Editorial staff

Editorial staff

Base: The Hows and Whys

Base is an Ethereum Layer-2 network incubated by Coinbase and built on the OP Stack, the open-source rollup framework developed by Optimism. It’s still young, mind you. First announced in February 2023, so roughly 3 years ago, as part of Coinbase’s broader strategy to expand from just being a centralized exchange to joining the big boy’s table. In crypto terms that means becoming an on-chain settlement infrastructure.

Here’s another important addition. Coinbase positioned Base not as a separate L1 competitor, but explicitly as an Ethereum-aligned scaling layer designed to reduce transaction costs while inheriting Ethereum’s security guarantees. At the time, Ethereum’s whole strategy was to develop its roadmap to expand the rollups, i.e. L2s and make the whole Mainnet a little lighter on its toes. Akin to how https://clideo.com video add consists of many subordinate app features that make it run.

The How-component

Transactions execute off-chain on the L2, in this case Base, are batched by a sequencer, and posted to Ethereum mainnet for data availability and final settlement. So it does what it was intended to do. Base, along with all other L2s allows significantly higher throughput and lower per-transaction costs relative to L1, while still anchoring finality to Ethereum. Mind you, gas fees are paid in ETH.

Base entered the market at a time when L2 competition was already well established, with Arbitrum and Optimism leading in TVL (total value locked). Coinbase promoted its L2 any way they knew how, including convenience. Bearing in mind, that Coinbase is one of the largest crypto exchanges globally, you can see why that would work. Users could bridge from Coinbase exchange directly to Base with minimal friction. So basically, they created a powerful onboarding funnel from centralized liquidity into on-chain applications.

All that payed off, and by 2024-2025, Base had become one of the leading Ethereum L2s by transaction count and active addresses, at times surpassing Optimism and Arbitrum in daily activity.

Today, Base functions as Coinbase’s strategic on-chain settlement layer, which is completely true. It acts as a bridge between centralized exchange liquidity and decentralized application execution. But what about today?

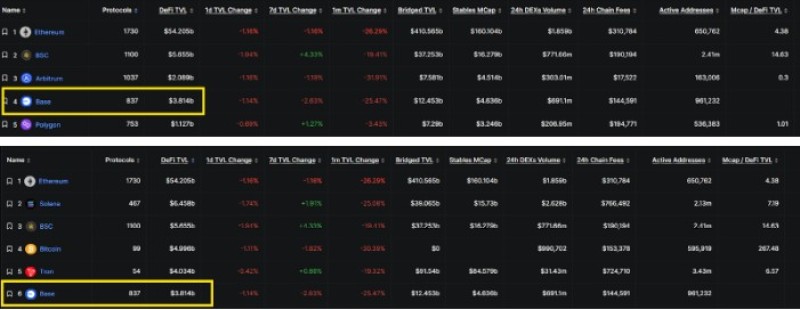

Look at the data below from DeFiLlama. As you can see, Base is the 6th overall chain based on overall TVL, and the 4th overall based (forgive the pun) on the number of deployed projects.

But there’s another factor here that’s worth mentioning.

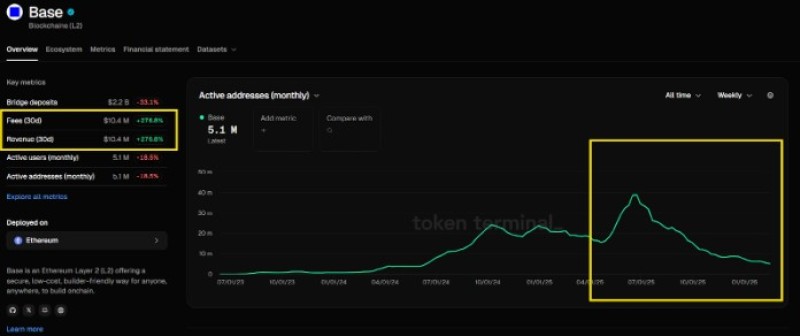

Base Dynamics As Of Feb 2026

Base active addresses peaked in late June, 2025, then dropped rather dramatically, and lay low as of Feb 2026, and I mean June 2024 low, when the chain was just getting started. But the overall health is pink and lively, if you know what I mean. Just look at the left side of the chart. The monthly fees are up. Not just up, they are up 277% in 30 days. That’s no joking matter. Plust the overall revenue followed suit, with a similar percentage, logically.

Let’s make sense of this. The data you’re looking at shows a very specific economic shift on Base, and it needs to be interpreted carefully.

Again, over the past 30 days, Fees and Revenue both stand at $10.4 million, up +276.8%, while monthly active addresses are 5.1 million, down –18.5% (that’s Token Terminal data, not something I made up. On the surface, this creates a paradox: monetization is accelerating aggressively, yet participation breadth is shrinking.

First things first. Definitions. On Token Terminal, fees represent the total amount users pay to transact on the network. Revenue is the portion kept by the protocol after applying its take-rate policy. That’s the basic part (can’t help the pun!). For Base (remember, it’s an Ethereum Layer 2 built on the OP Stack), the ‘cost of revenue’ per se primarily consists of L1 batch posting costs paid to Ethereum for data availability and settlement.

The fact that Fees (30d) = Revenue (30d) = $10.4M, both up +276.8%, indicates that total user payments to the chain have increased nearly 3.8x over the comparison period. Meanwhile, let’s remember that the network’s active address count has fallen by 18.5%. This mechanically implies that fee density per active address has risen significantly.

In plain English, that means the network is extracting more value from fewer wallets.

Big Player Manipulation?

Hold on, don’t throw daggers just yet. This does not automatically mean fewer big players are taking everyone’s lunch money. Address count is actually a weak proxy for participant size. Large traders and market makers often use multiple addresses. Retail users can aggregate through smart wallets or centralized exchange withdrawal clusters.

A drop in active addresses more often means a reduction in low-value or incentive-driven activity than a disappearance of institutional flow. So what DID cause the situation? There are several possible drivers at the wheel.

#1 Scenario. Disinterested Users Across The Board?

One explanation is an incentive unwind. That well could be the case. If a prior period was driven by quests, points programs, or airdrop farming, the network could lose a large number of low-value ‘sybil’ wallets while maintaining or even increasing economically meaningful activity. In that case, transactions per active address would rise, and new address creation would fall.

#2 Higher Fee Mediums

A second possibility is an app-mix shift toward higher-fee surfaces. If activity rotates toward DEX routing, NFT mints, perps trading, or bridge-heavy flows, total fees can spike even if unique participants decline. In that Scorsese scenario, fee concentration across a small number of contracts would increase.

#3 Ethereum Mainnet Passthrough

We’ve discussed this previously. As an optimistic rollup, Base posts transaction data to Ethereum. If Ethereum data availability costs rise and are passed through to users, that means the average fee per transaction increases regardless of user growth. Token Terminal isolates this as “cost of revenue” (L1 posting costs). If fees rise alongside the cost of revenue, gross margin may not expand proportionally.

There’s one thing we could say for sure. What it does not prove is that there’s any malintent involved, people. No proof that fewer ‘big boys’ are responsible.

In finance talk, the data is consistent with reduced low-value activity, higher per-transaction costs, greater transaction intensity among remaining users, or concentration in high-fee applications.

Editorial staff

Editorial staff