Peter Smith

Peter Smith

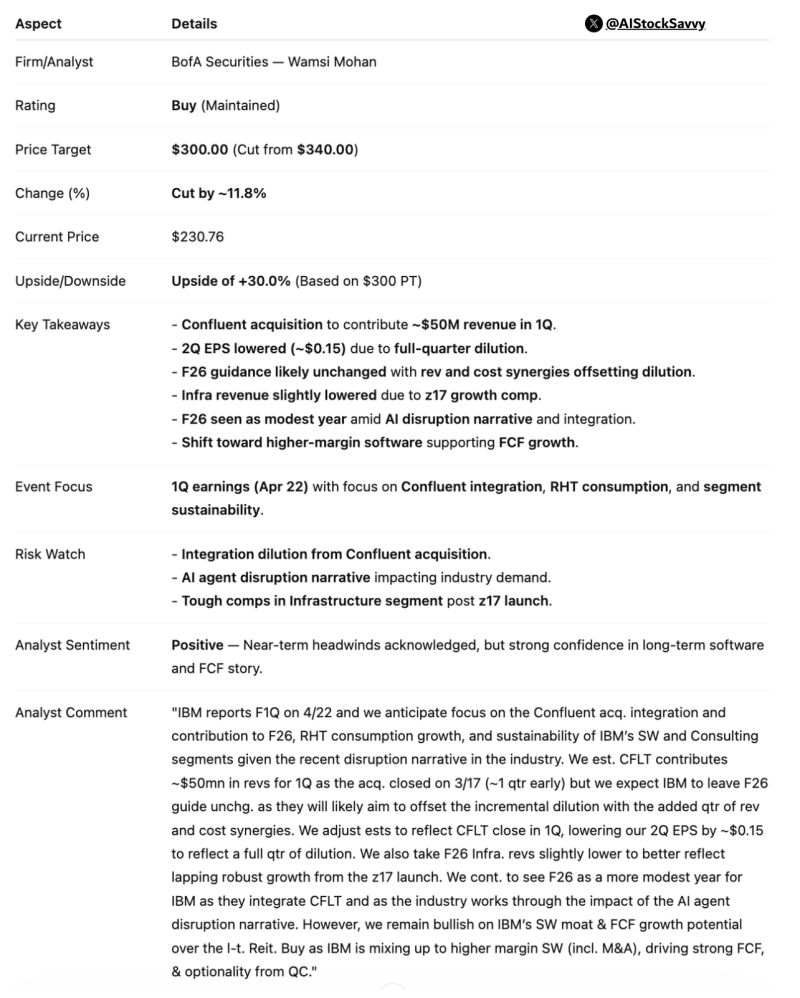

IBM remains in focus after Bank of America maintained its Buy rating while lowering its price target to $300 from $340. The move signals that short-term pressure has not changed the firm's broader bullish stance on the stock, which is currently trading around $230.76 - leaving meaningful upside to the revised target even after the cut.

As Hardik Shah noted in his analysis, the message is not that the IBM thesis is broken. Expectations are being reset to reflect a more complicated near-term setup, not a change in direction.

The IBM thesis is not broken - expectations are being reset to reflect a more complicated near-term setup, not a change in direction.

The revised view frames IBM as a stock caught between short-term earnings dilution and a longer-term strategic pivot toward higher-margin software and improving free cash flow.

Confluent Acquisition Creates Near-Term IBM Earnings Pressure

The main friction point in BofA's note is the Confluent acquisition and its integration effects. The deal is expected to add roughly $50 million in first-quarter revenue, but the firm also lowered second-quarter EPS by around $0.15 due to full-quarter dilution.

That trade-off defines the current IBM setup. Revenue contribution is real, but so is the earnings hit - and that leaves investors balancing strategic expansion against the cost of absorbing it. It makes the near-term picture messier without changing the underlying logic of the deal.

Revenue contribution is expected, but so is earnings pressure, and investors are left balancing strategic expansion against the cost of absorbing it.

For more on how IBM is positioning itself in the AI space, see IBM Stock News: Shares Surge on Anthropic AI Partnership.

Why IBM's Long-Term Software Strategy Remains Intact

What keeps the tone constructive is that IBM's broader direction has not changed. Fiscal 2026 guidance is likely to remain unchanged, with revenue and cost synergies expected to offset dilution over time. BofA continues to point to a sustained shift toward higher-margin software as the key driver supporting the free cash flow story that underpins the bullish case.

The note does acknowledge that fiscal 2026 may be a more modest year as IBM works through integration and faces industry disruption narratives. That makes this less a story of immediate acceleration and more one of defending the long-term framework while short-term estimates are adjusted.

Fiscal 2026 may be a more modest year, but the shift toward higher-margin software and improving free cash flow keeps the long-term framework intact.

Near-term headwinds are clearly being recognized - integration dilution and softer infrastructure expectations among them - yet the underlying view remains that IBM's software positioning and cash generation potential still justify a constructive stance. The $300 target, even after the reduction, still implies significant upside from current levels.

IBM Looks Like a Reset Story, Not a Reversal

IBM right now is a stock moving through an adjustment phase, not a retreat. The focus has shifted from the headline target reduction to whether the company can prove that integration pressure is temporary and the higher-margin strategy stays on track.

That is the question BofA is asking investors to sit with - and for now, their answer is still a Buy.

Peter Smith

Peter Smith