Artem Voloskovets

Artem Voloskovets

The U.S. housing market is showing fresh signs of fatigue. According to the latest S&P CoreLogic Case-Shiller release, the 20-city composite index fell 0.16% month-over-month in March, a steeper decline than the 0.06% decrease economists expected. Annual price growth also came in slightly below forecasts, rising 0.83% versus expectations of 0.90%.

On the surface, the miss looks modest. Yet the data adds to a broader pattern that has emerged across the housing market over the past year: home-price appreciation is steadily losing momentum despite inventory remaining historically constrained.

For much of the post-pandemic period, limited supply helped keep prices climbing even as mortgage rates surged. That dynamic now appears to be weakening. Sellers are finding fewer buyers willing to absorb elevated valuations, while affordability remains under pressure from financing costs that are still far above pandemic-era levels. The result is a market that is no longer overheating, but is not meaningfully correcting either.

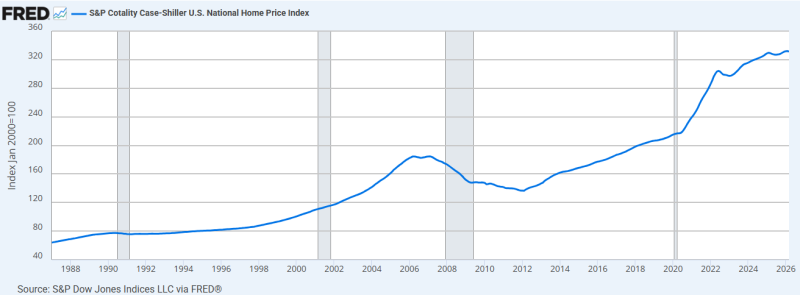

The Pandemic Price Shock Still Defines the Market

The latest slowdown is unfolding against the backdrop of one of the most dramatic housing rallies in modern U.S. history. The national Case-Shiller index climbed from roughly 215 points at the start of 2020 to more than 320 today, meaning U.S. home values remain around 50% higher than before the pandemic. Even the sharp rise in interest rates since 2022 has done little to erase those gains.

That legacy continues to shape market behavior. Prices may no longer be accelerating, but they remain elevated enough to keep many potential buyers on the sidelines. In other words, the challenge facing the housing market is not a collapse in prices - it is the persistence of prices that never truly came back down.

This helps explain why annual growth has slowed to less than 1% while affordability concerns remain widespread.

A Market Caught Between Supply Constraints and Demand Fatigue

The current housing cycle differs sharply from previous downturns. Inventory remains relatively tight because millions of homeowners continue to hold mortgages originated during the low-rate environment of 2020 and 2021. Selling a home often means replacing a 3% mortgage with financing that costs more than twice as much, creating a powerful incentive to stay put.

At the same time, elevated borrowing costs have eroded purchasing power. Many buyers who could comfortably qualify for a home a few years ago face substantially higher monthly payments today, even if asking prices stabilize. That combination has created a market stuck in equilibrium: supply is too limited for a major price correction, yet affordability is too stretched to support another broad-based surge in valuations.

What It Means for Investors

Housing remains one of the sectors most sensitive to interest-rate policy, making the latest Case-Shiller figures relevant beyond the real-estate market itself. Cooling home-price growth reinforces evidence that higher borrowing costs continue to restrain economic activity. While a single monthly report is unlikely to alter Federal Reserve expectations, persistent weakness in housing could strengthen the argument that restrictive monetary policy is gradually filtering through to the broader economy.

Artem Voloskovets

Artem Voloskovets