Victoria Bazir

Victoria Bazir

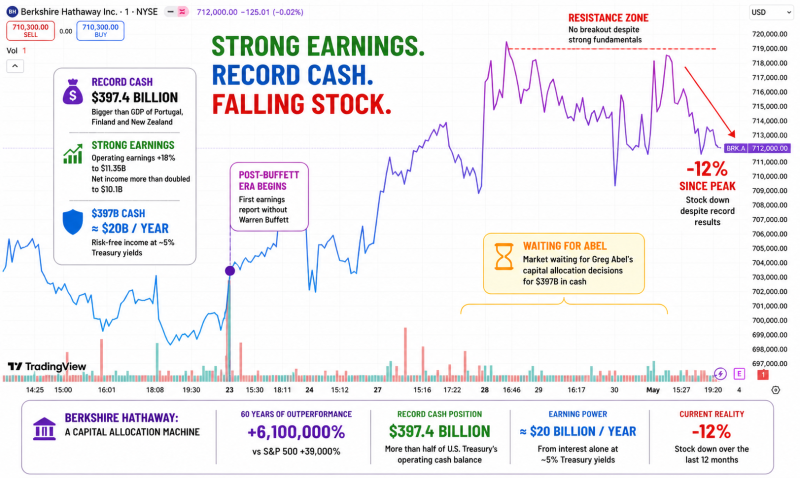

Berkshire Hathaway has entered a new era, releasing its first earnings report in 60 years without Warren Buffett leading the company. On the surface, the numbers remain strong, but the broader context reveals a more complex and underreported story.

Record Cash Is More Than Just a Number

The company’s cash reserves climbed to a record $397.4 billion, exceeding the GDP of countries such as Portugal and Finland. At current Treasury yields near 5%, this capital can generate roughly $20 billion annually without active investment.

This buildup did not happen in isolation. Berkshire has been steadily increasing liquidity while reshaping its portfolio, as highlighted in Berkshire Hathaway recent moves involving ULTA and Sirius XM, signaling a selective and tactical approach to capital allocation.

A Deliberate Shift in Strategy

Operational performance remains strong, with operating earnings rising 18% to $11.35 billion and net income more than doubling year-over-year. Yet the more telling signal lies in capital allocation.

Berkshire continues to reduce its exposure to equities, selling $24.1 billion in stocks while purchasing only $16 billion. This pattern has now persisted across multiple quarters, reinforcing the idea that the company is not reacting to markets - it is positioning ahead of them.

That positioning is becoming more extreme. According to recent data, Berkshire’s cash has reached historically high levels relative to total assets, as noted in Berkshire Hathaway analysis showing cash nearing multi-decade highs. This underscores just how defensive, and potentially opportunistic, the current stance is.

Reading Between the Lines

Historically, Berkshire has built large cash positions ahead of major market dislocations, including the dot-com collapse, the 2008 financial crisis, and the 2020 pandemic sell-off. The current environment - defined by high interest rates and elevated valuations, shares similar characteristics.

Recent reporting confirms that Berkshire’s cash has surged to record levels partly due to a lack of attractive opportunities and a cautious stance under new leadership . This suggests the strategy is not passive, but intentional.

Viewed through that lens, the growing cash pile looks less like inactivity and more like preparation. The strategy creates a rare asymmetry: consistent income from Treasuries combined with the ability to deploy massive capital quickly if valuations reset.

Why the Stock Is Falling

Despite strong fundamentals, Berkshire’s stock has declined around 12% over the past year. The disconnect reflects uncertainty rather than weakness.

Investors are now focused on Greg Abel and how he will deploy one of the largest cash reserves in corporate history. Markets are effectively pricing in transition risk, questioning whether Buffett’s discipline and timing can be replicated.

The Long-Term Perspective

The chart above puts the current situation into context. Berkshire has delivered approximately 6,100,000% returns over 60 years, dramatically outperforming the S&P 500.

Against that backdrop, a 12% decline appears modest, but it highlights how sensitive markets are to uncertainty around leadership and future strategy.

Conclusion

Berkshire Hathaway is not weakening - it is repositioning. Record cash, rising profits, and a falling stock price are not contradictions, but signals of a market waiting for clarity. The next phase will depend not on what Buffett built, but on how that foundation is used going forward.

Victoria Bazir

Victoria Bazir