Peter Smith

Peter Smith

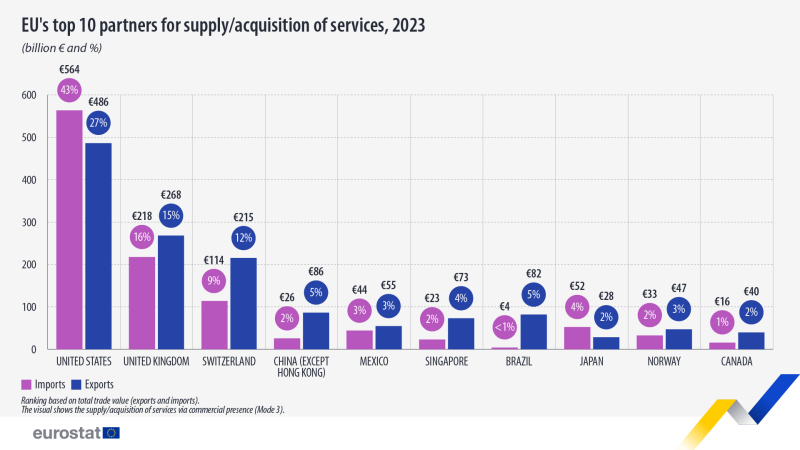

The European Union's services trade structure is far more concentrated than it may appear at first glance. New data from EU_Eurostat shows that a handful of partners - led by the United States - account for a dominant share of both imports and exports, reinforcing how tightly clustered the EU's global services relationships have become.

The Weight of a Single EU Services Trade Dominant Partner

Commercial presence accounted for 77.5% of the EU's services trade surplus in 2023. Within that framework, the United States stands clearly above all others:

- €564 billion in imports linked to the U.S. (43%)

- €486 billion in exports (27%)

This gap between import and export shares highlights an asymmetric but deeply integrated relationship. The U.S. is not just a partner - it is the central hub around which EU services trade is structured, with an import share that is nearly double the export share.

A Secondary Tier With More Balanced EU Services Exposure

Beyond the U.S., the United Kingdom and Switzerland form a second layer of importance. Unlike the U.S., their shares appear more balanced between imports and exports - suggesting more symmetrical trade relationships rather than directional dependence:

- UK: €218 billion in imports (16%) and €268 billion in exports (15%)

- Switzerland: €114 billion in imports (9%) and €215 billion in exports (12%)

This balance contrasts sharply with the U.S. dynamic and indicates tighter two-way integration. Switzerland in particular shows a notable export surplus relative to its import share - a pattern that reflects the financial and pharmaceutical services concentrated in the bilateral relationship.

The Sharp Drop Beyond the EU's Core Services Network

The chart also reveals a steep decline in relevance beyond the top three partners. Countries such as China, Mexico, Singapore, and Brazil appear in the dataset, but their shares fall quickly into low single digits. This creates a clear structural pattern with no gradual transitions between tiers - just a sharp drop-off in scale:

- A dominant top tier centered on the U.S.

- A balanced secondary layer with the UK and Switzerland

- A fragmented tail of smaller partners with limited influence

There are no gradual transitions between tiers - just a sharp drop-off in scale that makes the concentrated nature of EU services trade impossible to overlook.

EU Retail Trade Dips 0.2% in February but Volumes Hold Near Multi-Year Highs places this services trade concentration within the broader context of EU economic activity, showing how the same structural patterns visible in trade data are also reflected in domestic consumption trends. Eurostat Names Winners of Global Nowcasting Challenge adds a methodological dimension, highlighting how Eurostat is increasingly using advanced analytical frameworks to interpret the kind of concentrated data structures visible in the services trade dataset.

The implication is straightforward: the EU's services trade surplus and structure depend heavily on a small number of deeply embedded relationships. That concentration may provide stability - but it also means shifts within these key partnerships carry outsized consequences for the broader system.

Peter Smith

Peter Smith