Marina Lyubimova

Marina Lyubimova

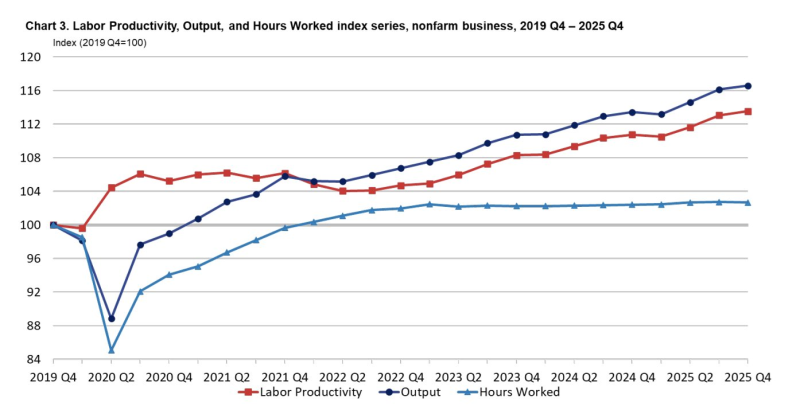

US nonfarm business productivity gained 1.8% annualized in Q4 2024 - revised down from the initial 2.8% estimate - as the economy continued to squeeze more output from a largely flat labor base. Output grew 1.5% while hours worked slipped 0.2%, extending a pattern that has defined the post-2022 labor market. Hours have plateaued around the 102-103 index level since then, even as economic output climbed toward 116 by 2025 and labor productivity pushed above 112.

Annual Productivity Trend Points to Above-Average Efficiency Gains

Zooming out, labor productivity rose 2.5% year-over-year from Q4 2024 to Q4 2025, with the annual average up 2.1% between 2024 and 2025. Both readings sit above long-run trend. That kind of sustained improvement gives businesses more room to grow revenue without adding proportional headcount - and crucially, without stoking wage-driven inflation. According to the Fed GDP growth and inflation outlook, expectations for stable expansion are directly tied to how productivity dynamics evolve through 2026.

Efficiency Gains Support Non-Inflationary Growth Potential

The macroeconomic case for optimism rests on a simple equation: if businesses can expand output without expanding hours, potential GDP rises without adding inflationary pressure. This aligns with broader signals tracked in AI productivity and GDP growth trends, where technology investment is increasingly credited for efficiency gains even as traditional hiring slows. Complementary labor data in US labor market and economic recovery signals reinforces the view that the economy may be finding a new, more efficient steady state - one where productivity, not headcount, drives the next leg of growth.

Marina Lyubimova

Marina Lyubimova