Saad Ullah

Saad Ullah

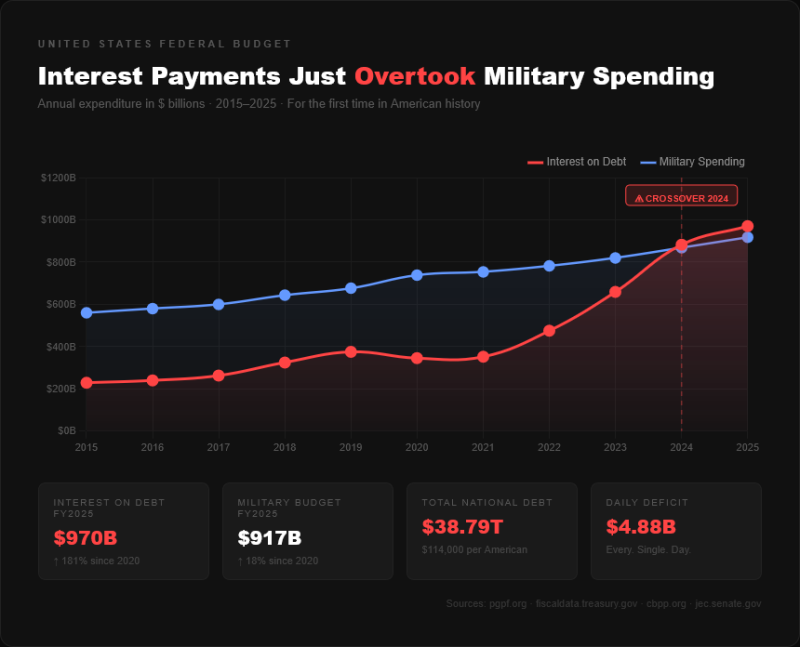

For decades, defense spending sat at the top of America's discretionary budget, a symbol of national priorities and global commitments. That era is over. In 2025, the cost of simply paying interest on what the US government owes has quietly overtaken what it spends on its military, a crossover that would have seemed unthinkable just a generation ago. It is not the result of dramatic policy change or a sudden crisis, but the slow, compounding consequence of years of deficit spending and rising borrowing costs finally showing up in the ledger.

$970 Billion: How Interest Payments Topped the Military Budget

For the first time in American history, federal interest payments on outstanding debt have overtaken defense spending, marking a genuine fiscal milestone. Budget projections put interest costs at $970 billion in 2025, against $917 billion allocated to the military. The crossover became visible around 2024, with interest payments climbing steadily past defense outlays on the budget chart. Total national debt now sits near $38.79 trillion, and the bill for carrying that debt keeps growing.

The rise in interest costs is driven by two forces working together: the sheer size of accumulated debt and higher average borrowing rates. As the Federal Reserve tightened monetary policy, yields on Treasury securities moved sharply higher, making each new dollar borrowed more expensive to service. Obligations have surged from manageable levels a decade ago to nearly $39 trillion today, and the combination of volume and rate has pushed annual interest expenses well past what most budget forecasters anticipated just a few years back.

The broader picture is one of persistent structural deficits. The government consistently spends more than it collects, adding to the cumulative debt pile year after year. Global debt has now hit $111 trillion, and the US sits at the center of that story. Changes in foreign Treasury holdings and shifting global demand for sovereign debt are adding another layer of complexity to an already stretched fiscal position.

Rising debt service costs highlight the growing share of fiscal resources devoted to simply maintaining current obligations rather than funding new initiatives.

The implications reach beyond accounting. As a growing share of the federal budget flows toward debt service rather than investment, defense, or social programs, it quietly reshapes what the government can and cannot afford to do. Japan offers a cautionary comparison, with debt at 230% of GDP and decades of experience managing the political and economic strain that comes with it. Whether the US can navigate a similar path, or find a way to alter the trajectory, is shaping up to be one of the defining fiscal questions of the decade ahead.

Saad Ullah

Saad Ullah