Artem Voloskovets

Artem Voloskovets

- Signal #1: Funding Has Returned to Pre-Bull-Market Levels

- Signal #2: Most Deals Are No Longer Seed-Stage Bets

- Signal #3: Infrastructure and CeFi Are Absorbing Most Capital

- Signal #4: Funding Remains Concentrated in Financial Centers

- Signal #5: The Same Funds Continue to Shape the Market

- Signal #6: The Largest Checks Are Going to Mature Companies

- What the Data Suggests

Funding volumes can increase during speculative periods and still fail to produce sustainable businesses. To understand where the industry is heading, it helps to look at how capital is distributed, which sectors receive funding, and what types of companies attract investor attention. Recent CryptoRank data highlights six indicators that reveal more than headline funding numbers.

Signal #1: Funding Has Returned to Pre-Bull-Market Levels

Crypto startups raised approximately $8 billion in Q3 2025, compared with $689 million in Q3 2023.

The recovery began in 2024, when quarterly funding stabilized around $2–2.5 billion, before accelerating sharply in 2025. The significance is not the growth rate itself. It is the fact that venture funding has continued to rise across multiple quarters rather than spiking around a single narrative or market event.

Signal #2: Most Deals Are No Longer Seed-Stage Bets

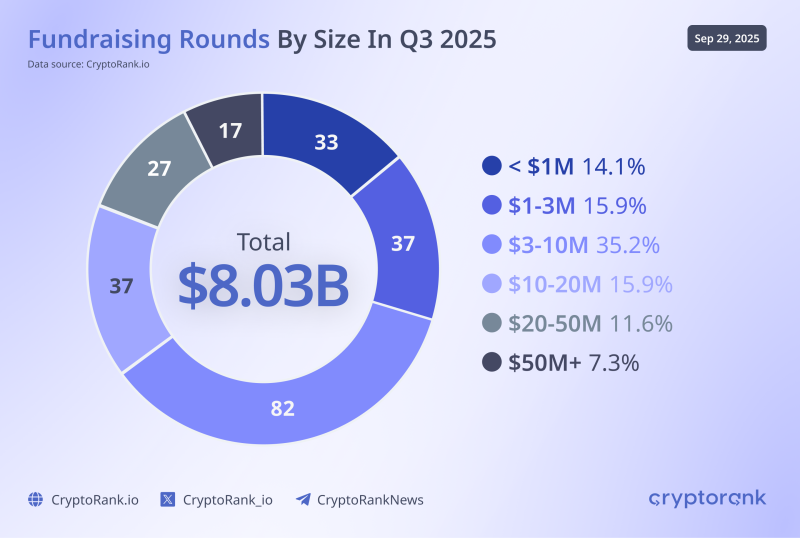

The most common funding range in Q3 2025 was $3 million to $10 million, accounting for 35.2% of all rounds.

The distribution looked as follows:

- Under $1 million — 14.1%

- $1–3 million — 15.9%

- $3–10 million — 35.2%

- $10–20 million — 15.9%

- $20–50 million — 11.6%

- Over $50 million — 7.3%

Most activity is concentrated in companies that have already moved beyond the idea stage. Investors are committing capital to businesses with products, users, and operating history rather than funding large numbers of early experiments.

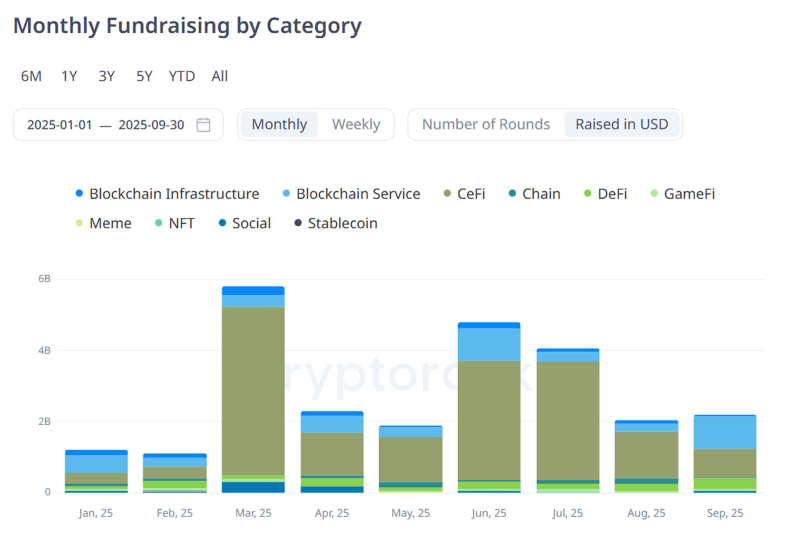

Signal #3: Infrastructure and CeFi Are Absorbing Most Capital

Category data shows that CeFi attracted the largest share of funding during most months of 2025. March generated nearly $6 billion in total fundraising, while June and July both exceeded $4 billion.

The largest funding flows went to:

- CeFi platforms;

- blockchain infrastructure;

- blockchain services;

- stablecoin-related businesses.

NFT, GameFi, and meme-related projects represented only a small share of total capital. The pattern suggests that investors currently prioritize services and infrastructure over consumer-facing speculation.

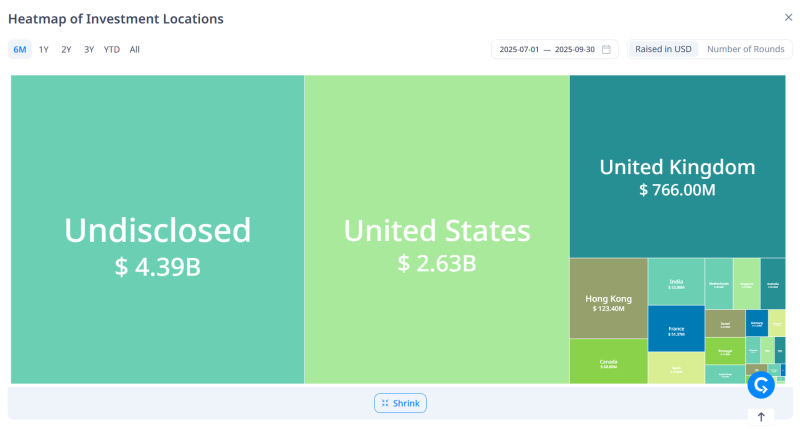

Signal #4: Funding Remains Concentrated in Financial Centers

Among disclosed investments in Q3 2025:

- United States — $2.63 billion

- United Kingdom — $766 million

- Hong Kong — $123 million

Another $4.39 billion was recorded as undisclosed. The geographic distribution remains similar to previous years. Most venture funding continues to flow through established financial hubs where institutional capital, legal infrastructure, and experienced operators are concentrated.

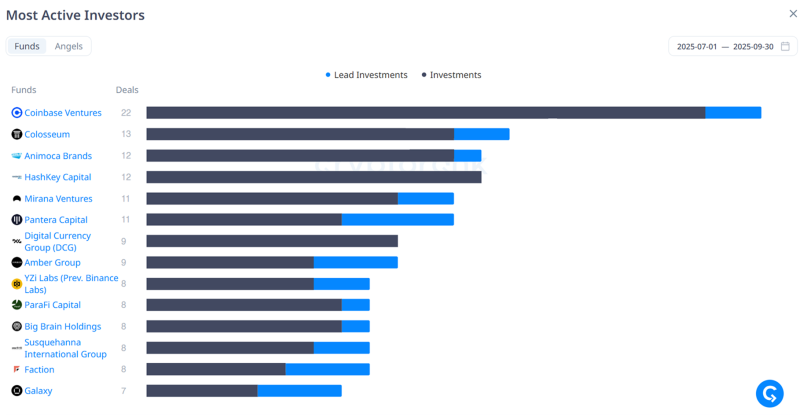

Signal #5: The Same Funds Continue to Shape the Market

The most active investors during the quarter were:

- Coinbase Ventures — 22 deals

- Colosseum — 13 deals

- Animoca Brands — 12 deals

- HashKey Capital — 12 deals

- Mirana Ventures — 11 deals

- Pantera Capital — 11 deals

These firms participated across multiple sectors and stages, giving them visibility into broader market trends. Their activity shows that capital deployment is not limited to a handful of large transactions. Established venture firms remain actively involved in sourcing and funding new companies.

Signal #6: The Largest Checks Are Going to Mature Companies

Late-stage fundraising has expanded rapidly:

- 2023 — $1.66 billion

- 2024 — $2.42 billion

- 2025 — $8.21 billion

- 2026 YTD — $6.47 billion

The number of late-stage rounds increased from 160 in 2023 to 307 in 2025, while total capital grew at a much faster pace.

That means average deal sizes are increasing. Investors are concentrating larger amounts of capital in companies that already have revenue, customers, and operational scale.

What the Data Suggests

The current funding cycle differs from the one that defined the 2021 bull market. Capital is concentrated in infrastructure, financial services, and later-stage businesses. Mid-sized growth rounds dominate deal activity, while large late-stage financings account for an increasing share of total capital raised.

Taken together, the data points to an industry that is attracting funding for execution and scale rather than for narratives alone.

Artem Voloskovets

Artem Voloskovets