Marina Lyubimova

Marina Lyubimova

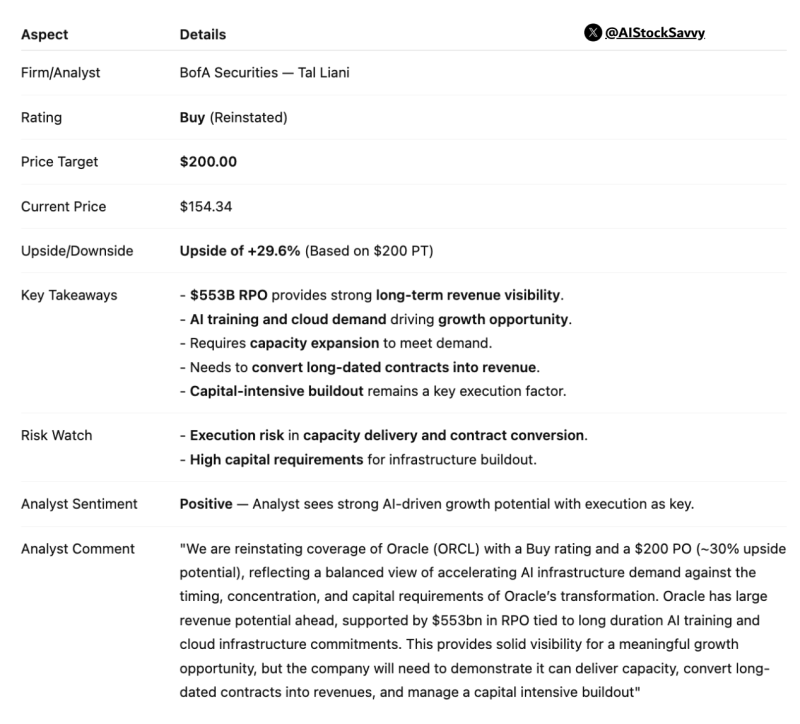

Oracle (ORCL) is back in the spotlight after Bank of America reinstated a Buy rating with a $200 price target, signaling renewed confidence in the company's long-term trajectory. With shares trading near $154, that target implies roughly 30% upside, driven by what analysts see as a structural shift in enterprise technology toward AI infrastructure. Oracle's expanding cloud pipeline and multi-year contracts put it at the center of that shift.

$553 Billion Backlog Gives Oracle Rare Revenue Visibility

The core of the bullish thesis is Oracle's reported $553 billion in remaining performance obligations, a figure that reflects multi-year commitments across AI training and cloud infrastructure. That kind of backlog is rare in enterprise tech and gives Oracle a degree of forward revenue visibility that most peers can't match. Analysts see it as evidence that Oracle is being selected as a core infrastructure provider in the AI buildout, not just a legacy database company.

AI Workloads Drive Growth, But Execution Remains the Key Risk

Beyond the backlog, AI training workloads and cloud demand are cited as the primary growth catalysts for ORCL going forward. The upgrade highlights that Oracle must now scale capacity and convert those long-term contracts into realized revenue, a capital-intensive process that carries execution risk. Infrastructure buildout requires sustained investment, and converting pipeline into cash flow will define how the market values Oracle over the next few years.

The reinstated Buy rating reflects a broader re-rating of traditional enterprise tech companies in the context of AI infrastructure spending. As AI infrastructure demand continues to accelerate, Oracle's ability to deliver on its backlog, expand capacity, and manage capital allocation will determine whether the $200 target holds. The fundamentals support the case, but execution will be the deciding factor.

Marina Lyubimova

Marina Lyubimova