Saad Ullah

Saad Ullah

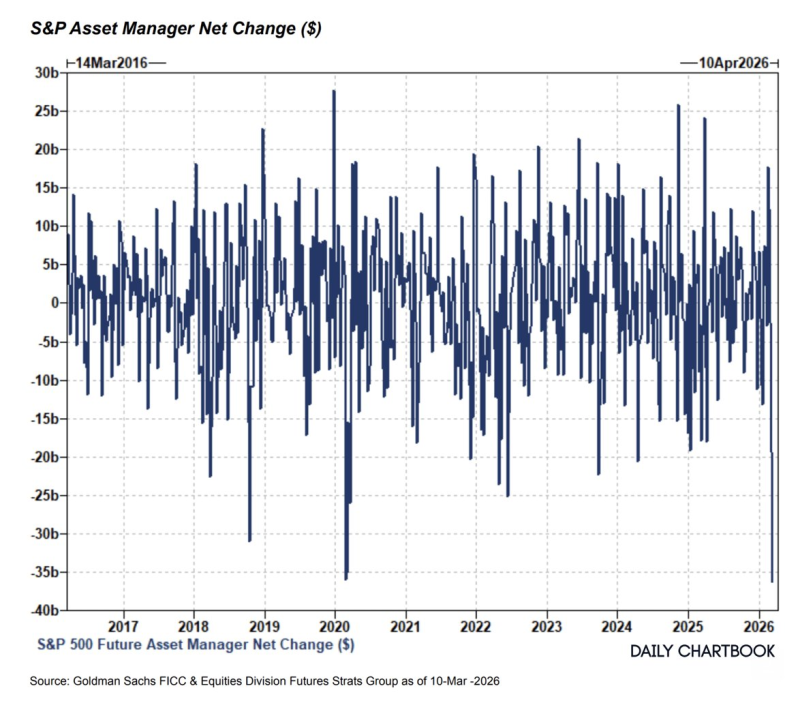

Institutional sentiment in equity markets shifted dramatically as asset managers slashed their exposure to S&P 500 futures. Between March 3 and March 10, a staggering $36.2 billion in contracts were offloaded, marking the largest single-week selloff in more than ten years.

Historical data stretching from 2016 to 2026 reveals just how unusual this move is. Asset manager net positioning in S&P 500 futures swings regularly between positive and negative, but the latest reading approaches the extreme lower bound near -$35 billion. That puts this episode firmly among the most severe positioning shifts in the entire dataset.

The scale of the latest outflow underscores how quickly institutional sentiment can change in the S&P 500.

Large-scale repositioning by institutions rarely happens in isolation. Risk-off behavior tends to spread across asset classes simultaneously, as covered in BTC, S&P 500, and Gold All Drop Below Key Levels in a Synchronized Risk-Off Sell-Off. Equity futures are especially sensitive to macro-driven flows, a dynamic also reflected in reporting on Nasdaq and S&P 500 Futures Flat as Bitcoin Holds Near $73K.

A selloff of this magnitude carries practical consequences beyond price moves. Rapid futures outflows can tighten liquidity and amplify short-term volatility. For traders watching institutional positioning, the data signals a clear shift in risk appetite, one that warrants close attention as macro uncertainty continues to drive market behavior.

Saad Ullah

Saad Ullah