Victoria Bazir

Victoria Bazir

Stronger economic data has pushed back expectations for Federal Reserve rate cuts, keeping Treasury yields elevated and supporting the U.S. dollar. Both factors tend to weigh on gold prices. The revision offers a useful example of how analysts evaluate gold markets beyond the metal's price action.

Step One: Watch Bond Yields Before Gold

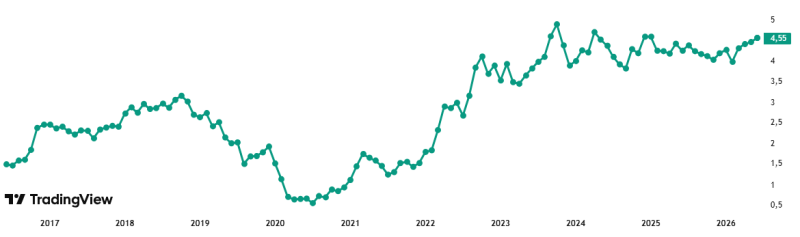

Gold is heavily influenced by developments in the bond market. The yield on the 10-year U.S. Treasury note has climbed to approximately 4.55%, remaining near the upper end of its recent range.

Figure 1. The 10-year Treasury yield has returned to 4.55%, increasing pressure on non-yielding assets such as gold.

Higher yields raise the return available on government debt. That makes gold comparatively less attractive and often supports the U.S. dollar at the same time.

This combination explains why UBS expects gold to remain under pressure in the near term despite maintaining a constructive longer-term outlook.

Step Two: Look at What Was Actually Revised

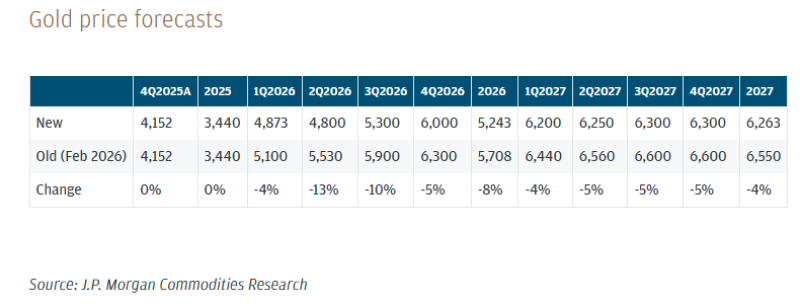

The headline number changed, but the broader view did not. UBS now expects gold to trade around $5,243 per ounce on average in 2026, down from the previous estimate of $5,708. For 2027, the forecast was reduced from $6,550 to $6,263.

The largest adjustment occurred during mid-2026. UBS cut its third-quarter 2026 forecast from $5,900 to $5,300, while the fourth-quarter target fell from $6,300 to $6,000. The bank's assumption is straightforward: higher yields and a stronger dollar are likely to slow the pace of the rally rather than end it.

Step Three: Compare Forecast Changes Across Wall Street

UBS is not the only institution revising its projections. J.P. Morgan recently lowered several gold forecasts for 2026 and 2027.

Figure 2. J.P. Morgan reduced near-term estimates but still expects gold prices to exceed $6,000 per ounce in 2027.

The revised forecast table shows a similar pattern. The bank reduced some quarterly estimates by 10–13%, yet still projects gold reaching $6,300 per ounce by the second half of 2027. The adjustment reflects timing rather than a change in direction.

Step Four: Identify the Drivers Behind the Revision

UBS highlighted three factors behind its downgrade:

- Treasury yields remain elevated;

- the U.S. dollar continues to hold firm;

- ETF and futures demand has softened.

The third point may be the most significant. According to the bank, investment flows into gold-backed ETFs and futures have stabilized but remain below levels that previously fueled strong upward momentum. Recent buying has not been sufficient to offset pressure from yields and the dollar.

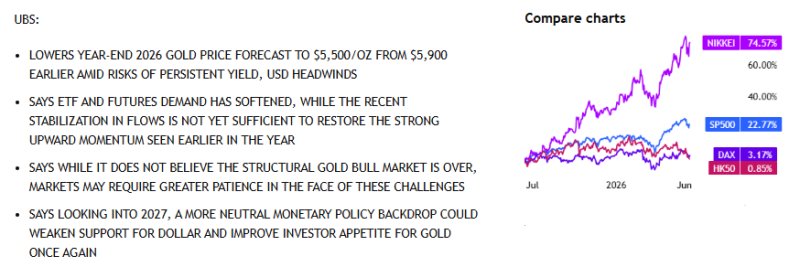

Figure 3. UBS links its forecast reduction to persistent yield pressure, dollar strength, and weaker ETF demand.

What Hasn't Changed

The bank still expects several long-term supports for gold to remain in place.

These include:

- eventual Federal Reserve rate cuts;

- weaker dollar conditions beyond 2026;

- continued central-bank purchases;

- reserve diversification trends.

UBS notes that a more neutral monetary-policy environment in 2027 could improve conditions for gold once current yield and currency headwinds begin to fade.

The Takeaway

The latest UBS revision reflects a reassessment of timing rather than a reassessment of gold itself. Higher Treasury yields, a stronger dollar and softer ETF demand have led the bank to reduce its forecasts and warn of near-term pressure on prices. At the same time, UBS continues to project gold above $6,000 per ounce during the next cycle and does not view the structural bull market as finished.

The report suggests that, for now, the key variables to watch are not gold inventories or mine supply, but bond yields, dollar strength and expectations for Federal Reserve policy.

Victoria Bazir

Victoria Bazir