Saad Ullah

Saad Ullah

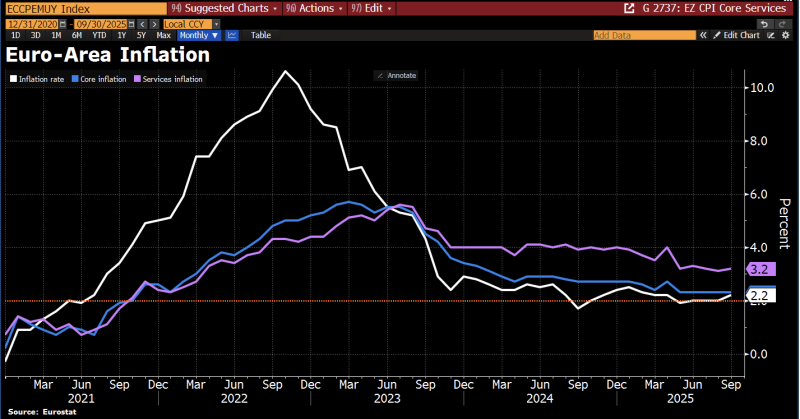

September brought an unwelcome surprise for the eurozone - inflation ticked higher for the first time in months. Headline CPI came in at 2.2% year-over-year, while core inflation held firm near 2.3%.

The Tale of Two Inflations

Data shared by Holger Zschaepitz shows this wasn't a clean victory lap. The overall number looks manageable, but dig deeper and the picture gets messier.

Eurostat's latest chart tells the real story. Yes, we've come a long way from the 10%+ nightmare of 2022. But services inflation is still running hot at 3.2%, and that's a problem. Goods prices have cooled off nicely, but anything involving wages and labor - restaurants, haircuts, repairs - keeps pushing higher. The economy has a split personality right now.

This September bump isn't what it seems. Energy prices crashed hard last year, creating what economists call a "base effect" - basically, this year's numbers look inflated just because we're comparing them to unusually low figures from 2024. There's no new energy crisis brewing. It's just math playing tricks on the headline rate. But it makes the ECB's job harder because the optics aren't great.

Services Are the Real Headache

Core inflation might be stable, but services have been stubborn all through 2024 and into 2025, consistently above 3%. Wages are still climbing as workers demand raises to catch up with the cost of living. Companies are passing those costs straight to customers. This is the inflation the ECB actually worries about because it doesn't go away on its own.

Frankfurt is stuck. Inflation is technically near the 2% target, but the services number screams "don't ease yet." Markets have pretty much priced out any aggressive rate cuts through 2025. The central bank needs more proof that wage pressures are really cooling before they'll move. September's reading just bought them more time to watch and wait.

Saad Ullah

Saad Ullah