Marina Lyubimova

Marina Lyubimova

The latest move matters because it points to firmer shipping costs even as key trade lanes stop moving in lockstep. As Ole S Hansen noted, the latest advance was moderate rather than explosive - but it still pushed the benchmark to a three-month high.

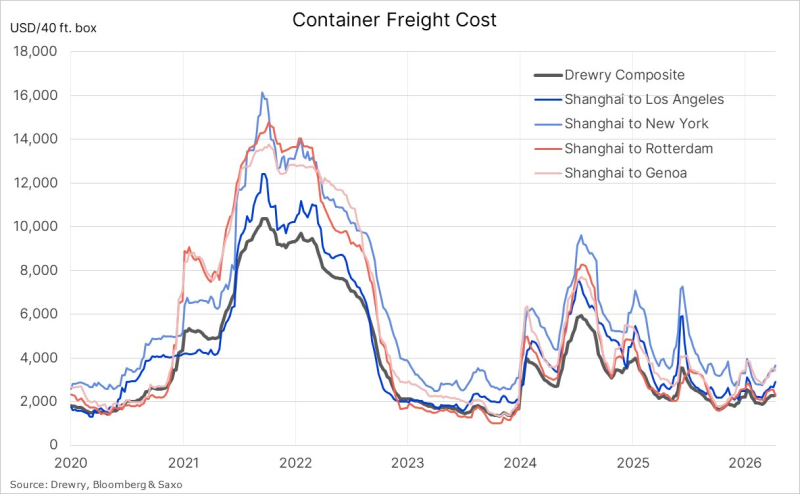

A Container Freight Recovery That Looks Steady, Not Disorderly

The chart shows just how far the freight market has traveled since the extreme peaks of 2021 and 2022, when several major routes surged well above $10,000 per container. By comparison, the current move is far more restrained. The Drewry Composite sitting near $2,309 is still a fraction of the pandemic-era spike - but strong enough to mark a clear rebound from the softer pricing environment seen through 2023 and parts of 2024.

That distinction matters. This is not a replay of the supply-chain panic phase. It is a slower rebuilding process, where rates are firming without breaking into a broad vertical surge.

Shipping Prices Are Going Absolutely Crazy: Shanghai to New York Just Hit $8,000 captured what the panic phase looked like at its peak - providing a useful baseline for how different the current firming environment feels by comparison.

US Container Routes Are Pulling Away From Europe

The most important shift in the latest update is divergence. Rates from Shanghai to New York and Los Angeles continued to rise, while rates to Europe declined - creating a split across major shipping corridors that is visible in the chart, where US-bound lines remain firmer while Europe-bound routes soften.

Instead of one unified global move, the market is starting to trade on route-specific pressure. That gives the latest rise in the composite index a more nuanced tone: shipping costs are increasing overall, but the strength is not evenly distributed.

The market is starting to trade on route-specific pressure rather than one unified global move - US-bound strength is lifting the composite while European routes soften.

China-US Cargo Volumes Collapse adds important context to the US route dynamics, showing how volume shifts between the two largest trading partners are reshaping which corridors see pricing pressure and which remain soft.

The Container Freight Market Is Higher, but Still Selective

The tweet's numbers frame the current move precisely. The index is up 4% year to date and 2% over the past twelve months - pointing to gradual improvement rather than a breakout phase. After repeated spikes and pullbacks across routes in 2024 and 2025, rates are lifting again but from a much lower base than the historic highs.

FAO Food Price Index Climbs to 128.5 as Global Uptrend Resumes places the freight rate recovery within a broader commodity and logistics pricing context, showing how firming shipping costs fit into a wider pattern of input price increases currently working through global supply chains.

Marina Lyubimova

Marina Lyubimova