Artem Voloskovets

Artem Voloskovets

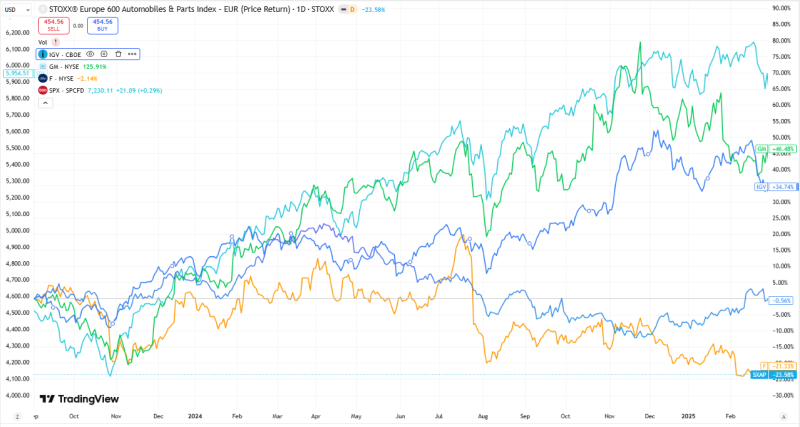

European automotive stocks have declined sharply since early 2025, with markets signaling that tariff risks were priced in well before any official measures took effect. The selloff reflects growing investor concern over trade exposure, particularly for companies heavily reliant on exports to the United States.

The STOXX Europe 600 Automobiles & Parts Index has dropped by more than 23% over the period, significantly underperforming U.S. automakers. In contrast, General Motors has posted strong gains of over 40%, while Ford Motor Company has remained relatively stable. This widening gap highlights a clear divergence in how investors are positioning across regions.

This trend has been widely reflected in market behavior, with investors adjusting expectations early in response to potential tariff measures. Concerns include higher export costs, weakening demand in key markets, and pressure on profit margins for European manufacturers. These risks fit into a broader market debate around global trade imbalances and how tariffs can reshape sector valuations.

At the same time, U.S. automakers appear to be in a more insulated position. Domestic production, pricing power, and reduced exposure to cross-border trade risks have helped support valuations. General Motors has also drawn attention for General Motors’ capital allocation strategy, which adds another reason why investors may treat U.S. names differently from European peers.

Artem Voloskovets

Artem Voloskovets