Saad Ullah

Saad Ullah

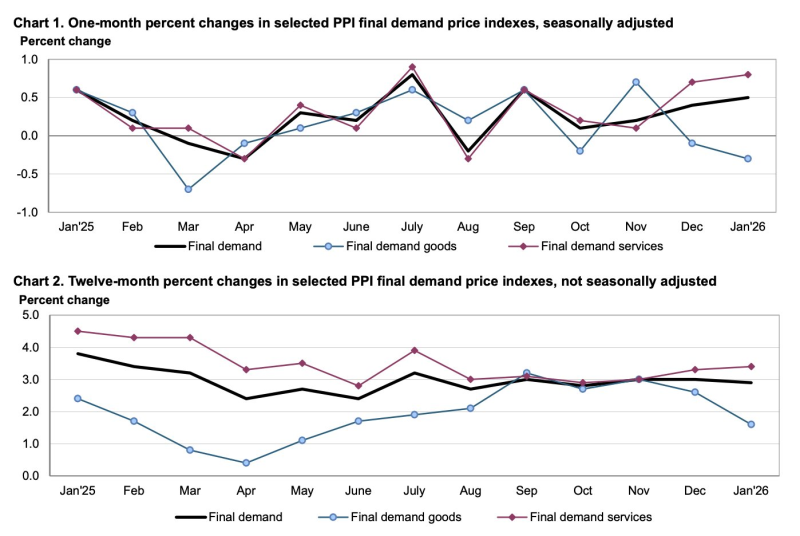

January's producer price data caught markets off guard. Headline PPI came in at 2.9% year over year - slightly under December's 3.0% but well above the 2.6% consensus. More striking was core PPI, which jumped to 3.6% from 3.3%, blowing past the 3.0% forecast. On a monthly basis, overall PPI rose 0.5% against an expected 0.3%, while core surged 0.8% versus a 0.3% estimate. As Truflation's prior PPI report had already flagged, producer-level price stickiness remains a real concern heading into 2026.

Looking at the broader trend, monthly producer inflation has been volatile throughout 2025 and into early 2026 - and January's reading signals renewed firmness. The twelve-month chart shows headline PPI running near the top of its recent range, with services consistently printing higher year-over-year gains than goods at multiple points. One nuance worth noting: the "ex food, energy, and trade" measure actually eased slightly, from 3.5% to 3.4% year over year, while holding steady at 0.3% month over month. That tells you some underlying categories cooled even as the broader number surprised higher. For more context on recent inflation trends at the consumer level, this CPI breakdown is worth a look.

PPI is widely watched as a potential leading indicator for CPI - when producers face higher costs, those increases can eventually reach consumers. But that transmission isn't guaranteed. With demand softening, many consumers are already trading down to cheaper alternatives or store-brand products, which puts pressure on producers and retailers to absorb costs rather than pass them on. That dynamic could limit how much of this PPI spike actually shows up in consumer prices down the line. Truflation's alternative CPI gauge at 0.94% suggests that official inflation metrics and real-world pricing may already be diverging.

The bottom line is that a hotter PPI print - especially in core measures - keeps the inflation picture murky. Elevated producer prices sustain uncertainty, but fading consumer demand could act as a natural ceiling on how far those pressures travel. That tug-of-war between firm PPI and softening demand is likely to stay front and center in both market conversations and Fed policy discussions in the months ahead.

Saad Ullah

Saad Ullah