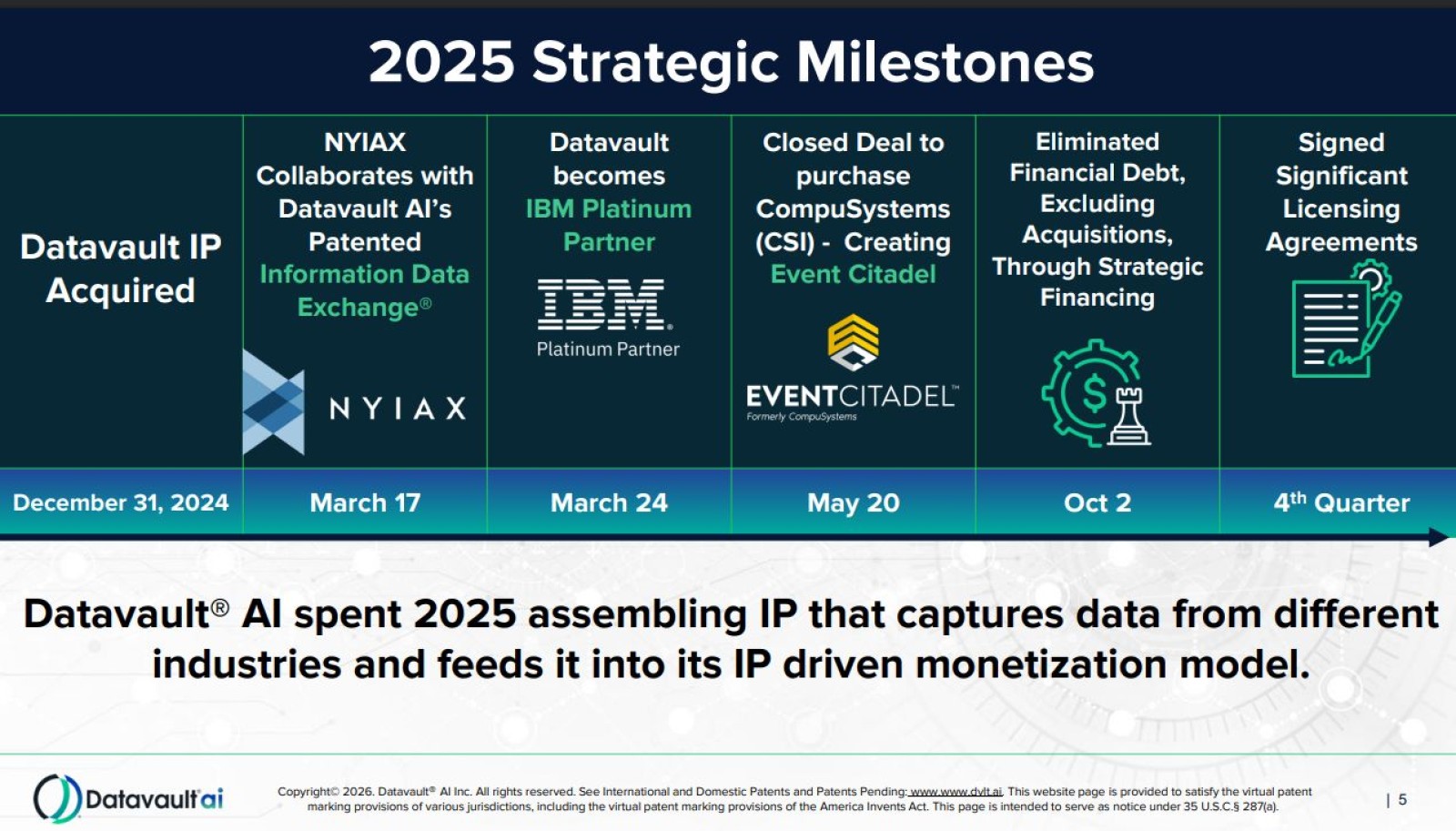

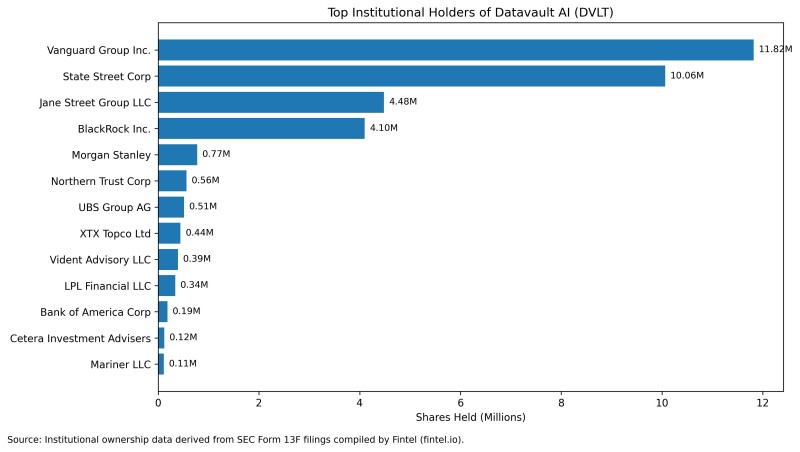

Institutional ownership has been building. Strategic acquisitions have expanded the company’s reach into events, media, and data infrastructure. The pieces are not being assembled randomly. They’re being layered. Each one feeding into a broader monetization engine that is only now starting to show what it can produce.

Even the balance sheet, often overlooked in growth stories, provides optionality. With over $100 million in working capital and no long-term debt, the company has room to operate, expand, and execute without being forced into defensive financing decisions.

That matters when momentum starts to build.

Because momentum, once it shifts, doesn’t move slowly.

It compounds.

The market’s initial hesitation following the release reflects a familiar pattern. Investors want to see it again. They want confirmation that Q4 wasn’t just strong, but sustainable. That’s a reasonable ask. But it also creates a window. Because by the time consistency is fully confirmed, the repricing has usually already begun.

Right now, Datavault sits in that gap. Between proof and recognition. Between what just happened and what the market is willing to fully price in.

And historically, that’s where the most asymmetric setups tend to emerge.

If the company executes even close to its stated trajectory, the conversation around Datavault shifts quickly. Not as a speculative AI play, but as a revenue-generating platform operating at the intersection of data, IP, and monetization infrastructure.

That’s a different category entirely.

And once a company moves into that category, it doesn’t tend to stay overlooked for long.

Editorial staff

Editorial staff