Marina Lyubimova

Marina Lyubimova

The U.S. Treasury will auction $85 billion in 4-week Treasury bills on May 28, with settlement scheduled for June 2. On the surface, the announcement looks routine. Short-dated bill auctions are a regular feature of the government's funding calendar and rarely attract much attention outside fixed-income circles. The broader backdrop, however, is becoming harder to ignore.

Federal Debt Servicing Costs Continue to Climb

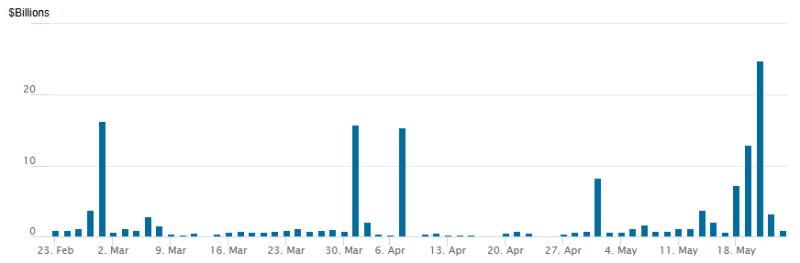

Recent Treasury data show federal interest payments repeatedly climbing into the double-digit billions of dollars on individual days. In May alone, one payment spike exceeded $20 billion, highlighting how expensive it has become to service the country's growing debt burden. While such payments follow a scheduled pattern rather than a sudden deterioration in public finances, they underscore the scale of financing operations required to keep the federal government running.

The increase in interest costs reflects a new reality for federal finances. Much of the debt accumulated during years of near-zero rates is now being refinanced at substantially higher yields, pushing debt-servicing expenses upward even without a dramatic increase in borrowing volumes.

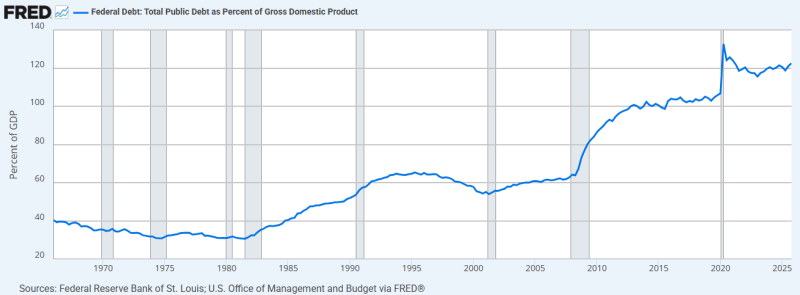

US Debt-to-GDP Ratio Remains Near Historic Highs

That burden is tied to a debt stock that remains historically elevated. According to Federal Reserve data, total U.S. public debt stands at roughly 120% of GDP, a level that would have been difficult to imagine before the financial crisis and one that has remained stubbornly high even after the pandemic-era borrowing surge faded.

The trajectory is striking. Federal debt represented less than 40% of GDP through much of the 1970s and early 1980s before beginning a decades-long climb driven by successive recessions, fiscal stimulus programs and structural budget deficits. The pandemic accelerated that trend, pushing debt levels to records that have yet to meaningfully reverse.

Against this backdrop, the Treasury continues to rely heavily on the short end of the curve. Four-week bills offer flexibility: investors face minimal duration risk, while the government can quickly adjust borrowing volumes as funding needs change. The tradeoff is equally obvious. Debt that matures in a month must soon be refinanced, forcing Washington to return to the market again and again.

The strategy has worked so far. Money market funds, cash managers and institutional investors have consistently absorbed large bill auctions, attracted by yields that remain well above pre-2022 levels. Strong demand has allowed the Treasury to issue vast quantities of short-term debt without significant disruption to funding markets.

Still, each auction serves as a reminder of the scale involved. An $85 billion sale is no longer exceptional in today's Treasury market. It is part of a financing machine that supports more than $36 trillion in federal obligations and a debt-to-GDP ratio hovering near post-war highs. The upcoming 4-week bill sale may be routine. The fiscal backdrop behind it is anything but.

Marina Lyubimova

Marina Lyubimova