Victoria Bazir

Victoria Bazir

The announcement is less about shareholder liquidity and more about capital allocation. A private credit lender is choosing to buy back its own equity rather than deploy all available capital into new loans.

Growth Is No Longer the Story

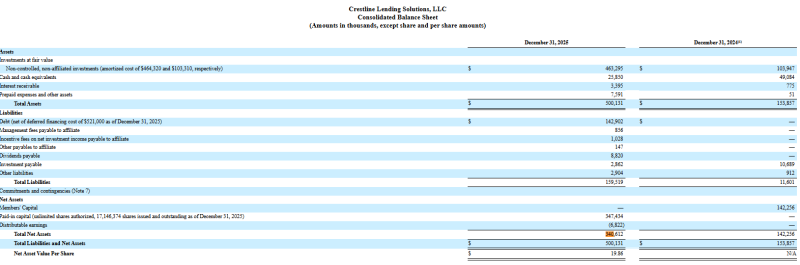

Private credit has spent years benefiting from bank retrenchment, higher interest rates, and strong investor demand for yield. Crestline's own balance sheet reflects that trend. Net assets increased from $142.3 million at the end of 2024 to $340.6 million by the end of 2025, while total assets reached $500.1 million.

The company is growing rapidly. The tender offer is not being launched from a position of weakness, but from one of expansion.

A Capital Allocation Decision

Every lender faces the same choice: deploy capital into new loans or return it to shareholders. By launching a repurchase program, Crestline is effectively saying that buying its own shares offers an attractive use of capital.

At a reported NAV per share of $19.86, the company could retire roughly 858,000 shares if the offer is fully subscribed. The financial impact is modest. The signal is not.

A More Competitive Market

Private credit remains one of the fastest-growing areas of finance, but competition is increasing. More managers are chasing the same borrowers, making disciplined capital deployment increasingly important. In that environment, repurchasing shares can generate better risk-adjusted returns than expanding a portfolio at lower spreads. The decision does not suggest a lack of opportunities. It suggests greater selectivity.

What It Means

Crestline now operates with more than $500 million in assets and belongs to a platform managing approximately $19.9 billion, including $7.9 billion in alternative credit strategies. The tender offer therefore looks less like a liquidity program and more like evidence of a maturing industry where capital efficiency matters as much as asset growth.

Victoria Bazir

Victoria Bazir