Alex Dudov

Alex Dudov

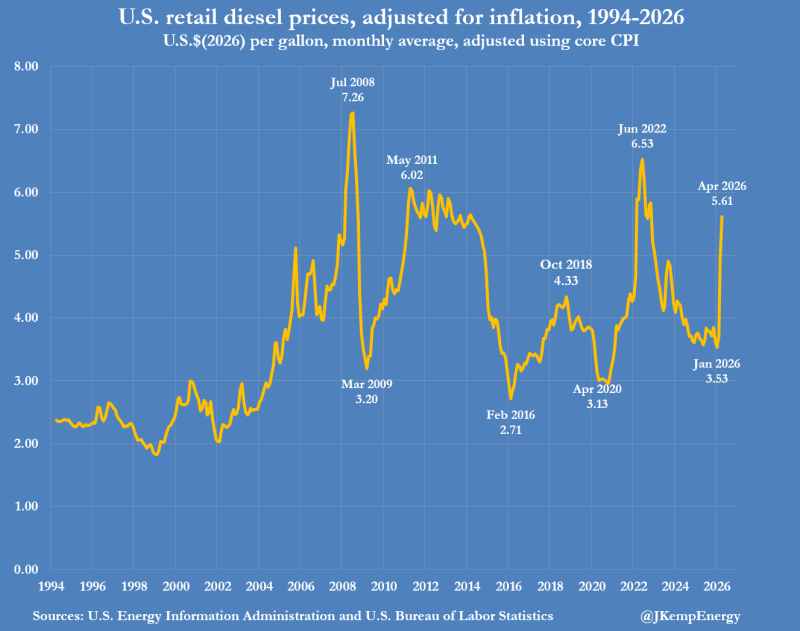

U.S. retail diesel prices are averaging $5.61 per gallon so far this month - up from $3.72 in February and $3.52 in January. John Kemp, citing source data, notes that inflation-adjusted prices have now climbed into the 87th percentile of all monthly readings since the start of the century. That number alone reframes what is happening: this is not a bounce from weakness, it is a leap into historically rare territory.

Diesel was sitting around the 38th percentile before the war began, and has since surged to the 87th percentile on an inflation-adjusted basis.

Diesel Prices: From $3.52 to $5.61 in Just Months

The chart tells a blunt story. Prices were materially lower at the start of the year, then accelerated sharply into April, creating a steep contrast with the moderate levels seen in January and February. This is not a slow-building trend. What the data shows is a decisive repricing - compressed into a very short window.

A move from the low-$3 range to above $5.50 per gallon in just a few months signals an abrupt shift in energy pricing conditions. In market terms, this looks far less like ordinary fluctuation and far more like a structural reset of the price baseline. The US Diesel Prices Jump Above $5.38 as Inflation Pressures Rise article tracked an earlier stage of exactly this dynamic.

A move from the low-$3 range to above $5.5 per gallon in just a few months signals an abrupt change in energy pricing conditions, not a slow-building advance.

Why the Diesel Percentile Shift Matters

Before the war began, diesel was sitting near the 38th percentile of inflation-adjusted readings going back to 2000. It has since jumped to the 87th percentile. That 49-point leap is the real story here - not just the dollar figure at the pump, but where this price sits in the long sweep of historical data. Most months since 2000 have been cheaper than this, by a significant margin.

Related coverage reinforces how broad the repricing has been. WTI Diesel Prices Surge as U.S. Pump Costs Jump 40% YoY tracked year-over-year pressure building across fuel markets, while US Gas Prices Jump to $3.91 as Oil Surges Above $100 showed the same dynamic playing out at the gasoline pump alongside crude above $100. This is not a diesel-only story - it is a fuel market story.

Diesel Prices Show No Sign of Normalization Yet

The chart does not show a cooling-off period. Diesel is holding at elevated levels after a forceful run higher, which means the market is still operating near the top end of its long-term historical range. The key developments driving this picture include:

- Average U.S. retail diesel at $5.61 per gallon - up nearly 60% from January

- Inflation-adjusted prices at the 87th percentile of all monthly readings since 2000

- A jump from the 38th to 87th percentile since the start of the conflict

- No normalization signal in the current chart data

Diesel is now sitting in a zone that, historically, has been associated with unusually high real-world fuel costs - and that alone makes the current pricing environment difficult to ignore.

As long as diesel holds near these levels, the broader signal is sustained pressure rather than a return to earlier-year conditions. The market is no longer operating on January or February assumptions - it has moved into a different pricing regime entirely, and the historical record makes clear just how uncommon that regime actually is.

Alex Dudov

Alex Dudov