Artem Voloskovets

Artem Voloskovets

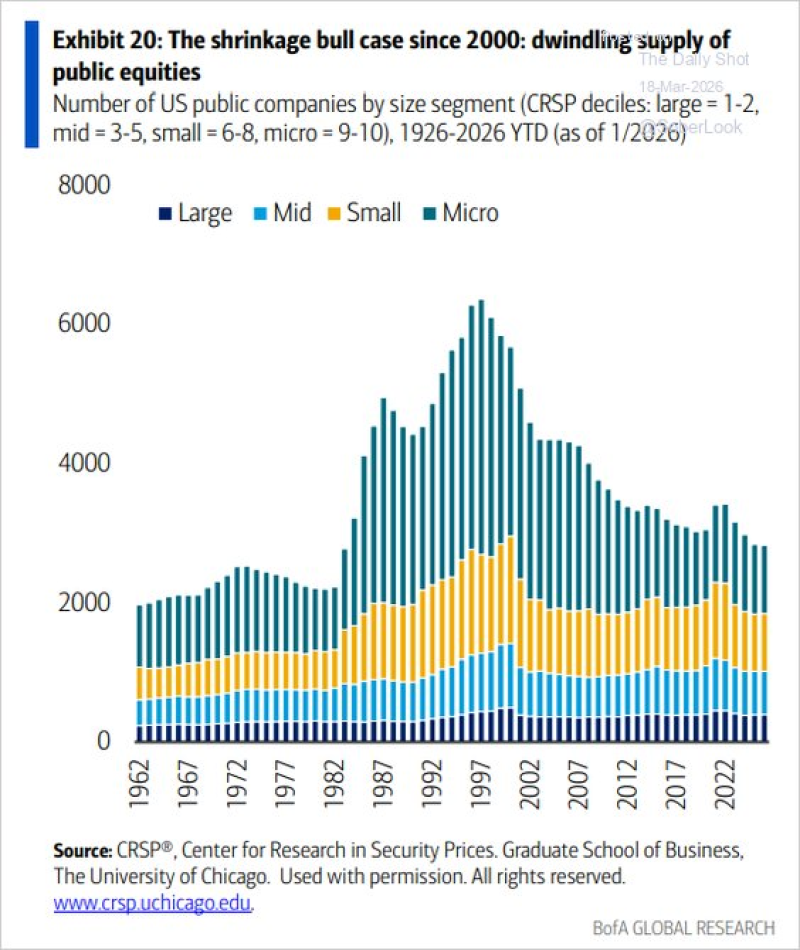

The S&P 500 (SPX) bull run is not just about earnings or sentiment - it reflects a deep structural shift in equity supply. The number of publicly traded U.S. companies has fallen by nearly 50% since the early 2000s, when listings topped 7,000. Today, more capital is chasing a shrinking pool of investable assets.

Public listings peaked in the late 1990s and have been declining ever since. The contraction is most visible in micro-cap and small-cap segments, which account for the bulk of the drop. By 2026, total listed firms remain far below historical highs - a persistent supply shortage that continues to shape market dynamics.

Meanwhile, demand for equities keeps growing. Institutional flows, passive indexing, and retirement capital have all increased stock exposure. With fewer companies available, money concentrates in the large-cap names that dominate SPX - which helps explain both elevated valuations and narrow market leadership. A significant share of fund managers now view U.S. equities as overvalued, yet flows persist.

This supply-demand mismatch is a defining feature of today's market structure. It supports continued strength in SPX but also increases concentration risk and hidden fragility. Goldman Sachs has flagged macro scenarios that could expose this vulnerability, while technical signals in SPY point to mounting internal pressure beneath the surface.

Artem Voloskovets

Artem Voloskovets