Artem Voloskovets

Artem Voloskovets

That consensus leaves little room for surprises next week. The more interesting question is why prediction markets continue to price a meaningful probability of another rate hike years after the most aggressive tightening cycle in decades.

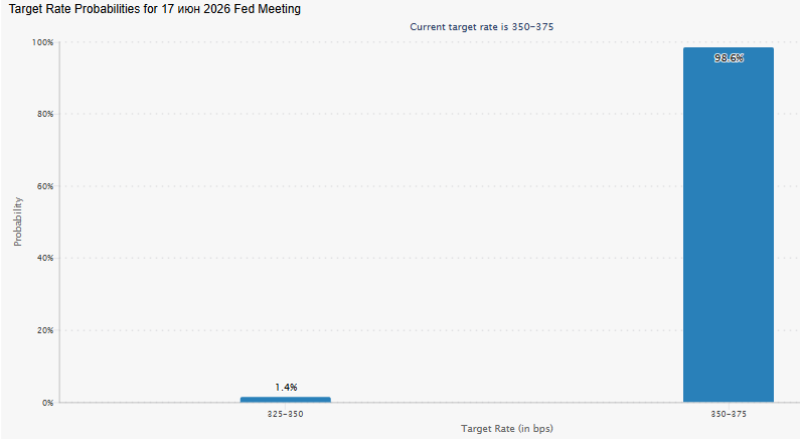

June Is Not The Story

Fed funds futures imply almost complete agreement on the outcome of the June meeting. Markets see a 98.6% chance of rates remaining unchanged and only a 1.4% chance of a quarter-point cut. Expectations for a hike are effectively absent.

Under normal circumstances, such pricing would suggest confidence that inflation risks are fading. Other indicators suggest otherwise.

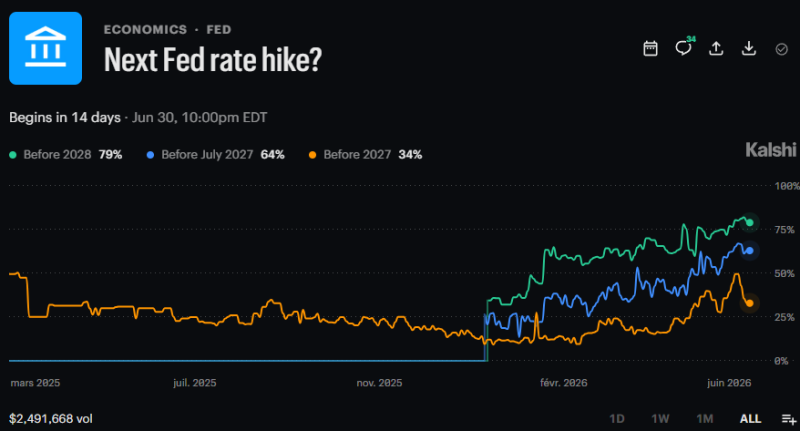

A Different Message From Prediction Markets

Kalshi contracts tied to future Federal Reserve policy show rising expectations that the next move after the current pause could eventually be another hike. The probability of a hike before 2028 has climbed to roughly 79%.

Contracts tied to shorter timeframes imply:

- 64% probability of a hike before July 2027;

- 34% probability of a hike before 2027.

The move has been gradual rather than sudden, reflecting a steady reassessment of inflation risks rather than a reaction to a single economic release. The gap between FedWatch and Kalshi is not a contradiction. One measures expectations for the next meeting. The other measures expectations over several years.

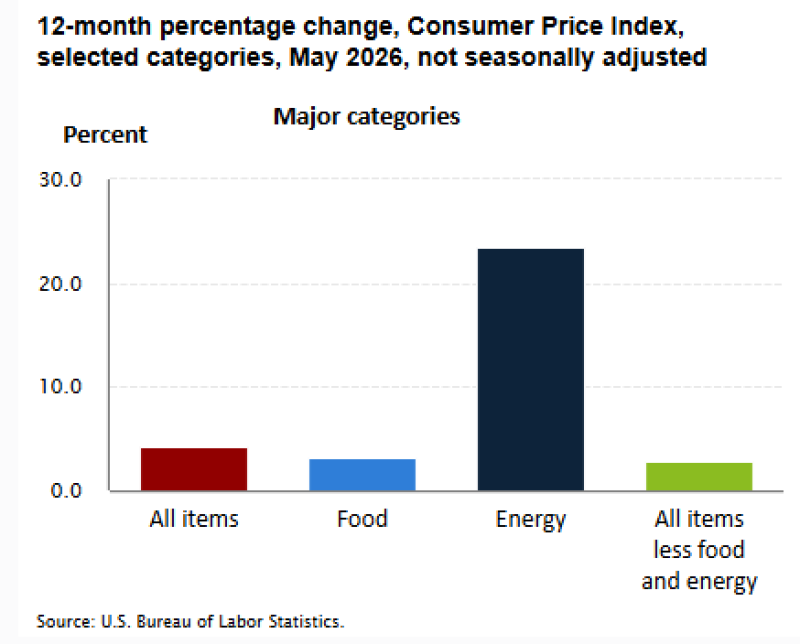

Inflation Is Still Running Above Target

The latest CPI report explains much of the market's caution. Consumer prices increased approximately 4% year-over-year in May, while core inflation remained close to 3%.

The most notable figure came from energy, where prices rose more than 23% compared with a year earlier.

| Category | Annual Change |

| All Items | ~4.0% |

| Food | ~3.0% |

| Energy | ~23.5% |

| Core CPI | ~3.0% |

The Federal Reserve targets inflation of 2%. While inflation has fallen significantly from its peak, current readings remain high enough to prevent policymakers from declaring victory.

The energy component deserves particular attention because sharp increases in fuel and utility costs have historically filtered through transportation, production, and consumer prices.

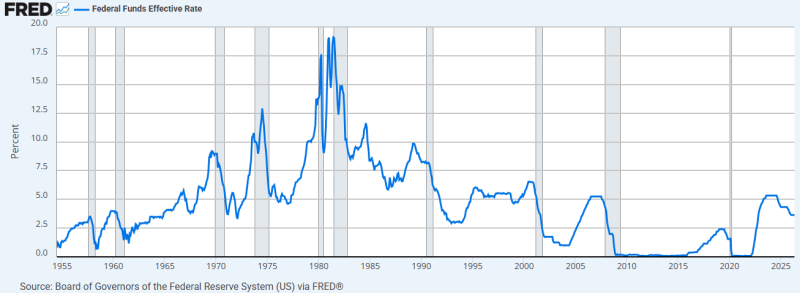

Rates Are High By Recent Standards, Not By Historical Standards

The current effective federal funds rate is approximately 3.6%. That level is restrictive compared with most of the period between 2009 and 2021, when rates spent years near zero. Historical comparisons tell a different story. The federal funds rate exceeded 19% during the Volcker era and remained above 5% during parts of the 1990s and mid-2000s.

Current policy therefore occupies an unusual position: restrictive enough to slow parts of the economy, but still far below levels associated with past inflation-fighting campaigns. That context helps explain why markets continue to leave room for future tightening if inflation stabilizes above target.

Four Charts, One Theme

The June meeting is unlikely to alter the policy outlook. FedWatch points to a pause. Kalshi points to lingering inflation concerns. CPI data show that price pressures remain above the Federal Reserve's objective. Historical rate data show that policymakers still have room to tighten if necessary.

Taken together, the charts suggest that the debate has shifted away from the next meeting and toward a broader question: whether inflation is heading back to 2%, or settling at a level that could eventually force the Federal Reserve to act again.

Artem Voloskovets

Artem Voloskovets