Eseandre Mordi

Eseandre Mordi

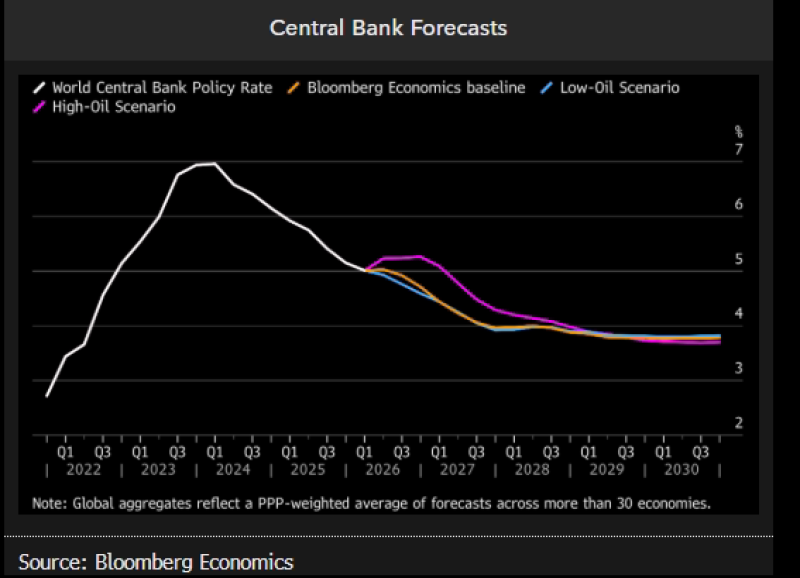

An oil spike may hit sentiment immediately, but the broader inflation story is more conditional than it first appears. As Daniel Lacalle argues, oil shocks and wars are disinflationary unless governments respond with more spending and money creation. The chart supports that tension: even across high-oil, low-oil, and baseline scenarios, global central bank policy rates are still projected to drift lower after peaking.

The Rate Path Markets Still Expect After an Oil Shock

The chart shows a sharp rise in global central bank policy rates from 2022 into 2023, followed by a steady decline through the years ahead. What stands out is not just the peak, but the shape of the descent. Even when oil assumptions change, the projected policy path still bends lower rather than reaccelerating higher.

The high-oil scenario does keep rates above the baseline for a period - suggesting energy pressure can delay easing. But the gap does not spiral wider over time. Instead, the lines gradually converge, implying that an oil shock alone is not seen as enough to create a lasting inflation regime.

Brent Oil Outlook: Goldman Sees $115 as Inflation Risk Surges in 2026 captures the market's near-term concern about oil-driven inflation - but the rate path chart suggests that even at those price levels, the long-term policy trajectory still points toward easing rather than a sustained tightening cycle.

When Energy Crowds Out Everything Else

That is where Lacalle's point becomes more relevant. If households and businesses are forced to allocate more money to fuel and energy, less money is available for other goods and services. In that setup, money velocity weakens rather than broadens across the economy.

The chart's long glide lower in policy forecasts fits that interpretation. A pure inflationary shock would normally imply a more stubborn rate path - instead, Bloomberg Economics' scenarios still point to eventual easing, even if the high-oil case temporarily slows the process.

WTI Oil: A $20 Price Shock Could Push U.S. Inflation Up 0.65% quantifies the direct inflation impact of an oil move - and the relatively modest 0.65% figure reinforces Lacalle's point that the shock itself is not the primary inflation risk. The policy response is.

The Policy Response Is the Real Oil Inflation Pressure Point

Oil becomes broadly inflationary only when policymakers try to offset the economic drag with more fiscal spending or monetary expansion. Without that response, the shock acts more like a tax on demand than a durable engine of economy-wide price acceleration:

- Global policy rates peak first, then trend lower across all scenarios

- The high-oil path stays above baseline temporarily but does not break away permanently

- The long-term forecasts still converge toward lower rates

- The inflation impact depends less on oil itself than on the policy reaction that follows

Fed Rate Cut Odds Hit 0% for 2026 as Inflation and Oil Keep Policy on Hold shows the near-term market pricing that sits alongside this longer-term rate path - reinforcing that while the short-term policy response to oil has been hawkish, the structural trajectory the chart projects still points toward eventual easing once the energy pressure subsides.

Eseandre Mordi

Eseandre Mordi