Eseandre Mordi

Eseandre Mordi

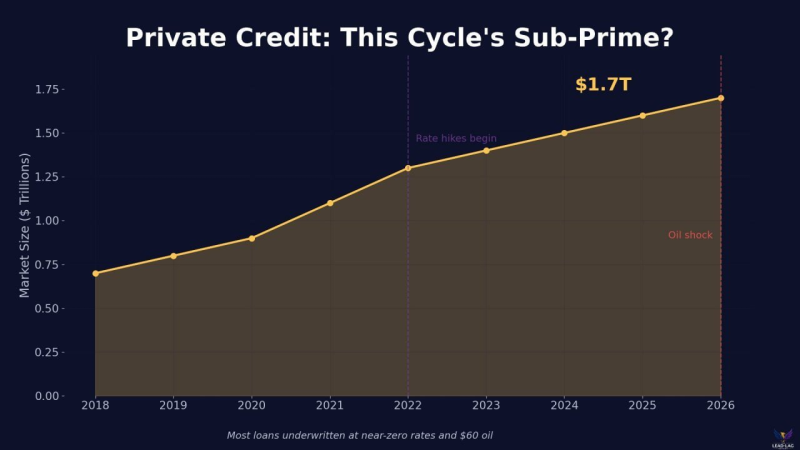

The private credit market has grown into one of the most closely watched corners of global finance, and not always for the right reasons. From roughly $0.7 trillion in 2018, it has nearly tripled in size by 2026, crossing the $1.7 trillion mark even as borrowing costs climbed sharply. The trajectory raises questions that markets are only beginning to ask out loud.

$1.7 Trillion and Growing: How Private Credit Outpaced the Rate Cycle

What makes this expansion unusual is its timing. Rate hikes that began in 2022 would typically slow lending activity, yet private credit vs. bank loans data shows the market continued to grow regardless. Much of the underlying loan book was written during a period of near-zero interest rates and low energy costs, conditions that shaped both lender assumptions and borrower repayment capacity. As those assumptions are tested, the structural risks embedded in that growth are becoming harder to ignore.

Private credit operates outside traditional banking channels, which means it carries less regulatory oversight and far less transparency. Valuations are self-reported, defaults do not always surface quickly, and liquidity can evaporate faster than it appears. This opacity is the core concern.

Oil Shocks, Margin Compression, and the Hidden Default Risk

Macro pressure is adding another layer of strain. Rising energy prices are compressing corporate margins, particularly for borrowers whose business models assumed stable input costs. When those costs rise sharply, debt service becomes harder to maintain, and in a market where valuations are not marked to market daily, the damage can accumulate quietly. Alternative asset investing strategies literature flags exactly this dynamic, noting that private credit is especially sensitive to default risk in higher-rate environments.

The comparison to subprime is not about identical mechanics. It is about the pattern: rapid growth fueled by cheap money, concentrated risk outside the regulated system, and limited visibility until conditions shift. Private credit at $1.7 trillion is now large enough that stress within it would not stay contained. Whether that stress is already building beneath the surface is the question investors and regulators are watching most carefully.

Eseandre Mordi

Eseandre Mordi