Saad Ullah

Saad Ullah

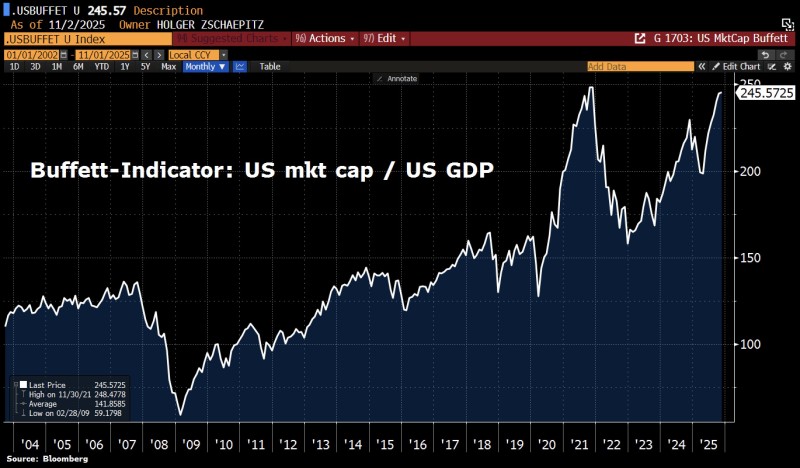

Warren Buffett has a favorite way to gauge whether the stock market is overpriced: compare total market value to GDP. Right now, that ratio is flashing red.

What the Numbers Say

According to Holger Zschaepitz, the Buffett Indicator just hit 245.6%—meaning U.S. stocks are worth more than twice the entire economy. That's territory we've only seen once before, at the peak of the pandemic stimulus boom in 2021. The question everyone's asking: is this time different, or are we setting up for another fall?

As of early November 2025, U.S. market capitalization sits at roughly $2.45 for every dollar of annual GDP output. Historically, anything near 100% is considered fair value. Above 150%? The market's getting pricey. At 245%, we're in rarified air.

Here's how today's reading compares to past extremes:

- 2000 (Dot-com peak): ~150%, followed by a brutal crash

- 2008–09 (Financial crisis low): Dropped to just 59%

- 2021 (Stimulus era peak): Hit 248%, the highest on record

- 2025 (AI boom phase): Back to 245%, despite higher rates and slower growth

In short, valuations are once again approaching speculative levels—even though the Fed isn't pumping easy money anymore.

Why Are Stocks So Expensive?

A few big forces are keeping valuations sky-high. The "Magnificent 7" tech giants now make up over 30% of the entire U.S. market. AI hype has sent earnings expectations soaring. Corporate buybacks and ETF inflows keep pushing prices up. And global investors still see the U.S. as the safest place to park money, especially compared to Europe or China. All of this has created a market that looks unstoppable—until it isn't.

Buffett has called this ratio "the best single measure of where valuations stand at any given moment." At 245%, the market sits more than 70% above its long-term average of 142%. History shows that when the indicator tops 200%, the next decade usually delivers weak returns as reality catches up to expectations. But some analysts argue that digital productivity and intangible assets like AI make old valuation rules obsolete.

Bears see this as a classic bubble—stretched tech valuations propped up by hype rather than fundamentals. Bulls counter that the U.S. economy has fundamentally changed, and traditional metrics don't capture the value of software, data, and AI infrastructure. Either way, by Buffett's favorite measure, U.S. stocks have rarely been this expensive. Whether that signals caution or opportunity depends on who you ask—but history suggests betting on gravity might not be a bad idea.

Saad Ullah

Saad Ullah