Eseandre Mordi

Eseandre Mordi

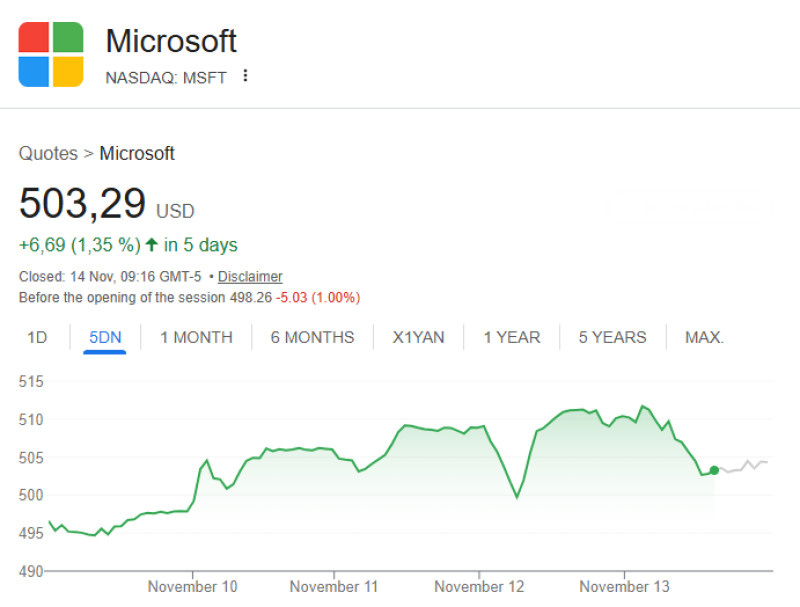

⬤ Baird has started covering Microsoft with an Outperform rating and $600 price target, emphasizing the company's extensive AI and cloud presence and potential for sustained double-digit growth. Analyst William Power says Microsoft is leading the AI revolution through its integrated infrastructure, application ecosystem, and OpenAI partnership—creating a comprehensive and defensible platform. Microsoft's first-quarter FY26 revenue jumped 18% to $77.7 billion, powered by Azure and Intelligent Cloud, and Baird believes the stock remains attractive despite its earlier rally this year. Azure's 40% year-over-year growth drives Microsoft's momentum, while total cloud revenue—now nearly 60% of overall business—rose 25% in constant currency. Copilot adoption surpassed 150 million monthly active users, and core software products like Microsoft 365, LinkedIn, and Dynamics grew 17%. Power highlighted Microsoft's financial strength with a 49% operating margin and 33% free-cash-flow margin as major competitive advantages.

⬤ As Microsoft accelerates its AI and cloud dominance, policymakers are debating tax changes that could affect multinational tech companies. Proposals for higher digital-services taxation and stricter AI revenue reporting might increase operational burdens across Microsoft's supply chain, potentially straining smaller partners. Higher taxes on specialized technical labor could also intensify talent competition, making it harder for Microsoft to keep the AI engineers and researchers critical to maintaining its edge.

⬤ With global AI demand growing rapidly, Microsoft's cloud scale, platform integration, and strong margins position it as one of the best long-term AI beneficiaries. While potential tax reforms present risks, Baird sees the company's strategic depth and financial resilience as a compelling opportunity for investors targeting the next wave of AI-driven cloud growth.

Eseandre Mordi

Eseandre Mordi