Saad Ullah

Saad Ullah

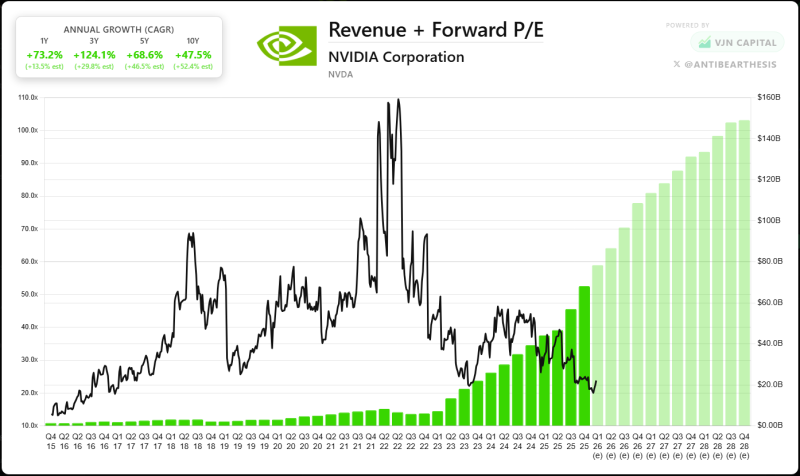

NVIDIA is drawing fresh attention because the chart shows two forces moving in opposite directions: revenue keeps climbing while the forward P/E has compressed sharply from prior extremes. As Noah argued, that combination supports the view that NVDA remains a long-term bullish holding, with projected revenue continuing to rise through 2026, 2027, and 2028.

NVDA Growth Moving Higher While the Multiple Stays Contained

The image shows NVIDIA's revenue bars rising steadily and then accelerating sharply from 2023 onward, with estimates extending that climb well into future periods. At the same time, the forward P/E line has fallen far below the triple-digit peaks seen in earlier years and is now sitting in a much lower range near the right edge of the chart.

That is the core tension in the setup: fundamentals are expanding while valuation has become materially less stretched than in past hype phases. In earlier cycles, NVIDIA often traded with a much richer earnings multiple when enthusiasm around growth was strongest. Now the market is assigning a far more restrained valuation than it did during previous spikes - even as the revenue path remains steep.

NVDA Price Climbs While P/E Drops to 48x documented this multiple compression as it was developing, showing how the earnings growth rate has been outpacing price appreciation in a way that makes the current forward P/E level structurally different from the inflated multiples that defined earlier NVDA enthusiasm cycles.

The NVDA Bull Case Is Strong, but Not Frictionless

The tweet adds an important caveat: a large share of NVIDIA's sales comes from a small number of clients. That concern does not contradict the chart, but it frames the risk around the current growth story. If spending from those major buyers stays strong, the revenue ramp remains credible. If that concentration starts to weaken, the market could reassess confidence in the trajectory quickly.

NVDA Stock: 3 Major Investors Exit as AI Bubble Concerns Grow captures the skeptical side of the debate, showing why the concentration risk and bubble concerns have been translating into actual positioning changes - even as the fundamental data in the chart continues to support the bull case.

Where the NVDA Valuation Debate Gets More Interesting

What makes this setup compelling is that it is not just a story about optimism - it is a story about compression. The chart does not show valuation excess expanding alongside revenue. It shows the opposite. That is why the AI bubble argument looks less straightforward when placed next to the actual data.

If NVIDIA keeps delivering on the revenue path implied by the chart, the current forward multiple may look conservative in hindsight. If growth slows abruptly because of customer concentration, that lower multiple may prove justified.

Nvidia Leases $3.8B Data Center in Nevada as AI Infrastructure Demand Surges shows the infrastructure commitment that supports the revenue ramp - with $3.8 billion in data center capacity reflecting the kind of capital allocation that makes the forward revenue estimates on the chart structurally grounded rather than purely speculative.

Saad Ullah

Saad Ullah