Eseandre Mordi

Eseandre Mordi

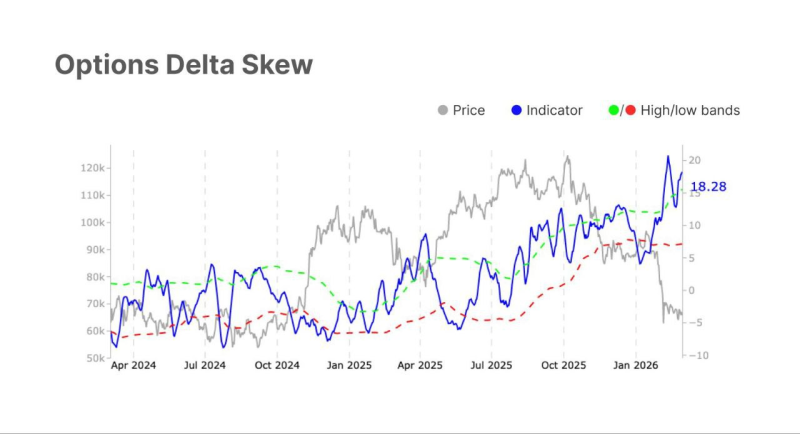

When a key options metric quietly slips above its historical ceiling, it tends to mean something. Right now, the 25-delta skew is doing exactly that, and traders are taking notice. The move above the upper band signals a measurable shift in how the market is pricing risk, one that goes well beyond routine fluctuations in volatility.

25-Delta Skew Climbs to 18.3%, Breaching the 15.6% Upper Band

Options market metrics have shown a notable shift as the 25-delta skew climbed to approximately 18.3%, surpassing its normal upper threshold near 15.6%. This move suggests that out-of-the-money put prices are rising relative to calls, pointing toward higher costs for downside protection. The chart indicator in blue climbing above the green and red bands makes the shift hard to miss, underlining a clear departure from typical pricing patterns seen throughout most of the past year.

Elevated skew suggests that a segment of traders is prioritising downside protection, affecting implied volatilities and option premiums across the derivatives market.

The primary interpretation of this skew expansion is straightforward: traders are paying up for insurance against potential market declines. In options markets, the delta skew reflects the relative pricing of downside versus upside optionality. When skew rises, put options become relatively more expensive, which aligns with a heightened focus on hedging. The current reading sitting well above its historical average band marks a meaningful break from the norm.

What Rising Options Skew Tells Us About Market Sentiment

The rising skew can also be read as a return of the hedge bid, as market participants seek cover amid uncertain equity price behavior. While SPX realized volatility has only recently compressed, the skew expansion tells a different story about forward-looking risk appetite. Elevated skew levels do not point to a specific direction for equities, but they do suggest that a meaningful portion of the market is positioned defensively, driving up premiums on protective puts.

The implications stretch beyond individual option contracts. Rising skew affects implied volatility surfaces, risk management frameworks, and derivatives pricing across asset classes. As seen with recent positioning such as the $19M put bet on QQQ and bullish options setups in META, the options market is actively repricing risk on multiple fronts. Tracking these structural shifts offers a clearer read on how institutional and retail participants alike are preparing for potential volatility ahead.

Eseandre Mordi

Eseandre Mordi