Saad Ullah

Saad Ullah

The latest PCE data confirms that inflation is not falling as expected, reinforcing a persistent trend that has kept policymakers on edge for months.

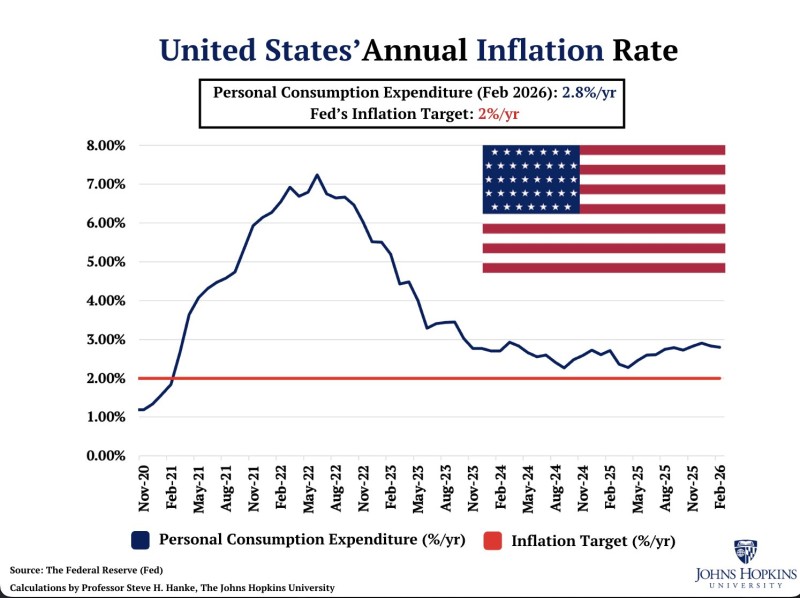

The numbers leave little room for optimism. As Steve Hanke pointed out, the Personal Consumption Expenditures index held steady at 2.8% year-over-year in February - above both the Fed's 2% target and the 2.6% forecast. That gap may look small on paper, but in policy terms it carries real weight, keeping the Federal Reserve in a difficult position as it tries to justify any near-term rate cuts.

PCE Inflation Pattern: From Peak to Plateau

The data tells a story in three chapters. First, a sharp surge through 2021 and 2022 as pandemic-era stimulus flooded the economy. Then a steady decline into 2023 that gave markets hope. And finally, a slowdown in that downward move that has now turned into something closer to a stall.

Inflation rose sharply, then fell - but now it has settled into a narrow band with no clear direction lower.

Rather than continuing its descent, PCE inflation stabilized in a range between roughly 2.3% and 3.0%. The 2% level - the Fed's official target - has not been reclaimed. Instead of acting as a ceiling to push through on the way down, it functions more like a floor that inflation keeps bouncing off. Fed rate cut odds jumped to 87% after the latest PCE release, a reaction that reflects just how much tension exists between market expectations and the actual data.

SPY and Markets React to a Range That Refuses to Break

Structurally, the chart no longer reflects a clean downtrend. The pattern of lower highs and lower lows that defined 2022 and most of 2023 has faded. What replaced it is sideways movement - inflation that repeatedly approaches the 2% level but fails to move below it, while also failing to break above 3%.

This is consolidation, not disinflation. And consolidation at 2.8% is not what the Fed had in mind when it began tightening. U.S. inflation has held above 2.5% even as the Fed stays cautious on rate cuts, and the February PCE reading does nothing to change that picture.

Price pressures are no longer easing in a straight line - the data has shifted from a clear downtrend into a flat, rangebound structure.

The SPY ETF, which tracks the S&P 500, remains sensitive to every inflation print precisely because the rate outlook drives equity valuations at this stage of the cycle. When inflation refuses to fall, rate cuts get pushed out, and stretched multiples come under pressure.

PCE at 2.8%: The 2% Target That Has Not Been Reclaimed

The most important takeaway from the February data is not where inflation is - it is where inflation is not. It is not at 2%. Despite the sharp decline from the 2022 peak near 7%, the PCE index has spent more than a year unable to close that final gap.

The inability to break below 2% is the defining feature of the current inflation structure - and it is what keeps the Fed from declaring victory.

That persistent gap matters for SPY and for the broader market. As long as PCE holds above target, the Fed has no clean reason to cut rates aggressively. Inflation continues to hold above the Fed target as both CPI and PCE flatten, and the February reading at 2.8% fits squarely within that pattern.

The data reflects stability above target rather than continued progress toward it - and for equity markets still pricing in rate relief, that distinction is everything.

Saad Ullah

Saad Ullah