Marina Lyubimova

Marina Lyubimova

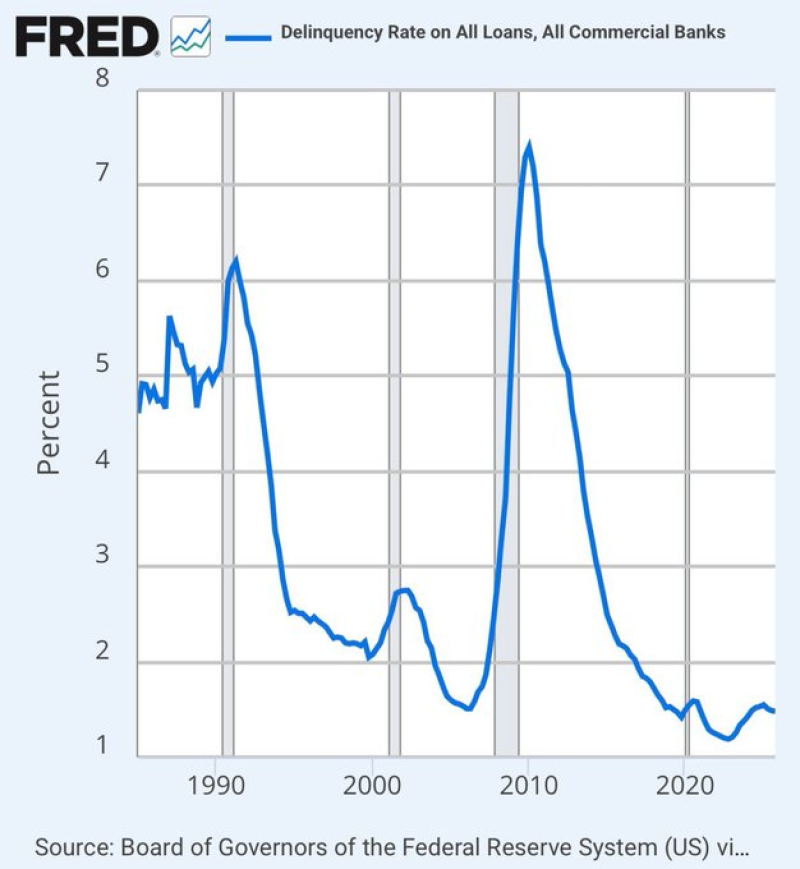

⬤ U.S. banking credit metrics are flashing a reassuring signal. The delinquency rate on all commercial bank loans has dropped to about 1.48%. That puts current readings near historic lows - a striking contrast to the crisis years. For context on just how bad things got before, check out what happened with US auto loan delinquencies hitting a record 6.9% as $1.67T in debt piled up, a reminder of how quickly specific loan categories can deteriorate.

⬤ The Federal Reserve's long-term chart tells a vivid story. Delinquency rates surged above 7% during the 2008 financial crisis and climbed sharply in the early 1990s recession before grinding lower through the 2000s and mid-2010s. Today's 1.48% sits near the floor of that entire dataset, with only brief dips slightly below this mark in recent years.

⬤ Analysts note that broad delinquency trends reveal how borrowers are managing repayments across a wide range of loan types. Fewer borrowers falling behind on scheduled payments - relative to total outstanding loan portfolios - points to genuine credit health improvement. That said, the picture isn't uniform everywhere. US credit card debt delinquencies recently reached a 14-year peak, a pocket of stress worth watching even as the broader bank loan metric holds low.

⬤ The sustained decline in delinquencies matters for financial market sentiment and overall perceptions of U.S. credit health. Persistently low readings suggest that widespread repayment problems have not taken hold across commercial bank loan books - even amid ongoing economic headwinds. For a deeper look at how some of these numbers have shifted over time, credit card delinquencies: the untold recovery story offers useful historical framing. As credit conditions evolve, the delinquency rate remains one of the clearest barometers of borrower resilience and overall financial system health.

Marina Lyubimova

Marina Lyubimova