Peter Smith

Peter Smith

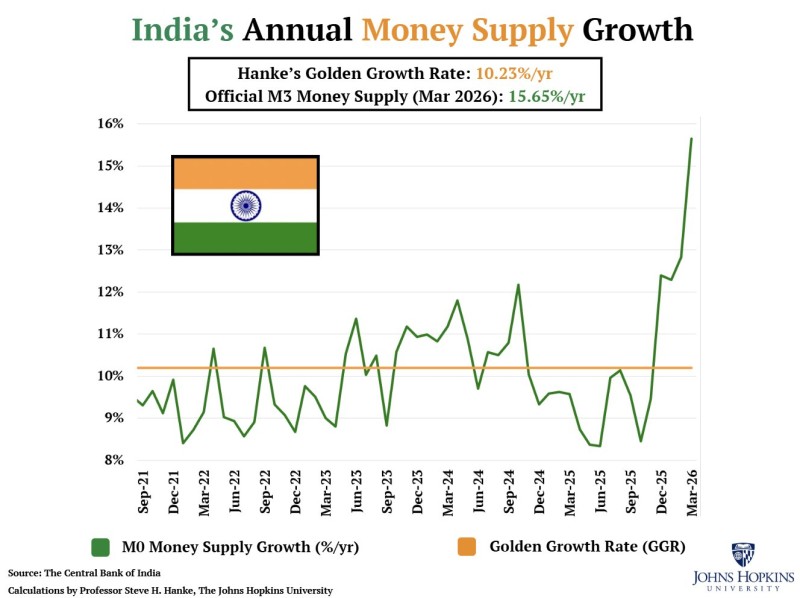

India's inflation story is drawing fresh attention after consumer prices edged up from 3.2% year over year in February to 3.4% in March. The more striking figure, however, is the M3 money supply, now growing at 15.65% annually - a level that economist Steve Hanke flags as well above his estimated Golden Growth Rate of 10.23% per year, the pace consistent with India's 4% inflation target. With monetary expansion running this far ahead of the benchmark, the latest data points to a widening gap between money growth and price stability.

India's M3 Money Supply Breaks Above the Golden Growth Rate Benchmark

From late 2021 through much of 2023, money supply growth moved around the 10% area - sometimes dipping below it, sometimes pushing modestly above. Those swings were volatile, but they stayed relatively close to the benchmark line.

That changed in the latest stretch. By late 2025 and into early 2026, the trend turns sharply higher, breaking above prior peaks and reaching 15.65% in March 2026. That is the highest reading on the chart and a clear departure from the earlier range.

India's official M3 money supply is now growing at 15.65% per year, well above the Golden Growth Rate of 10.23% per year needed to keep inflation anchored at 4%

Earlier fluctuations in India's money supply repeatedly returned toward the Golden Growth Rate line. The newest move does not.

India's Money Supply Breakout Changes the Inflation Narrative

What matters in this setup is not only the latest number, but the structure of the move. Instead of reverting to the benchmark, the chart shows an acceleration phase - money supply growth pushes higher, briefly pauses, and then extends again into a fresh high. In technical terms, the pattern shifts from range-bound oscillation to an upside breakout.

The move above 12%, then above 13%, and finally toward 16% suggests the deviation is no longer minor - it has become pronounced enough to reshape the broader inflation discussion

That makes the current signal more important than a one-month jump. The deviation is no longer minor. It has become pronounced enough to reshape the broader inflation discussion.

India Inflation at 3.4% Still Lags the Monetary Signal

Inflation itself has not moved nearly as sharply as money supply. The increase from 3.2% to 3.4% is modest on its face, but the core point is that monetary expansion is running much hotter than the level associated with stable prices.

India's inflation previously came in at 3.21% in February as M3 money supply growth topped the 11% optimal rate - and the spread has only widened since. The orange benchmark line stays flat near 10.23%, while the green money supply line ends the period far above it. That gap is now the widest visible on the chart.

If there is one message in the data, it is this: the inflation story is being framed as a money supply story. March's uptick may still look limited, but the monetary backdrop has already moved much more aggressively

March's inflation uptick may still look contained. The monetary backdrop, however, has already moved aggressively - and that is the signal worth watching.

Peter Smith

Peter Smith