Victoria Bazir

Victoria Bazir

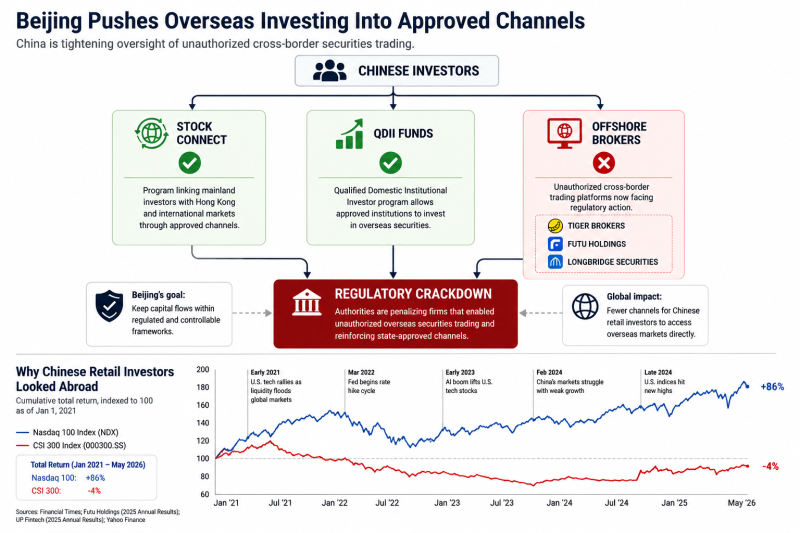

China's latest crackdown on illegal cross-border securities trading is not simply a regulatory action against a handful of brokerages. It is a direct challenge to one of the fastest-growing channels connecting Chinese retail investors with global markets.

According to the Financial Times, regulators are moving against offshore brokerage platforms that allowed mainland investors to buy foreign securities outside approved regulatory frameworks.

The decision highlights a broader shift in Beijing's approach to international investing. Rather than preventing overseas investment altogether, authorities are steering investors toward approved programs such as Stock Connect and QDII while restricting alternative channels that operate outside direct regulatory oversight.

The scale of the affected market is substantial.

One of the industry's largest players, Futu Holdings, reported HK$1.24 trillion ($158 billion) in average client assets during the fourth quarter of 2025, up 71% year-over-year. Funded accounts reached 3.37 million, while total client assets increased 65.9% from the previous year.

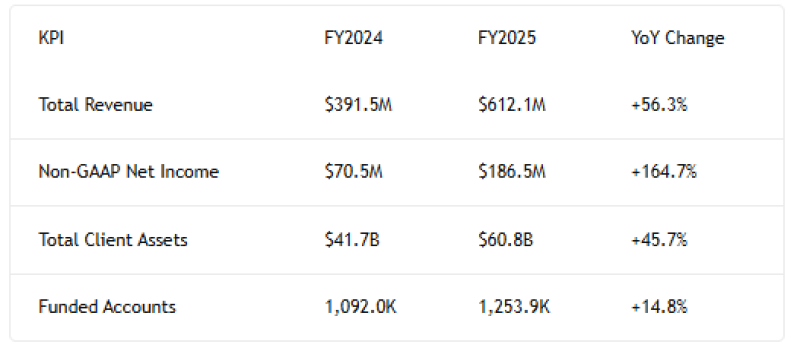

Tiger Brokers also reported strong growth. Total client assets rose to $60.8 billion, an increase of 45.7% year-over-year, while revenue climbed 56.3% to $612.1 million. The platform ended the year with approximately 1.25 million funded accounts.

Those figures suggest that offshore investing has become a significant business rather than a niche activity. The question is why demand became so strong in the first place.

The performance gap between U.S. and Chinese equities offers a straightforward explanation. Since January 2021, the Nasdaq 100 has gained approximately 86%, while China's CSI 300 has declined around 4%. Foreign markets provided access to stronger returns, particularly in large-cap technology stocks. Offshore brokerages became one of the easiest ways to capture that performance.

Beijing's latest action does not eliminate overseas investing. It changes who controls the gateway. For global markets, the immediate impact may be limited. Approved investment channels remain open, and institutional flows are unlikely to disappear. The longer-term implication is different: access to Chinese retail capital may increasingly depend on state-approved infrastructure rather than privately built brokerage networks.

The crackdown therefore represents more than a compliance story. It marks another step in China's effort to keep cross-border capital flows visible, regulated, and ultimately under government control.

Victoria Bazir

Victoria Bazir