Marina Lyubimova

Marina Lyubimova

MiCA is the first comprehensive framework that brings stablecoins into a regime comparable to traditional e-money. It does not simply “regulate crypto”; it redefines liquidity by imposing reserve quality, redemption rights, and authorization rules on issuers and service providers. For traders in Europe, the visible outcome is already emerging: fewer trading pairs, thinner books, and a gradual shift from global (USDT-driven) liquidity to compliant instruments.

The Regulatory Core: Why Stablecoins Must Change

MiCA’s impact on liquidity is anchored in a small set of provisions that directly constrain how stablecoins are issued and used:

| Provision | Source | What it enforces | Market consequence |

| Reserve of assets | Article 36(1) | Full backing at all times | Limits balance-sheet flexibility |

| Liquidity composition | Article 36(4), RTS by European Banking Authority | High-quality, short-maturity reserves | Reduces yield strategies |

| Authorization of providers | Article 63 | CASP licensing across the EU | Forces exchange compliance |

| Redemption rights | Article 55 | Timely redemption at par | Constrains stress scenarios |

| Transitional regime | Article 143 | Phase-in until July 2026 | Temporary coexistence |

The practical implication is straightforward: a stablecoin becomes a regulated monetary instrument, not just a trading bridge. Assets that cannot meet these constraints will not be able to remain listed on EU-regulated venues.

The implications of stablecoin regulation extend beyond Europe. Similar regulatory pressure is emerging globally, particularly in the United States, where stablecoin policy decisions are expected to impact liquidity conditions for major crypto assets. A recent example shows how regulatory deadlines can influence market expectations and positioning, as discussed in BTC and ETH reaction to stablecoin regulation timelines.

Which Stablecoins Fit the MiCA Model

Under MiCA, compliance is not theoretical; it is operational and jurisdictional. The market is already separating into compliant and non-compliant assets:

| Stablecoin | EU status | Structural reason |

| USDT (Tether) | Non-compliant | No EU authorization; reserve transparency concerns |

| USDC (Circle) | Compliant | E-money institution structure and MiCA alignment |

| EURC | Compliant | Native EU-focused issuance |

| DAI | Unclear | Decentralized governance vs. regulatory accountability |

Circle has already positioned USDC and EURC within the MiCA framework, while assets like USDT face structural incompatibility with the regime. This difference is not cosmetic; it determines where liquidity can legally exist.

As MiCA entered into force, market share began to shift toward compliant instruments. Data indicates a rapid increase in EUR-denominated and compliant stablecoin usage, while non-compliant assets continue to dominate globally but lose relevance in the EU context.

This is the first key conclusion: MiCA does not remove liquidity; it relocates it—from non-compliant tokens to compliant ones, and from offshore venues to regulated exchanges.

Delistings Are Not Optional - They Are Required

Exchanges operating in Europe must comply with MiCA’s asset eligibility rules. This has already translated into concrete actions by major platforms such as Binance and Coinbase, which have announced or initiated removals of non-compliant stablecoins for EEA users.

Delisting, therefore, is not a discretionary business choice. It is the mechanical outcome of regulation: if an asset cannot meet MiCA requirements, it cannot be offered on EU-regulated venues.

Liquidity Structure: What the Numbers Show

The dominance of USDT becomes clear when examining trading volumes across pairs. Despite increasing regulatory pressure in Europe, USDT remains the primary source of global crypto liquidity, particularly on offshore exchanges. Its scale continues to shape market structure, even as its role within the EU weakens under MiCA.

| Pair | Exchange | 24h Volume |

| BTC/USDT | Binance | ≈ $1.1B |

| BTC/USDC | Binance | ≈ $327M |

| BTC/EUR | Coinbase | ≈ $14M |

The gap between global (USDT) and EU-aligned (USD/EUR) liquidity is orders of magnitude, which directly affects execution quality. As USDT pairs are restricted in the EU, local liquidity inevitably becomes thinner.

For example, recent market shifts show how Tether still maintains a leading position in the ecosystem, as highlighted in Tether’s changing position in the crypto market.

Even when prices appear aligned across exchanges, small and persistent deviations exist between global venues and EU-regulated platforms. These discrepancies widen during periods of volatility, indicating that arbitrage is less efficient when liquidity pools are segmented.

The implication is subtle but important: price discovery begins to fragment. Under MiCA, Europe becomes a partially insulated liquidity zone rather than a seamless part of the global market.

Liquidity concentration is not unique to Bitcoin pairs. Similar patterns can be observed across altcoin markets, where trading activity rapidly clusters around specific assets and exchanges. For instance, sharp spikes in trading volume often signal short-term liquidity migration rather than long-term capital inflow, as seen in XRP trading volume surge above $3 billion.

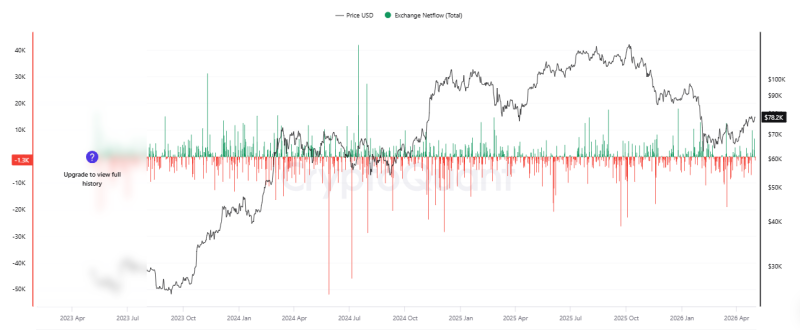

Capital Flows Confirm Redistribution, Not Exit

On-chain data from CryptoQuant shows that exchange netflows oscillate around neutral levels over time. There is no sustained evidence of capital leaving the market.

Instead, flows alternate between inflows (potential selling) and outflows (accumulation), reinforcing a central conclusion: liquidity is being reallocated across jurisdictions and assets rather than disappearing.

Market Depth: The Invisible Cost of Regulation

Market depth determines how much capital can be traded without moving the price. Global exchanges, particularly those dominated by USDT liquidity, exhibit dense order books and tight spreads.

As MiCA restricts non-compliant assets, EU venues will operate with:

- fewer participants,

- fewer large orders near the mid-price,

- and reduced depth.

This translates directly into wider spreads, higher slippage, and less efficient execution for traders operating within the EU.

Putting It Together: The New Market Structure

The combined evidence - from regulation, market share, volumes, prices, flows, and depth - points to a layered market:

| Layer | Assets | Liquidity profile |

| Global (offshore) | USDT pairs | Deep, dominant, highly efficient |

| Transitional | Mixed assets | Medium, shifting |

| EU-compliant | USDC, EURC, fiat pairs | Lower depth, regulated |

This structure is not temporary; it is the intended outcome of MiCA.

Conclusion

MiCA does not reduce the size of the crypto market. It reorganizes liquidity along regulatory lines. Non-compliant stablecoins such as USDT lose access to EU venues, compliant assets like USDC and EURC gain relevance, and trading conditions in Europe become structurally different from those in global markets.

The final implication is unavoidable:

Stablecoin delistings in the EU are not a short-term disruption. They are the predictable and inevitable consequence of a regulatory system that redefines what liquidity is allowed to exist.

Marina Lyubimova

Marina Lyubimova