Usman Salis

Usman Salis

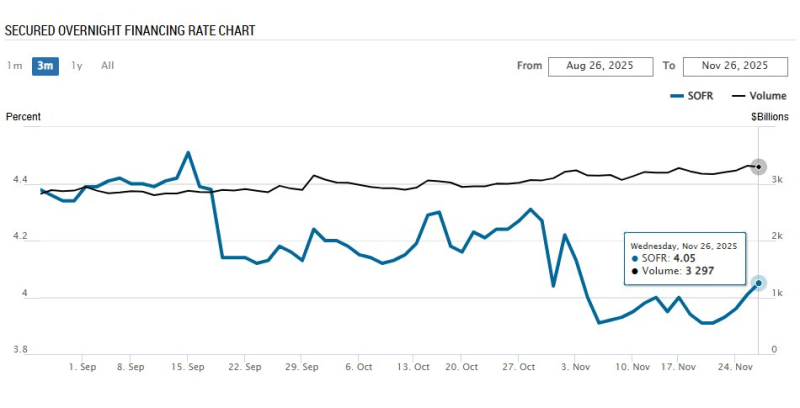

⬤ On November 26 the Secured Overnight Financing Rate reached 4.05 percent, above the Federal Reserve's upper target bound. On the same day institutions placed $7.561 billion at the Fed's overnight reverse repo facility for 3.75 percent. The gap shows that traders will pay more for secured funds in the open market than accept the lower RRP rate. Such action normally appears near month end when banks must strengthen their balance sheets.

⬤ The three month chart shows SOFR near 4.3 percent in early September then drifted toward 4 percent through October. Since early November the rate has climbed steadily to 4.05 percent on daily volume near $3.297 billion. The difference between the RRP return and the market cost keeps widening, a sign that some participants now treat liquidity with caution.

⬤ When SOFR prints above the Fed funds ceiling, demand for overnight cash exceeds the amount banks will supply. Month-end RRP spikes are routine - yet persistently high SOFR together with steady inflows into the facility indicates that firms are playing defense. The Fed watches such frictions - they can foreshadow stress before it appears in standard data.

⬤ Short-term rates like SOFR react first when liquidity conditions change. If the pattern continues - high SOFR plus heavy RRP usage - borrowing costs across markets will rise, risk appetite will cool and traders will react more sharply to policy shifts. The effects will not stay within overnight markets - they will spread into credit availability and overall financial stability during the weeks ahead.

Usman Salis

Usman Salis