Eseandre Mordi

Eseandre Mordi

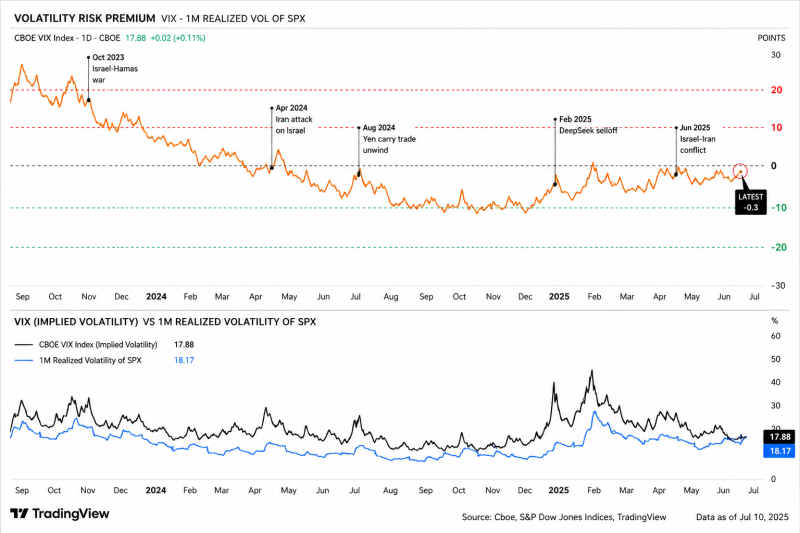

The volatility risk premium - the spread between the CBOE Volatility Index and 1-month realized volatility on the S&P 500 - has compressed to ~0–2 points, with a recent dip into negative territory near -5. For context, the long-term norm sits closer to +4–6 points, meaning the market has effectively lost its usual “insurance buffer.”

On the chart, realized volatility (blue) recently spiked to roughly 50–55% annualized during the early-2025 shock, while VIX peaked near 45–50. That inversion - realized exceeding implied - is rare and typically short-lived. Now both have normalized, but the key issue is how they normalized: VIX has fallen faster than realized volatility, leaving the premium structurally compressed.

Volatility is mispriced - here’s the problem:

- Options sellers lost edge With the premium near zero, the typical carry from selling volatility has dropped from ~5 points historically to almost nothing. Risk/reward is no longer asymmetric in their favor.

- Market is pricing “no new shocks” Current VIX levels around 13–15 imply calm conditions, while realized volatility still sits closer to 15–20. That gap suggests the market is assuming stability despite recent instability.

- Fragility is increasing Every time the premium approached 0 or below in the past two years, it was followed by a volatility spike of +10–20 VIX points within weeks.

- Positioning risk is building Systematic vol-selling strategies typically scale up when VIX drops. With low premium, this creates crowded positioning that can unwind quickly.

The key pain point: there is no buffer left. When VIX trades at a healthy premium, markets can absorb shocks without sharp repricing. At ~0 premium, even a minor catalyst - macro data, geopolitics, or liquidity stress - can trigger an outsized move.

Bottom line: the market has shifted from pricing risk to assuming stability. Historically, that transition doesn’t last - it resolves either through continued compression (rare) or a fast volatility spike. Right now, the numbers suggest the second scenario is increasingly likely.

Eseandre Mordi

Eseandre Mordi